Downloaded 131 times

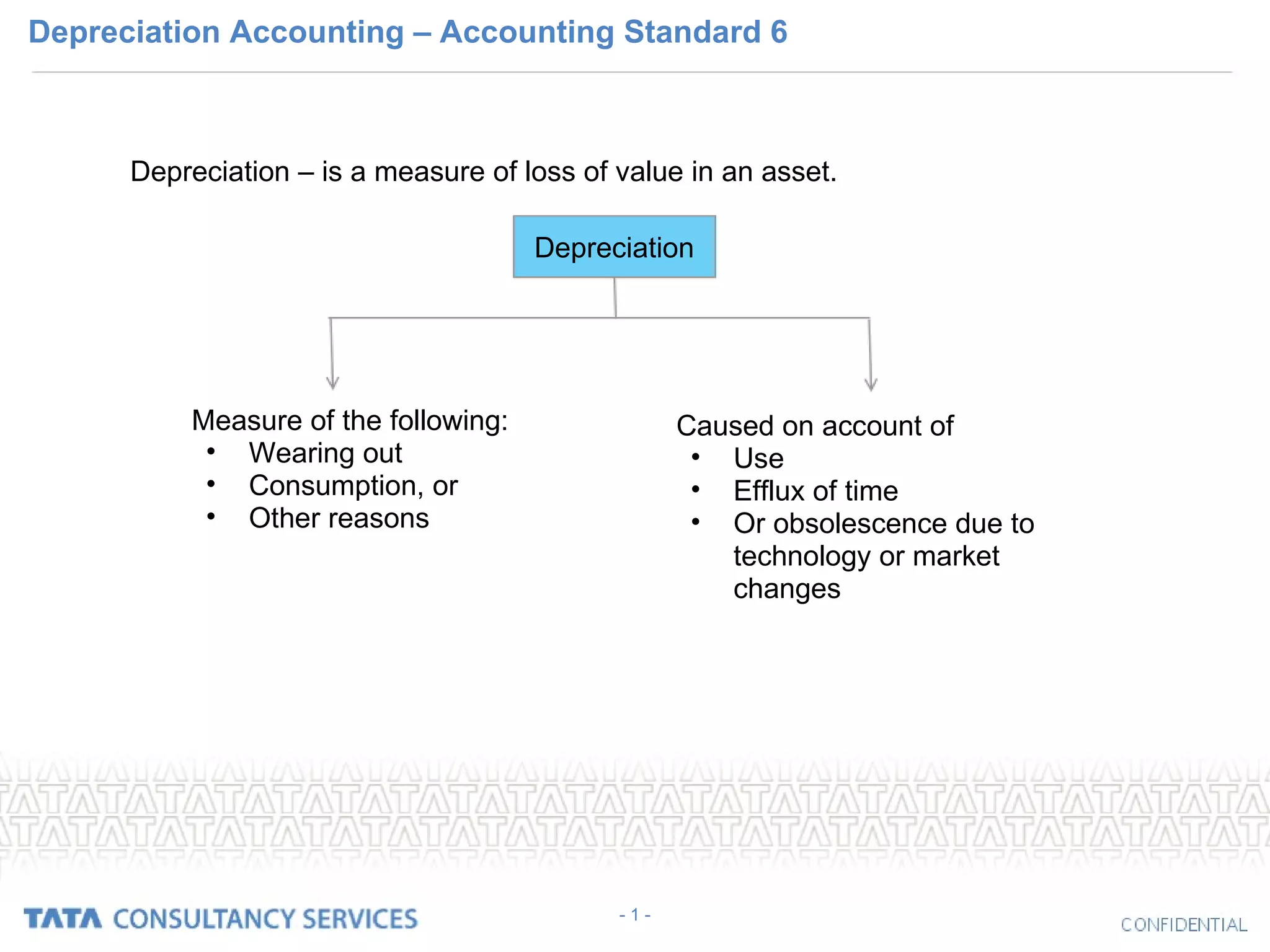

