This presentation andits contents have been prepared by Hyundai Capital Services, Inc. (“HCS” or “the

Company”) solely for information purposes, and may not be reproduced, published, redistributed, or transferred,

directly or indirectly to any other person, in whole or in part, for any purpose.

The Company has not taken measures to independently verify data contained in this material. No representations or warranties,

express or implied, are made as to, and no reliance should be placed on, the accuracy, fairness or completeness of the information

presented or contained herein. This presentation shall not be construed as legal, tax, investment, or other advice.

Financial statements in this document have been prepared in accordance with K-IFRS. Other additional contents such as market or

industry information have been sourced internally or from various associations. The data contained in this presentation is current

as of the date hereof, but the Company shall not be liable for any updates or verification of the contents thereafter.

Certain information and statements in this presentation contain estimates and other “forward-looking statements” which should

be approached with caution. The Company shall not be responsible for any losses or damages incurred based on these forward-

looking statements.

Disclaimer

3.

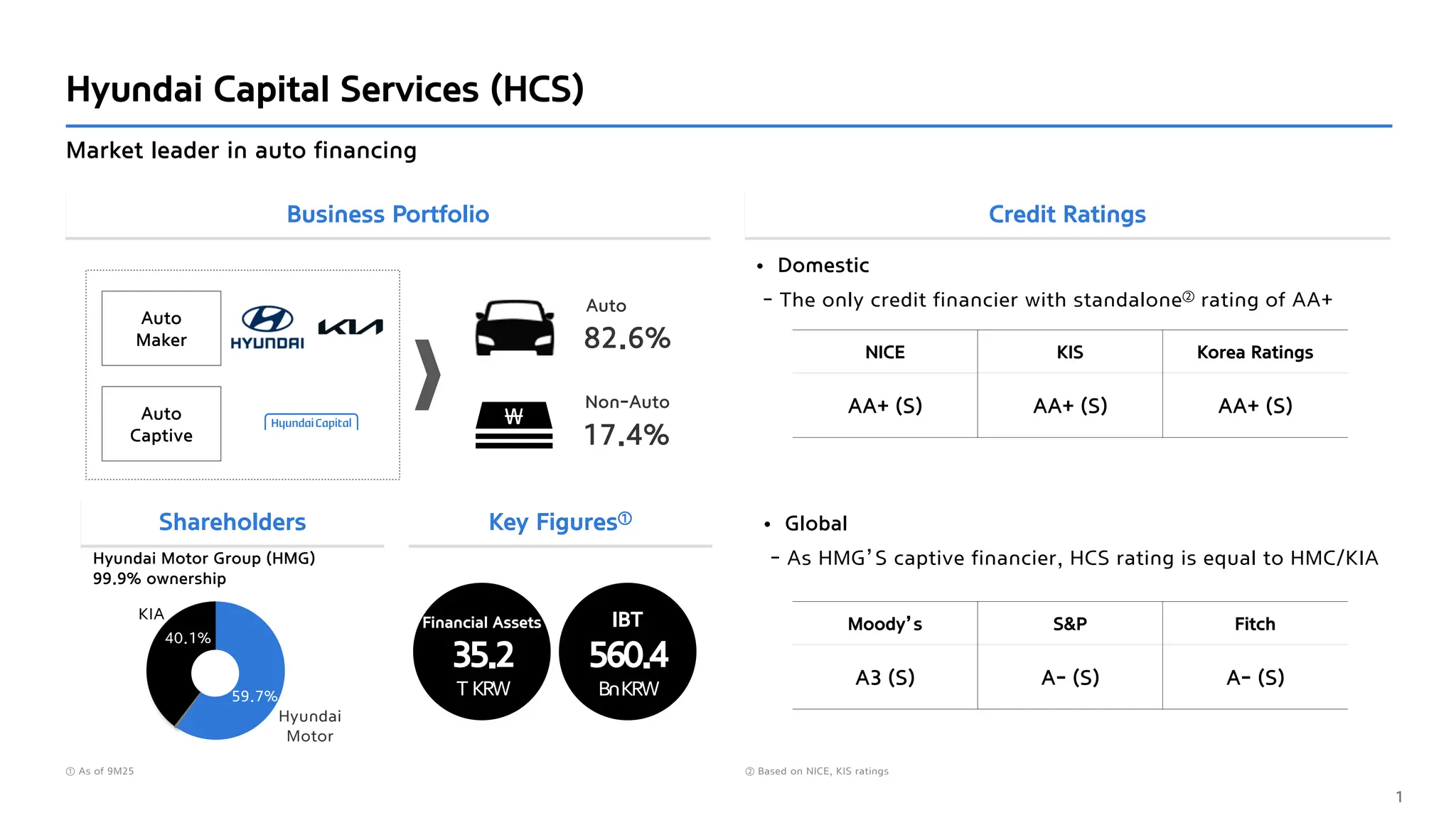

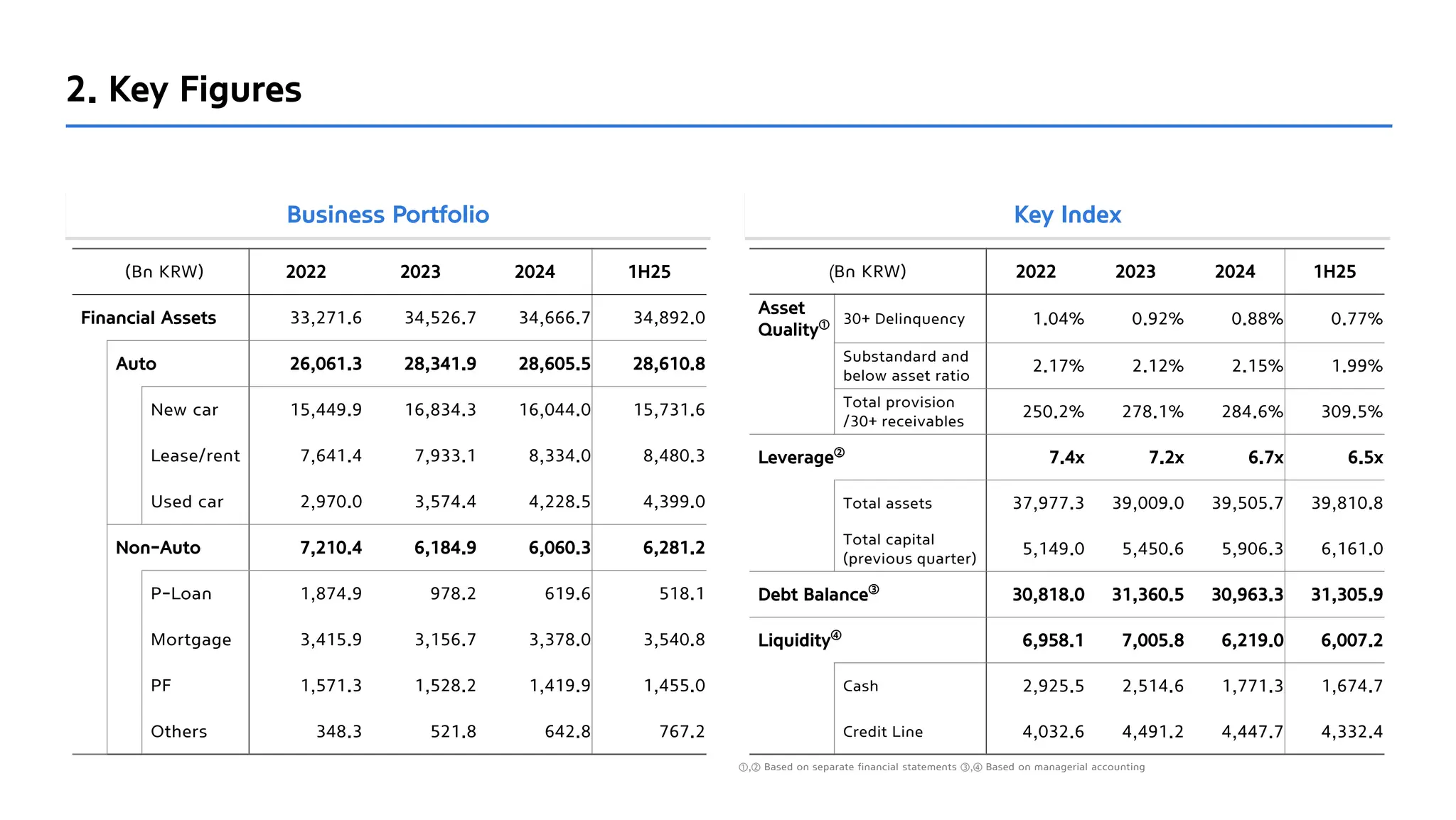

Business Portfolio CreditRatings

Hyundai Capital Services (HCS)

Market leader in auto financing

1

Hyundai Motor Group (HMG)

99.9% ownership

Moody’s S&P Fitch

A3 (S) A- (S) A- (S)

Auto

Captive

Auto

Maker 82.6%

Auto

₩

17.4%

Non-Auto

Financial Assets

35.2

T KRW

IBT

560.4

BnKRW

59.7%

40.1%

Shareholders Key Figures①

• Domestic

- The only credit financier with standalone② rating of AA+

• Global

- As HMG’S captive financier, HCS rating is equal to HMC/KIA

NICE KIS Korea Ratings

AA+ (S) AA+ (S) AA+ (S)

