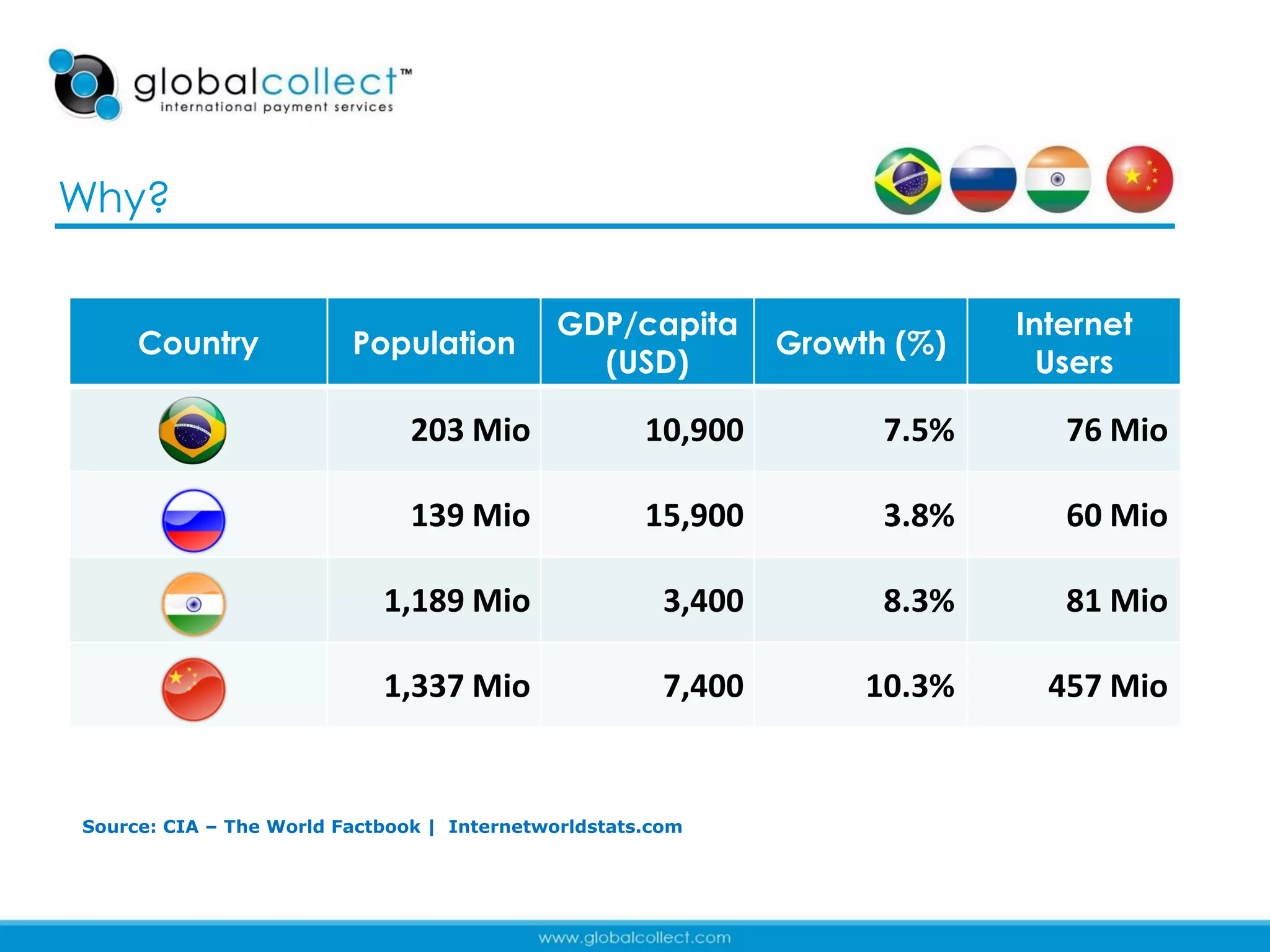

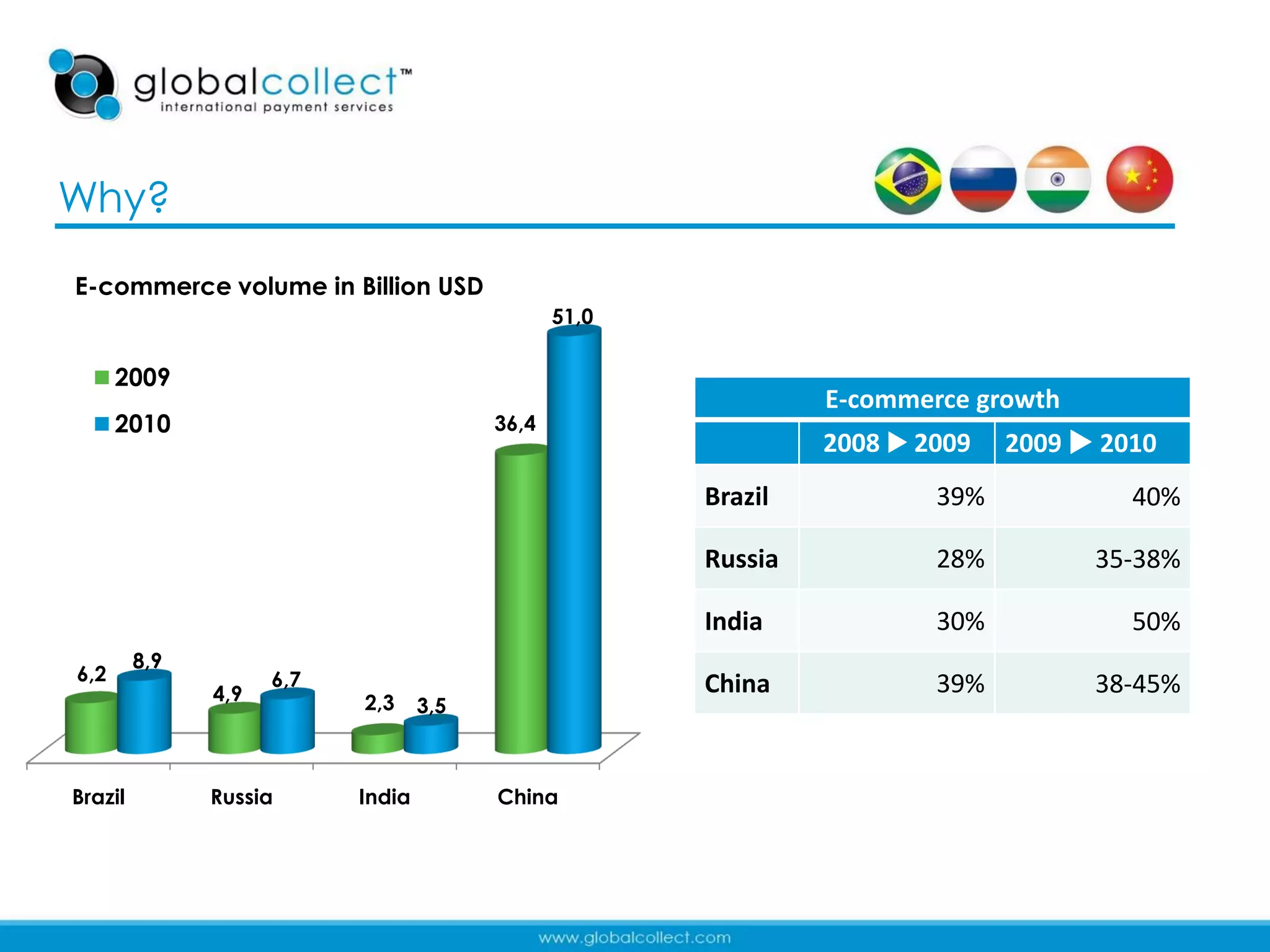

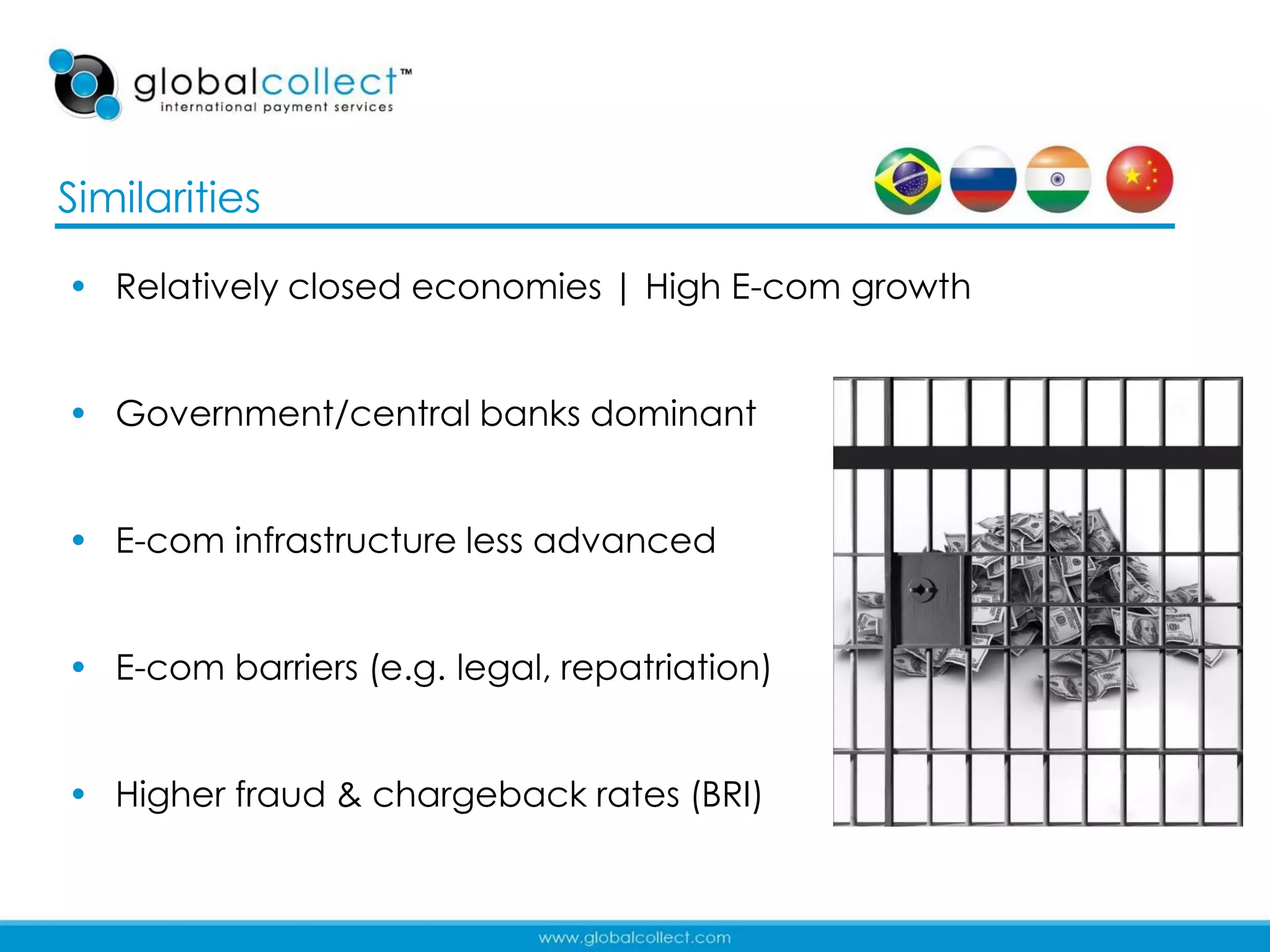

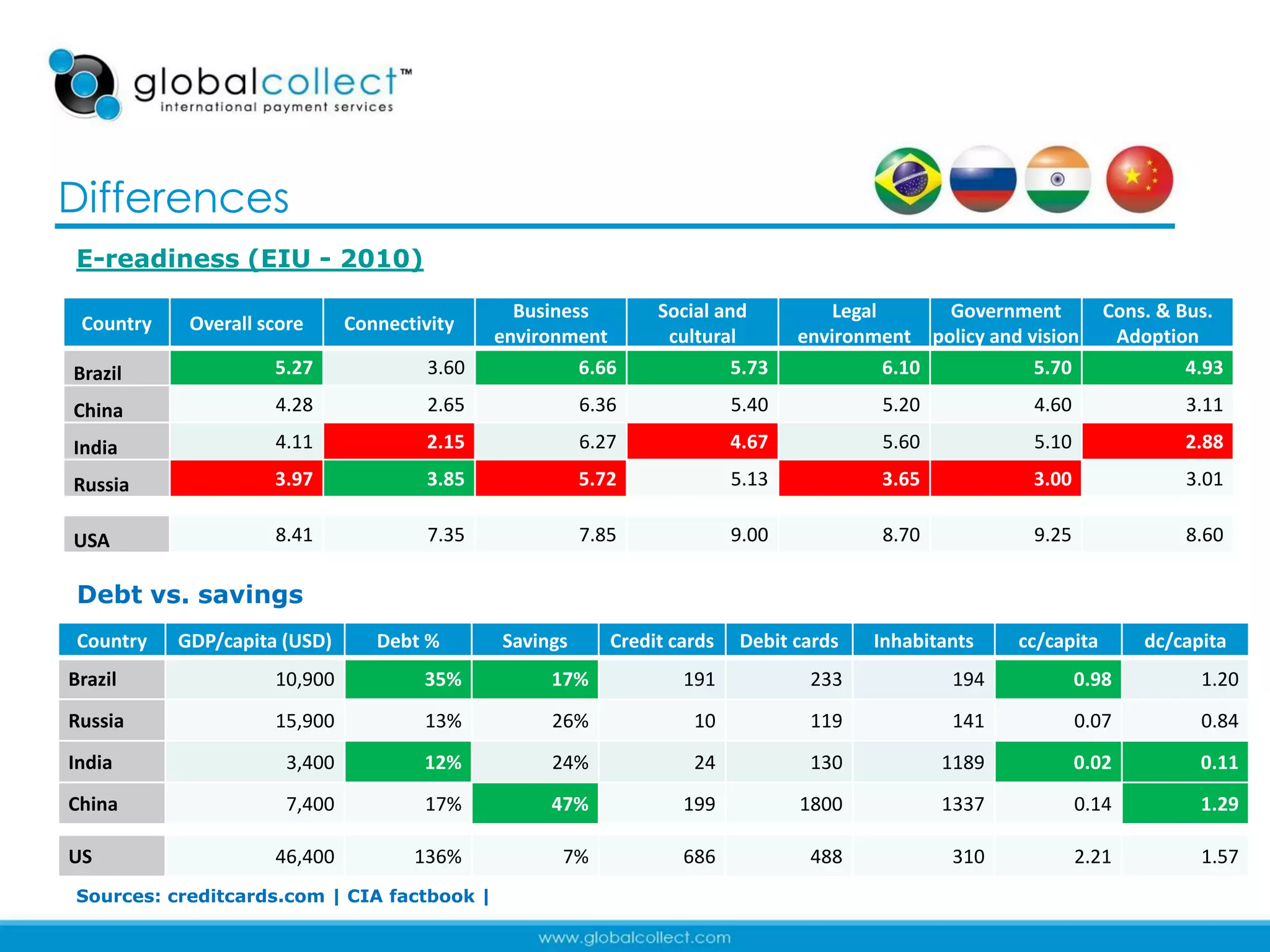