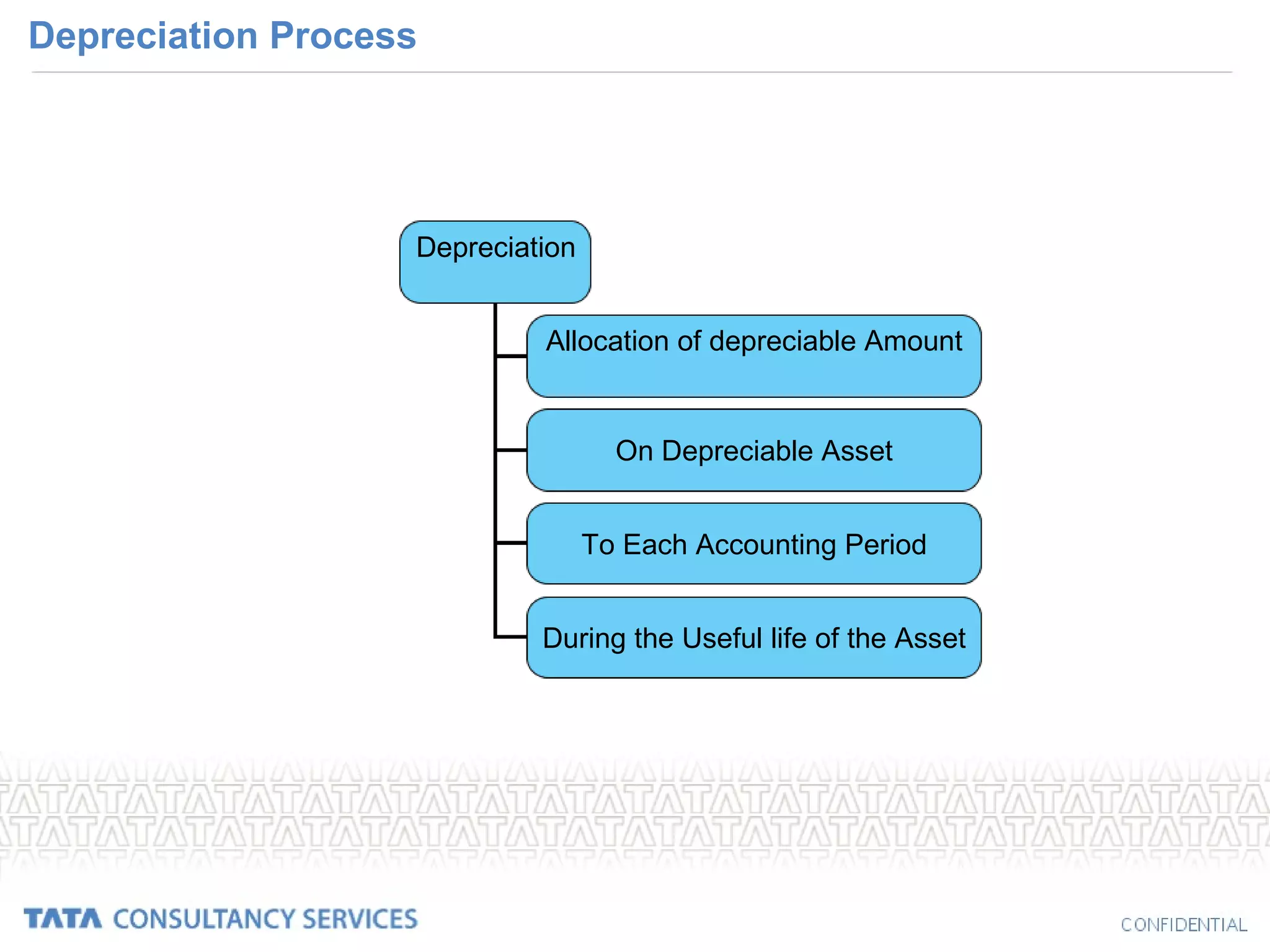