① As of 9M25 ② Based on NICE, KIS ratings

Hyundai

Motor

KIA

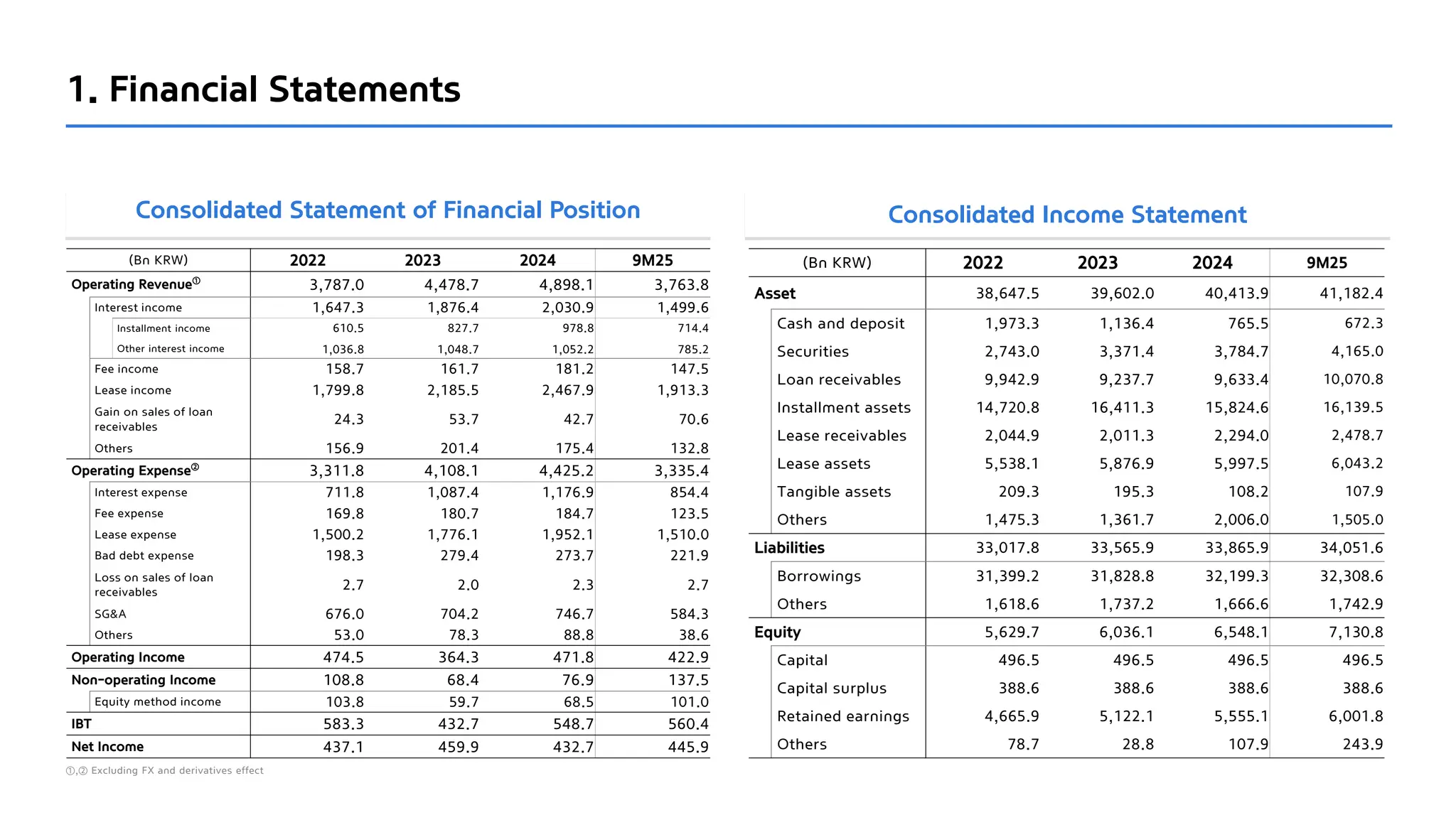

4.

23%

12%

16%

32%

17%

9M25

④ HMC Genesis+SUV,KIA RV

HMG Global Car Sales① HMG Sales Mix and Profitability

Hyundai Motor Group (HMG)

• Strong sales performance in key markets, and continued

improvement in sales mix

• Sales mix focused on High Average Sales Price(ASP) models

Mitigating tariff headwinds through premium mix impact and structural enhancement

• Safeguarding profitability with increased hybrid mix

Operating

income

Operating

margin

Revenues

(T KRW)

(K units)

Car Sales by Region

Global

HMG Global

Car Sales①

Others

India

Europe③

North

Americas②

Korea

2

Korea North Americas

Europe India

Portion of

High ASP

Models④

HMC KIA

HMC KIA

① HMC, KIA Biz. Performance Report, Wholesale ② HMC North Americas, KIA US ③ HMC Europe, KIA Western Europe

75,809

82,612 84,292

6,845 7,307 7,231

2022 2023 2024

5,478

60,919

62,739