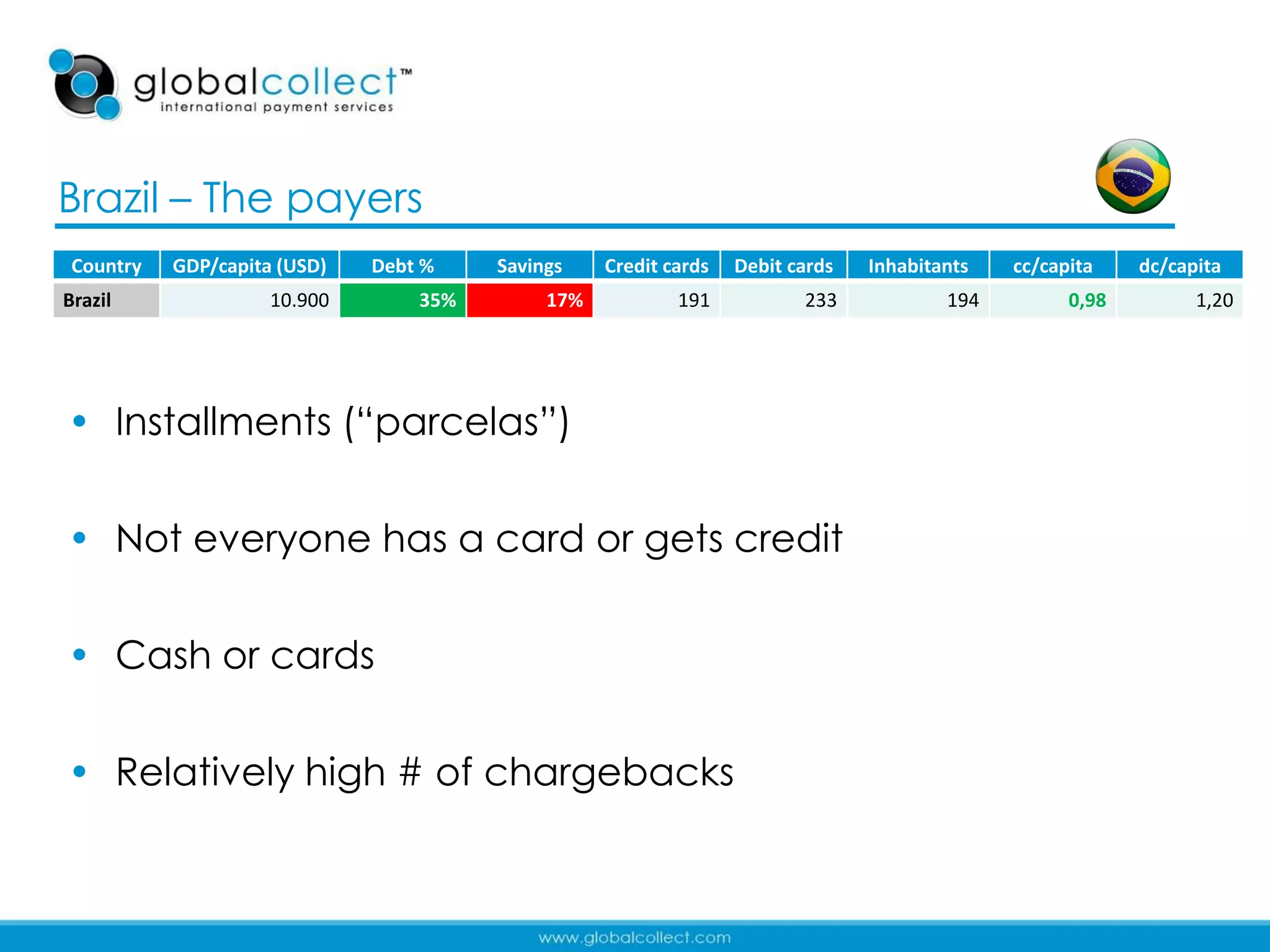

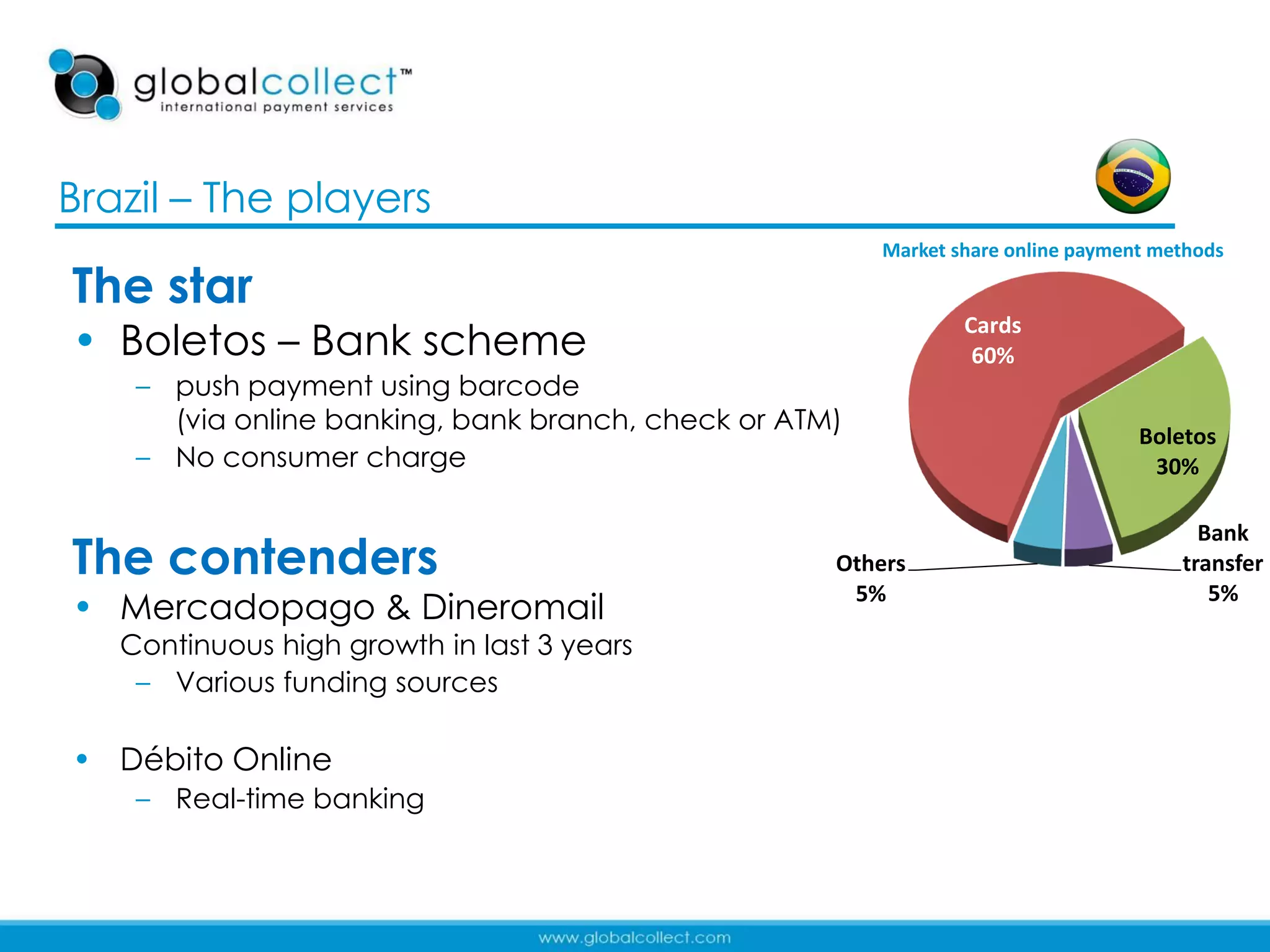

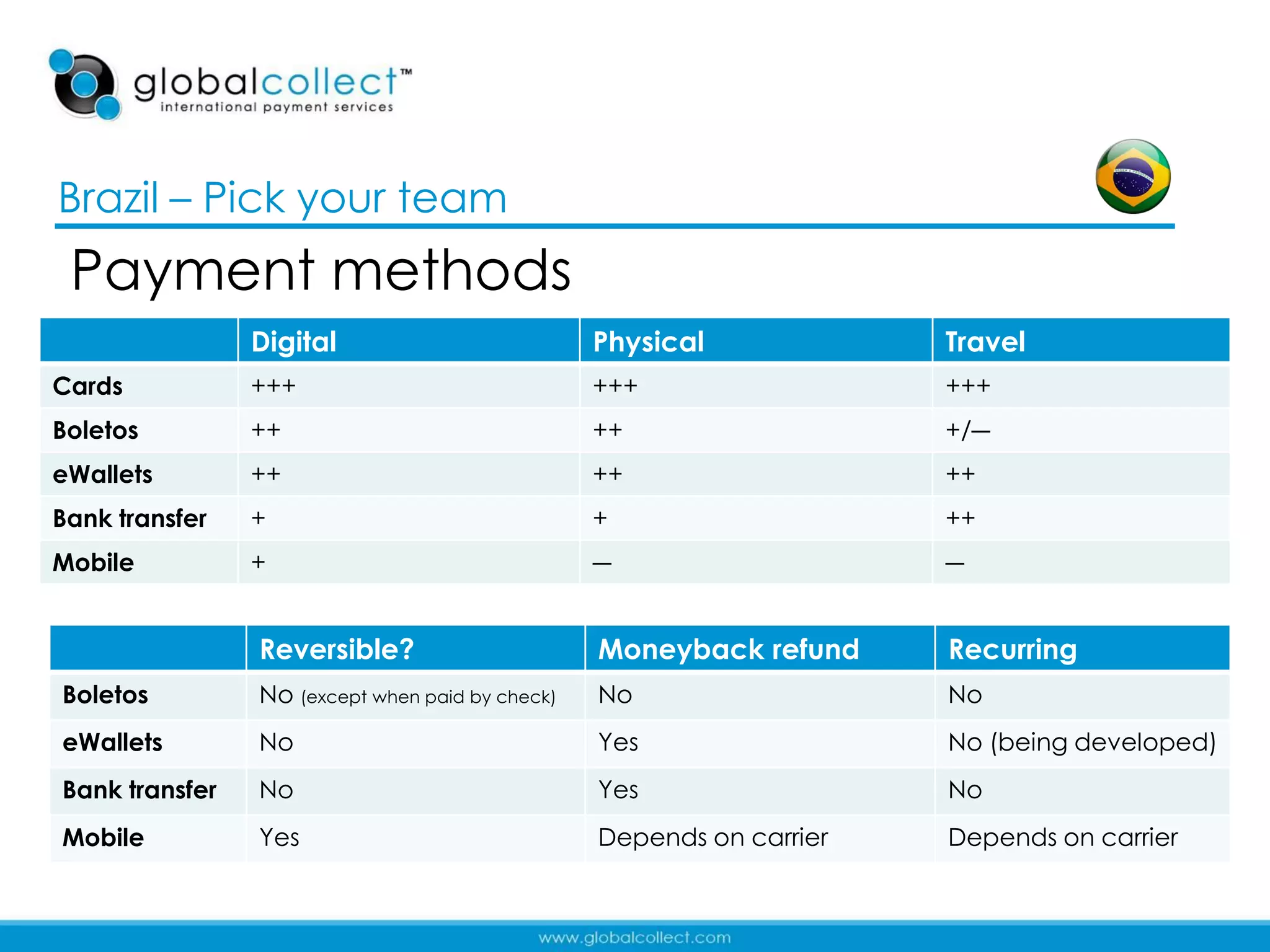