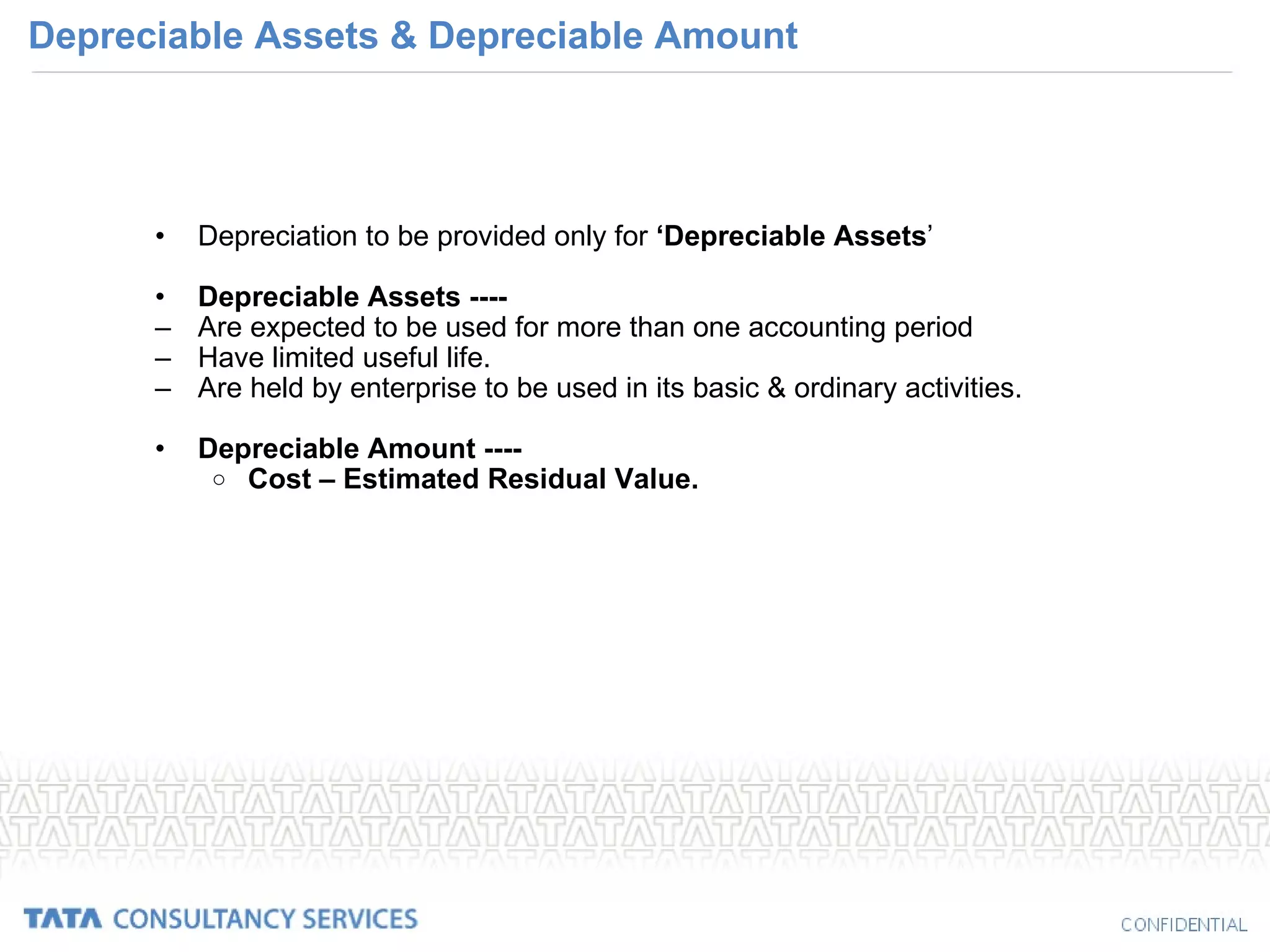