5,395 5,478

9M24 9M25

917 950

9M24 9M25

1,703 1,752

9M24 9M25

654 633

9M24 9M25

887 878

9M24 9M25

61.7% 63.2%

9M24 9M25

69.9% 69.5%

9M24 9M25

12.4%

8.4%

8.9%

7.0%

11.4 9.8 10.0

7.2

80 86

9M24 9M25 9M24 9M25

129

139

5.

1.9

1.0 0.6 0.4

3.4

3.23.4 3.6

1.6

1.5 1.4 1.4

0.3

0.5 0.6 0.8

7.2T

6.2T 6.1T 6.1T

2022 2023 2024 9M25

15.4 16.8 16.0 16.0

7.6

7.9 8.3 8.6

3.0

3.6 4.2 4.4

26.1T

28.3T 28.6T 29.1T

2022 2023 2024 9M25

Auto Non-Auto

Asset

• New cars/Lease: Captive growth driven by stronger installment

and lease momentum

• Used cars: Offering captive financing for HMG CPO vehicles

• P-Loan: 100% X-Sell to Auto Finance customers

• PF: Focused on senior, metropolitan exposure

Maintaining auto-centric asset portfolio

Portion

3

New Car

Lease

Used car

(T KRW)

P-Loan

Mortgage

Others

PF

Portion

(T KRW)

HMG M/S P-Loan %

73.3% 76.8% 76.6% 75.3% 5.6% 2.8% 1.8% 1.3%

78.3%

82.1% 82.5% 82.6%

21.7%

17.9% 17.5% 17.4%

6.