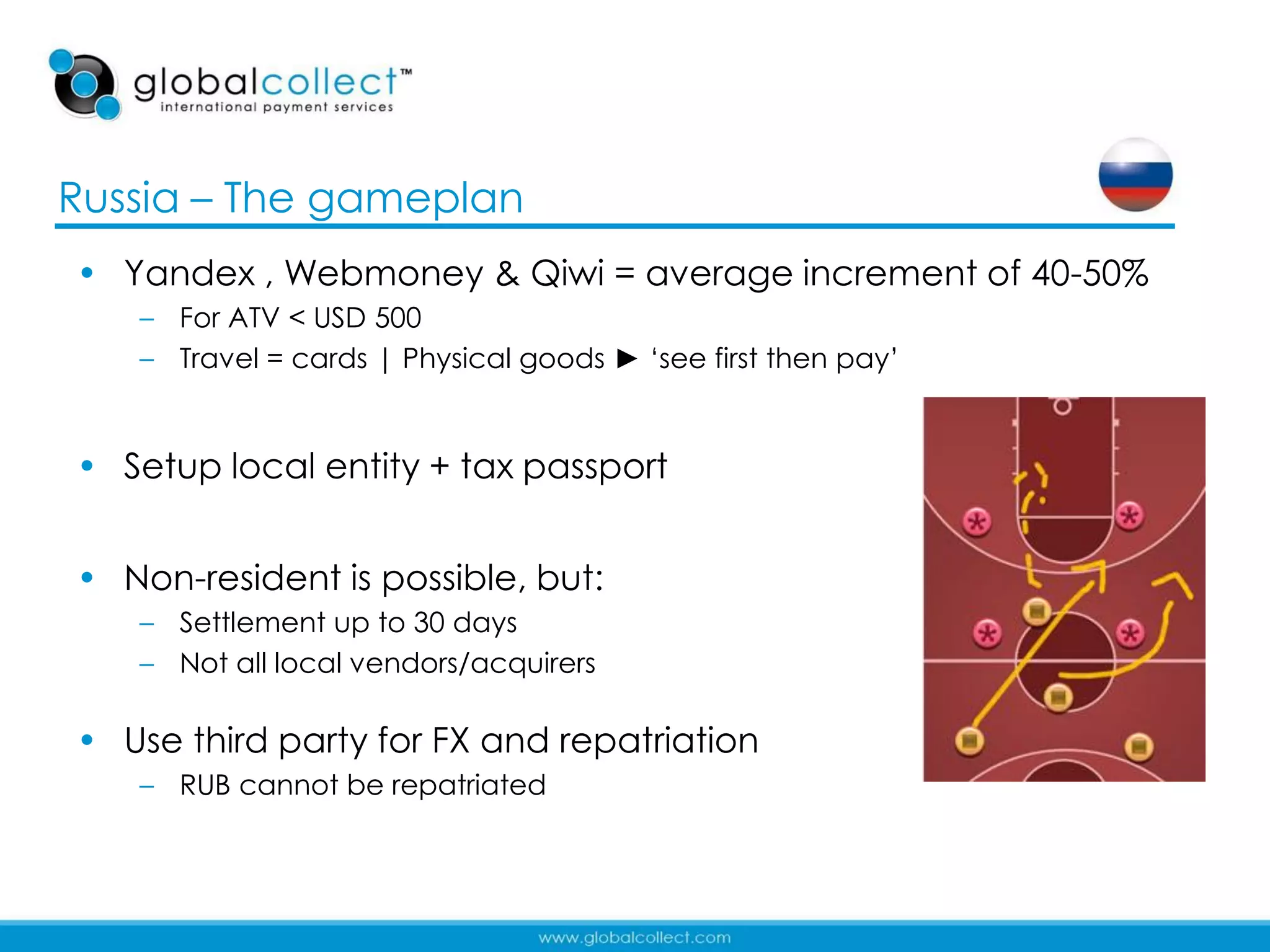

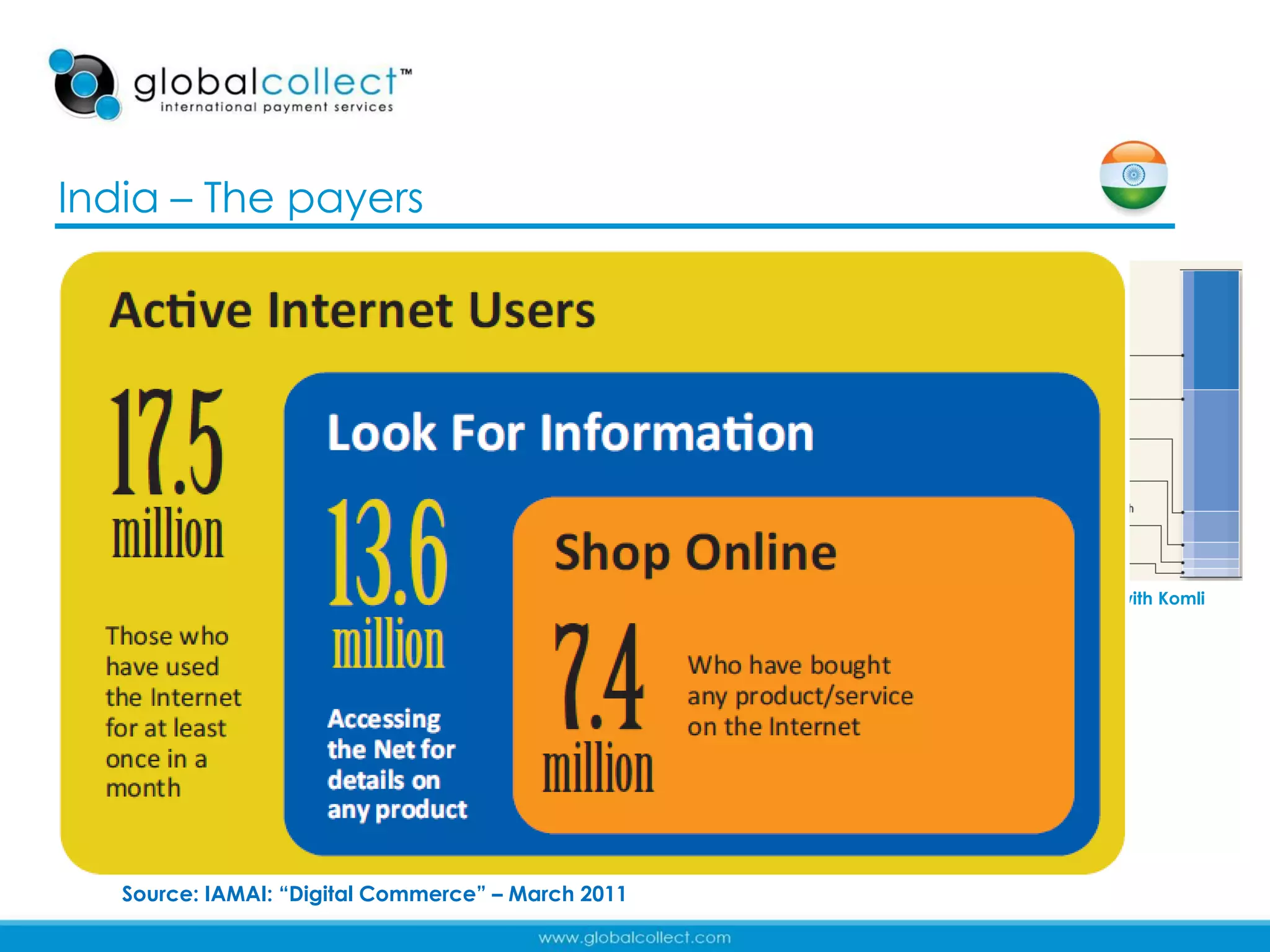

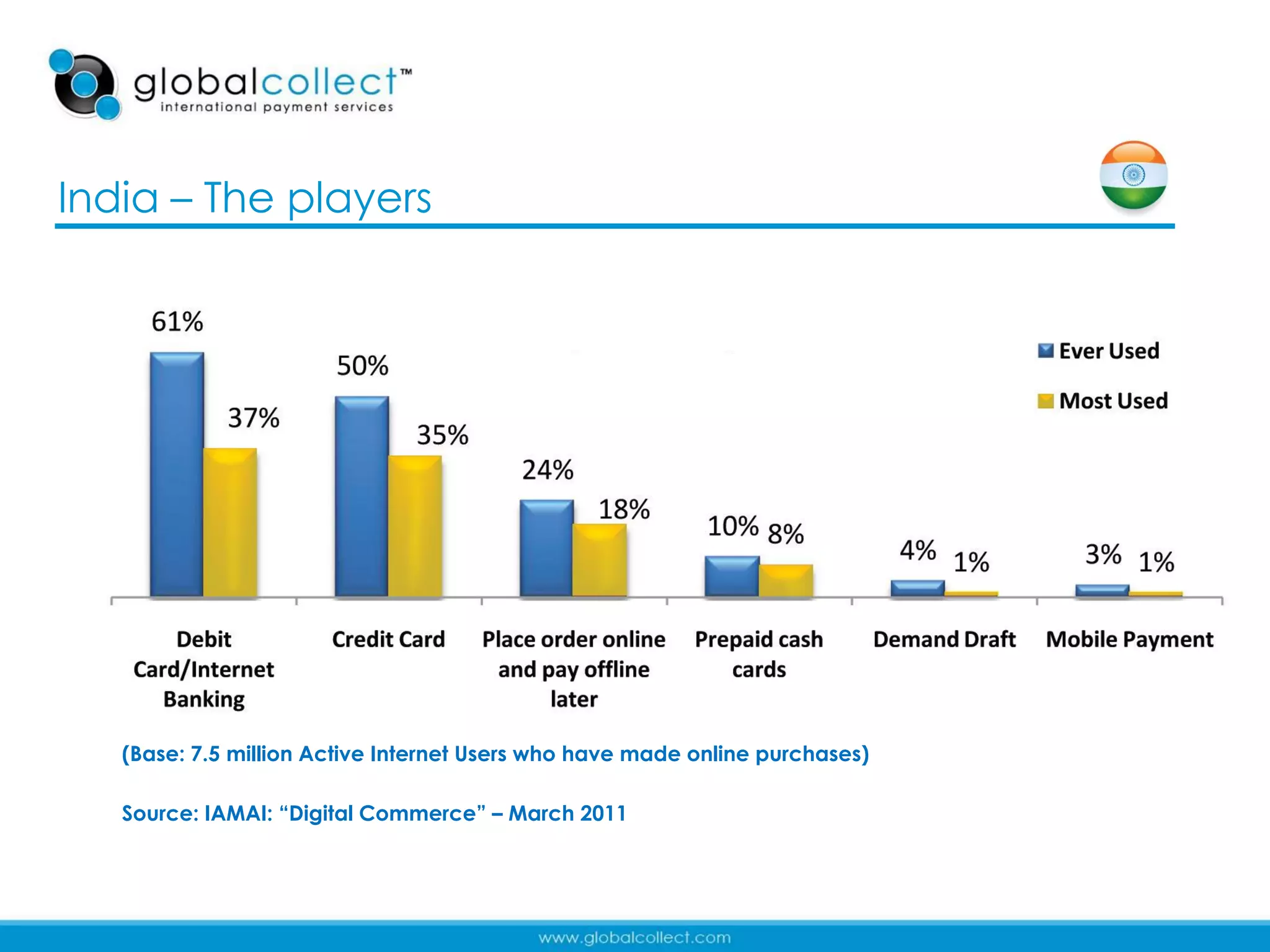

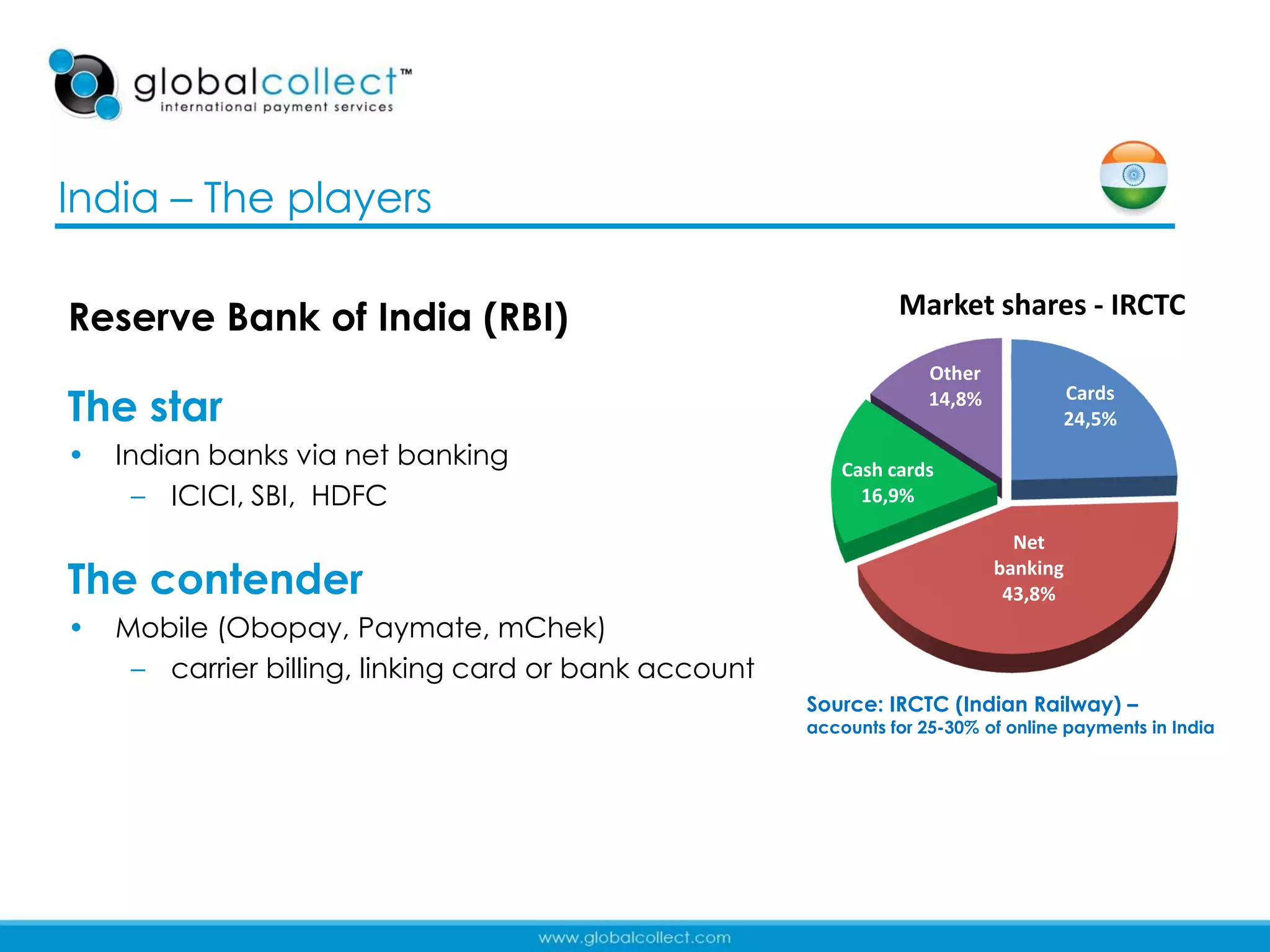