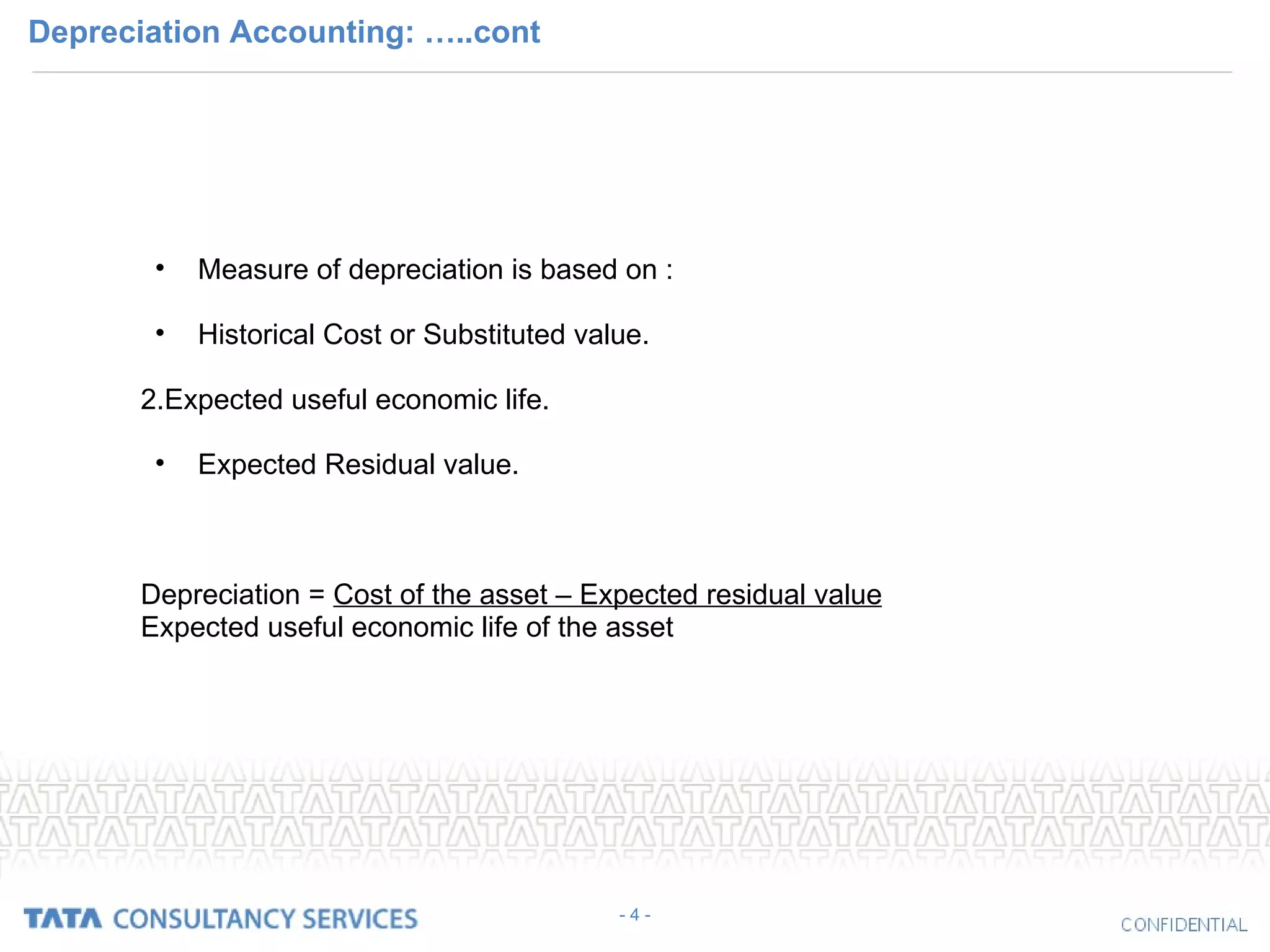