0.94% 1.04%

0.92% 0.88%

0.77%

20212022 2023 2024 9M25

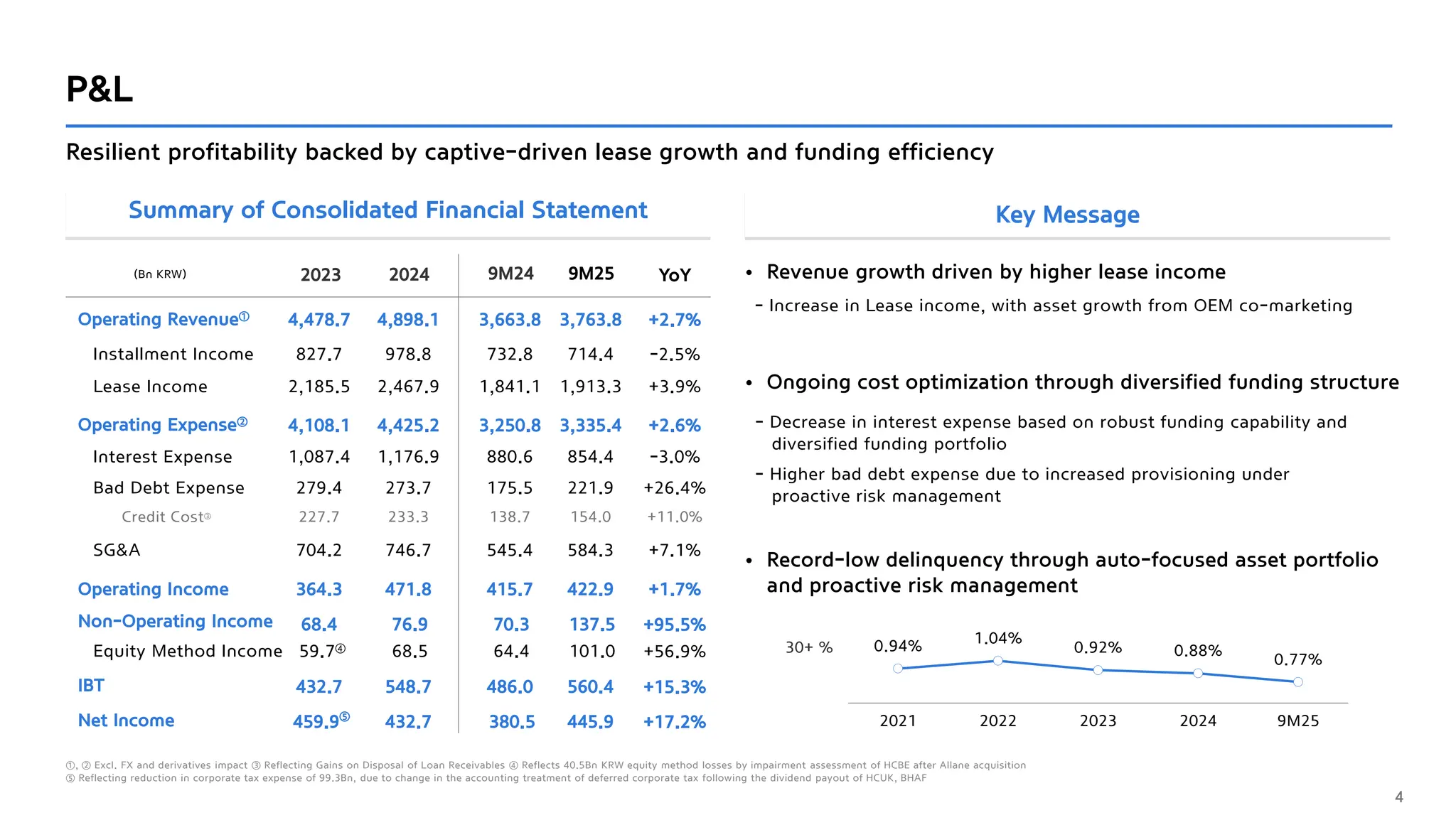

Summary of Consolidated Financial Statement Key Message

P&L

• Revenue growth driven by higher lease income

Resilient profitability backed by captive-driven lease growth and funding efficiency

(Bn KRW)

- Increase in Lease income, with asset growth from OEM co-marketing

30+ %

4

- Decrease in interest expense based on robust funding capability and

diversified funding portfolio

- Higher bad debt expense due to increased provisioning under

proactive risk management

①, ② Excl. FX and derivatives impact ③ Reflecting Gains on Disposal of Loan Receivables ④ Reflects 40.5Bn KRW equity method losses by impairment assessment of HCBE after Allane acquisition

⑤ Reflecting reduction in corporate tax expense of 99.3Bn, due to change in the accounting treatment of deferred corporate tax following the dividend payout of HCUK, BHAF