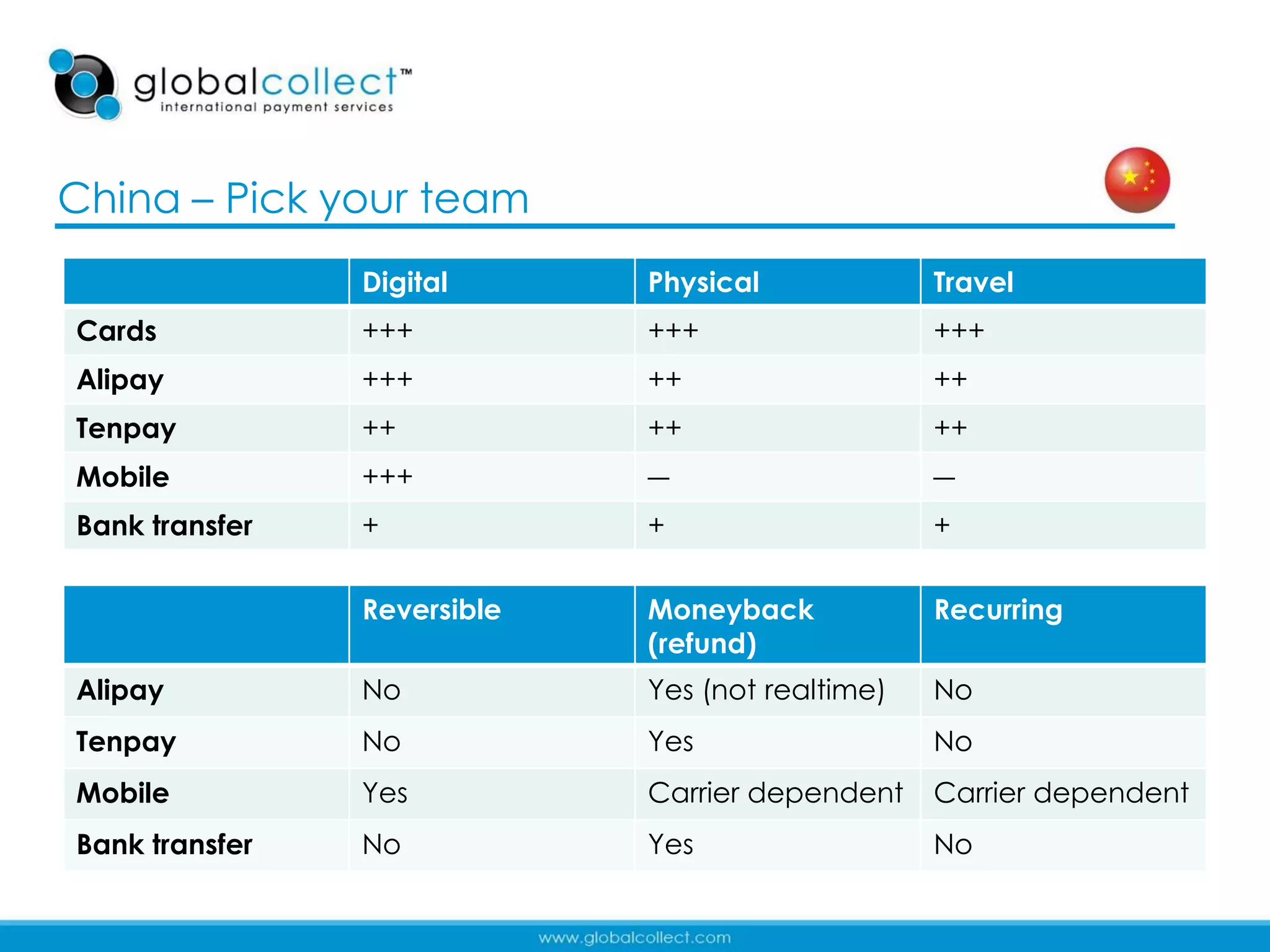

The document discusses payment strategies in the BRIC countries (Brazil, Russia, India, China), highlighting the unique challenges and opportunities in e-commerce for each market. It emphasizes the importance of local payment methods, regulations, and consumer behavior while providing insights into GDP per capita, e-commerce growth rates, and preferred payment methods. The document encourages businesses to adapt their strategies to align with local practices and regulatory environments for successful market entry.

![[SGPKOR] 결제사업자가 바라본 소셜게임의 현재와 미래](https://cdn.slidesharecdn.com/ss_thumbnails/a13-globalcollect-110326122601-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)