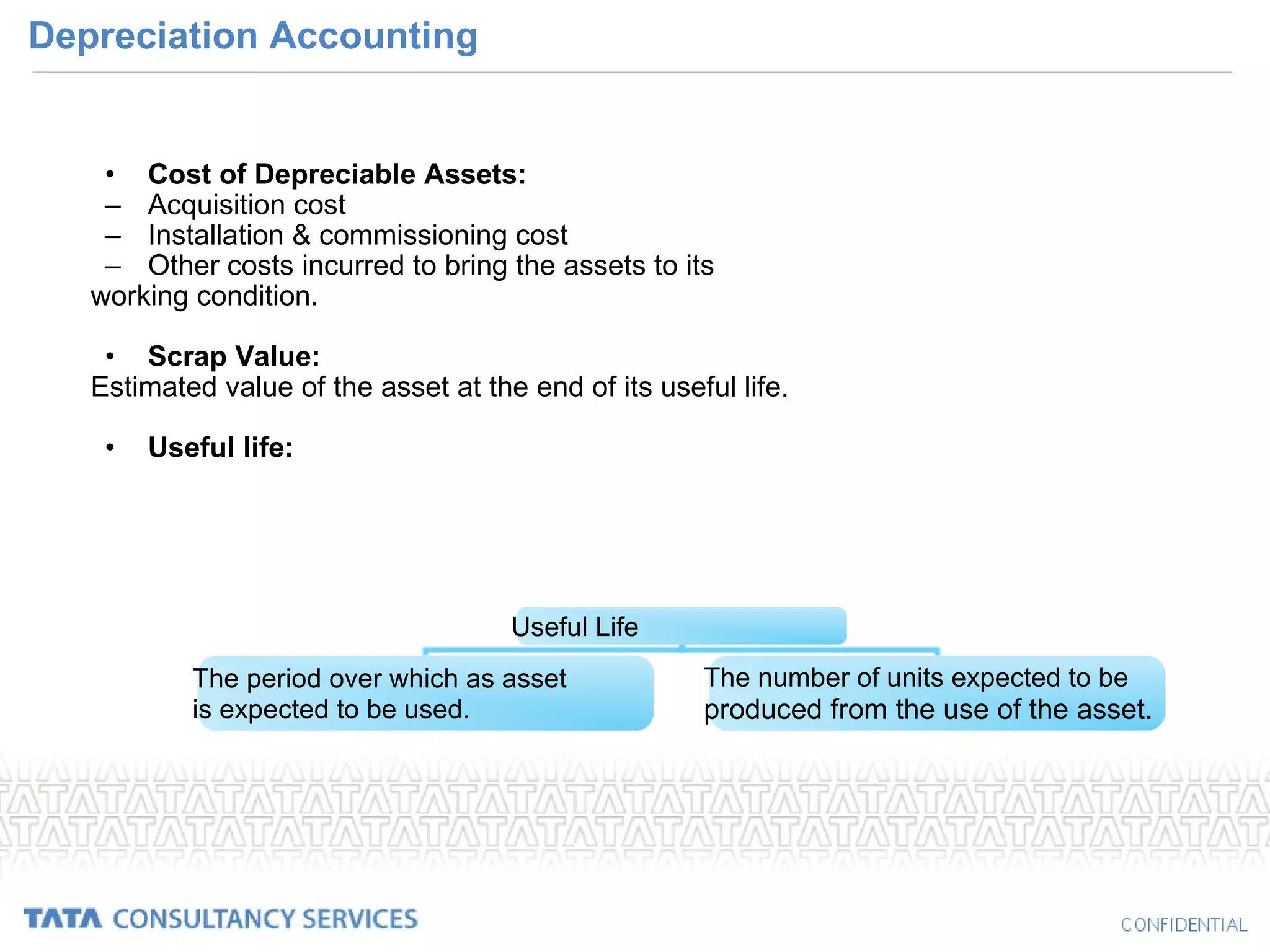