• Ongoing cost optimization through diversified funding structure

• Record-low delinquency through auto-focused asset portfolio

and proactive risk management

Interest Expense

Lease Income

Installment Income

Bad Debt Expense

Equity Method Income

SG&A

Operating Revenue①

Operating Expense②

Operating Income

IBT

Non-Operating Income

Net Income

Credit Cost③

2023

4,478.7

4,108.1

364.3

1,087.4

432.7

2,185.5

827.7

279.4

68.4

59.7④

459.9⑤

704.2

227.7

YoY

+2.7%

+2.6%

+1.7%

-3.0%

+15.3%

+3.9%

-2.5%

+26.4%

+95.5%

+56.9%

+17.2%

+7.1%

+11.0%

4,898.1

4,425.2

471.8

1,176.9

548.7

2,467.9

978.8

273.7

76.9

68.5

432.7

746.7

233.3

2024 9M24

3,663.8

3,250.8

415.7

880.6

486.0

1,841.1

732.8

175.5

70.3

64.4

380.5

545.4

138.7

9M25

3,763.8

3,335.4

422.9

854.4

560.4

1,913.3

714.4

221.9

137.5

101.0

445.9

584.3

154.0

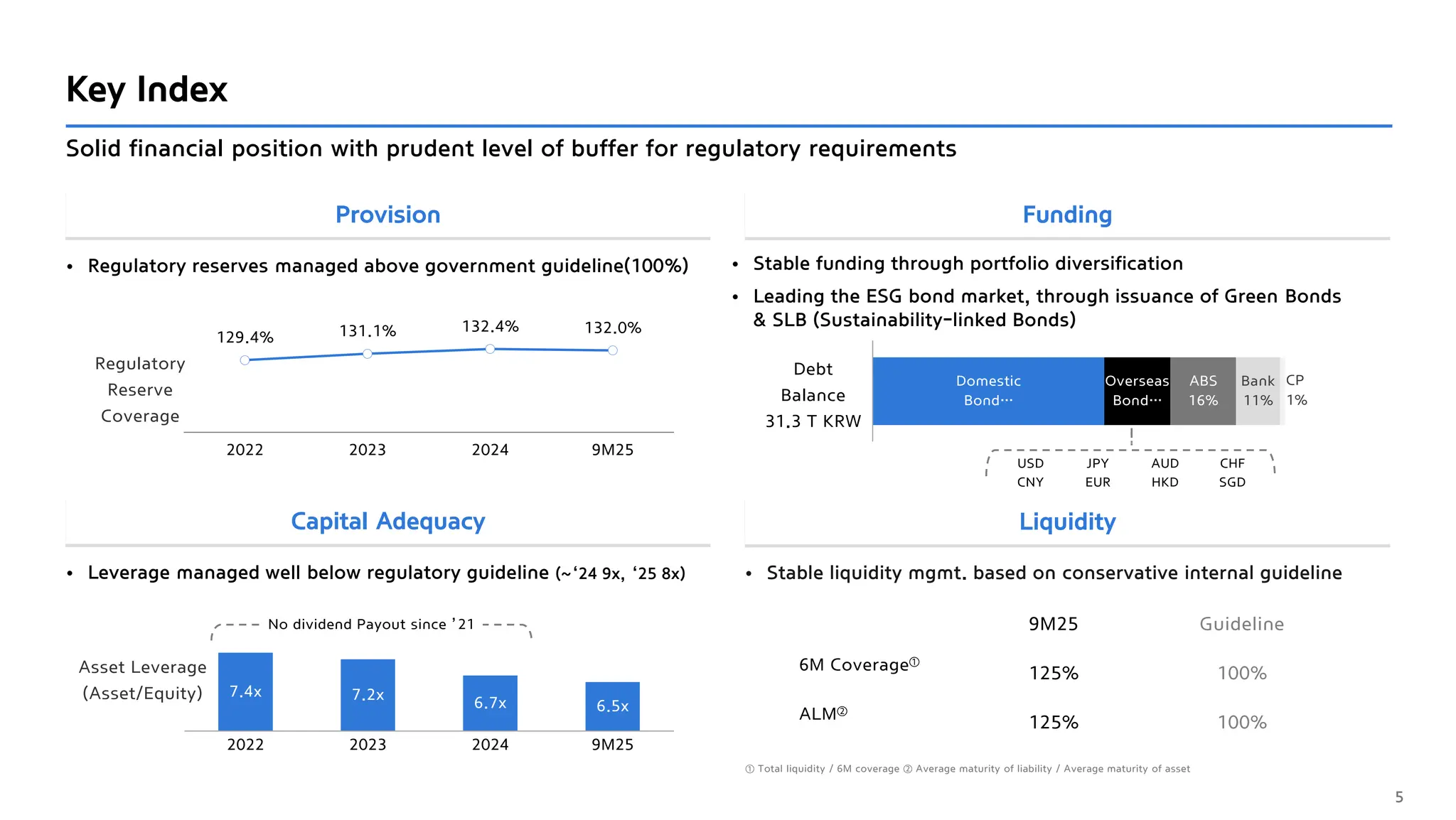

7.

Capital Adequacy Liquidity

ProvisionFunding

Key Index

• Regulatory reserves managed above government guideline(100%) • Stable funding through portfolio diversification

• Leading the ESG bond market, through issuance of Green Bonds

& SLB (Sustainability-linked Bonds)

Solid financial position with prudent level of buffer for regulatory requirements

Debt

Balance

31.3 T KRW

9M25 Guideline

6M Coverage①

125% 100%

ALM②

125% 100%

• Stable liquidity mgmt. based on conservative internal guideline

5

Asset Leverage

(Asset/Equity)

Regulatory

Reserve

Coverage

z

No dividend Payout since ’21

• Leverage managed well below regulatory guideline (~‘24 9x, ‘25 8x)

USD JPY AUD CHF

CNY EUR HKD SGD

① Total liquidity / 6M coverage ② Average maturity of liability / Average maturity of asset

Domestic

Bond…

Overseas

Bond…

ABS

16%

Bank

11%

CP

1%

7.4x 7.2x 6.7x 6.5x

2022 2023 2024 9M25

129.4% 131.1% 132.4% 132.0%

2022 2023 2024 9M25

![Where to Buy LinkedIn Accounts_ [12 Best Sites] (3).pdf](https://cdn.slidesharecdn.com/ss_thumbnails/wheretobuylinkedinaccounts12bestsites3-251124162550-95b6ddfa-thumbnail.jpg?width=640&height=640&fit=bounds)