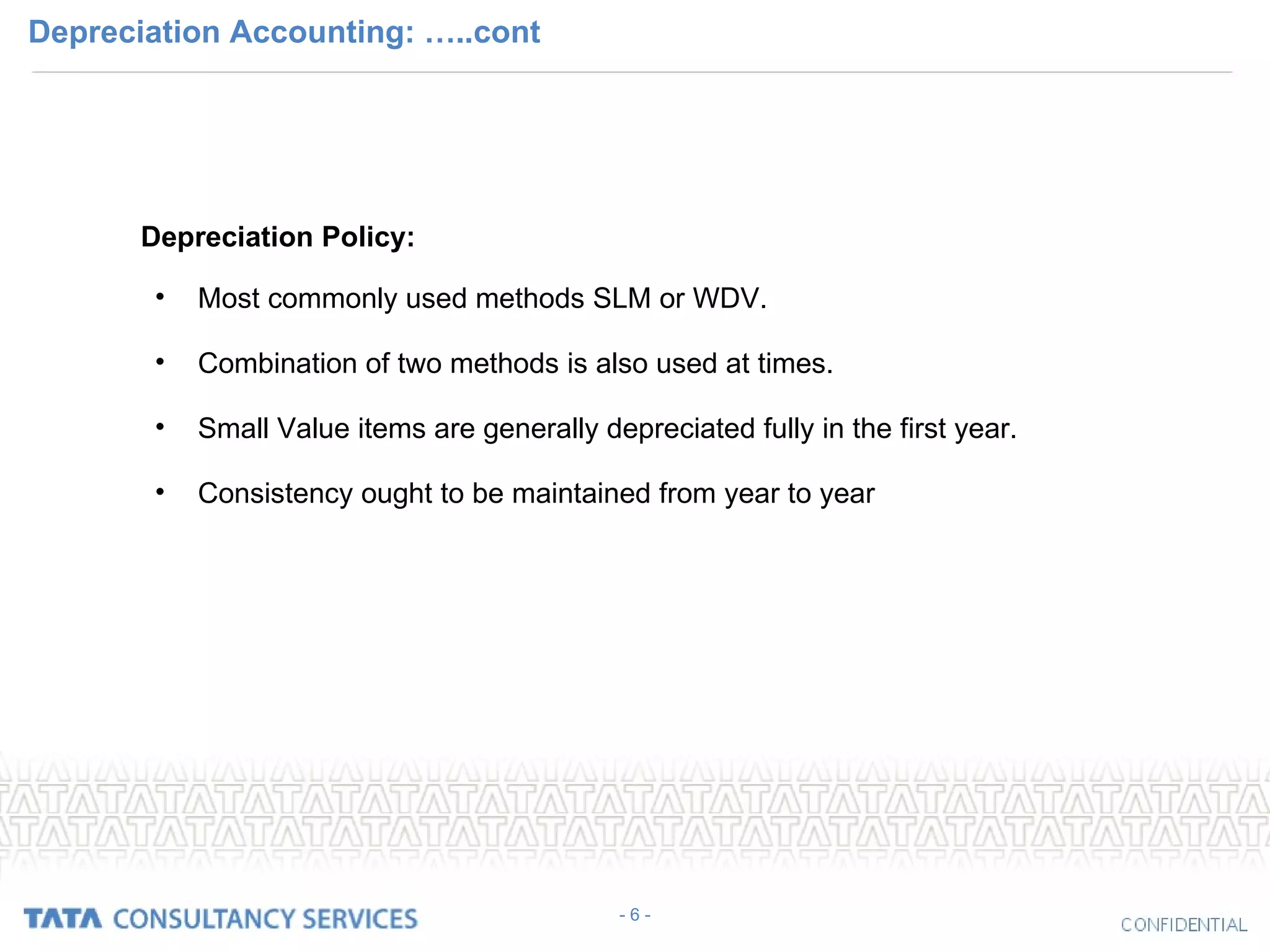

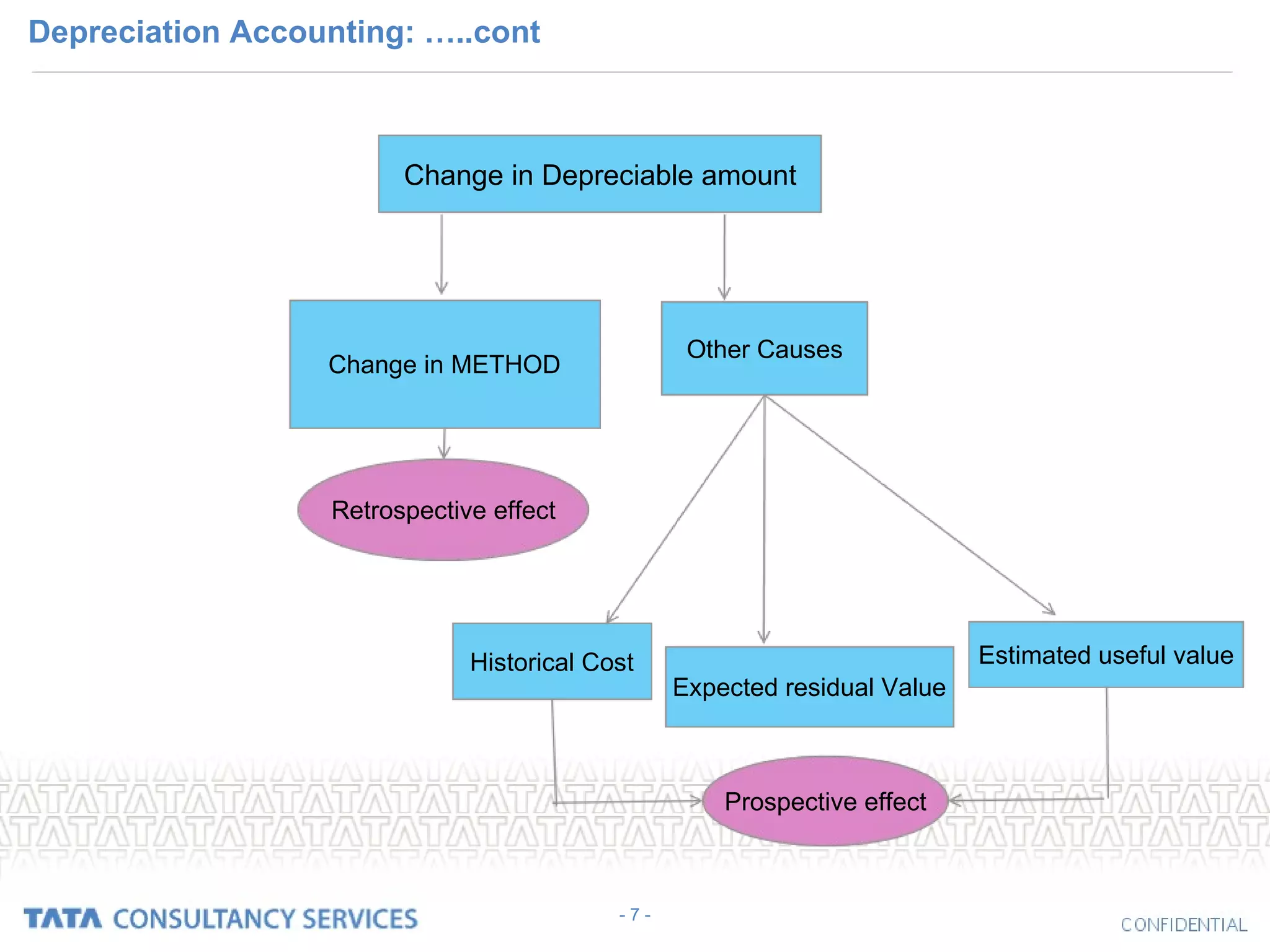

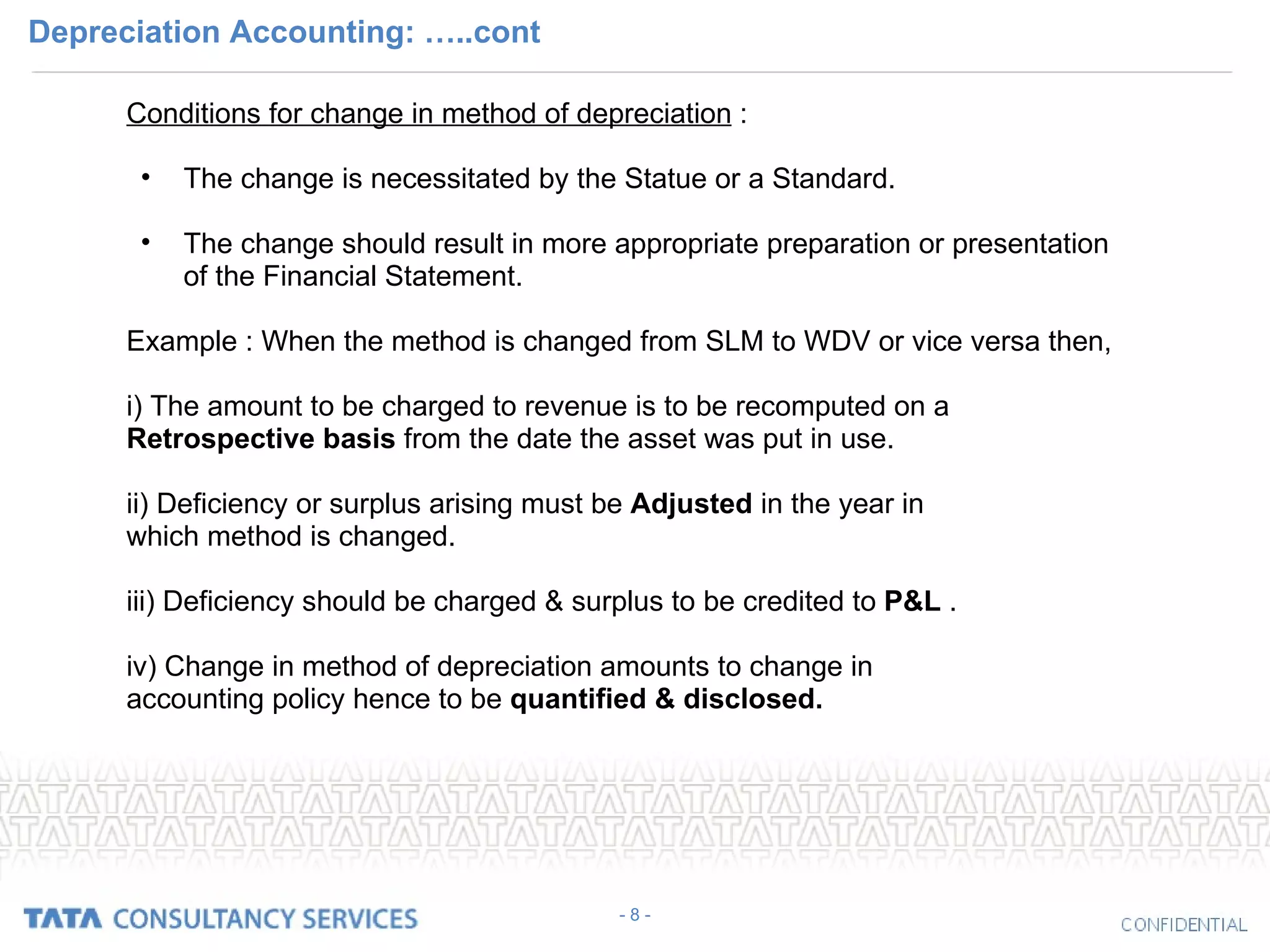

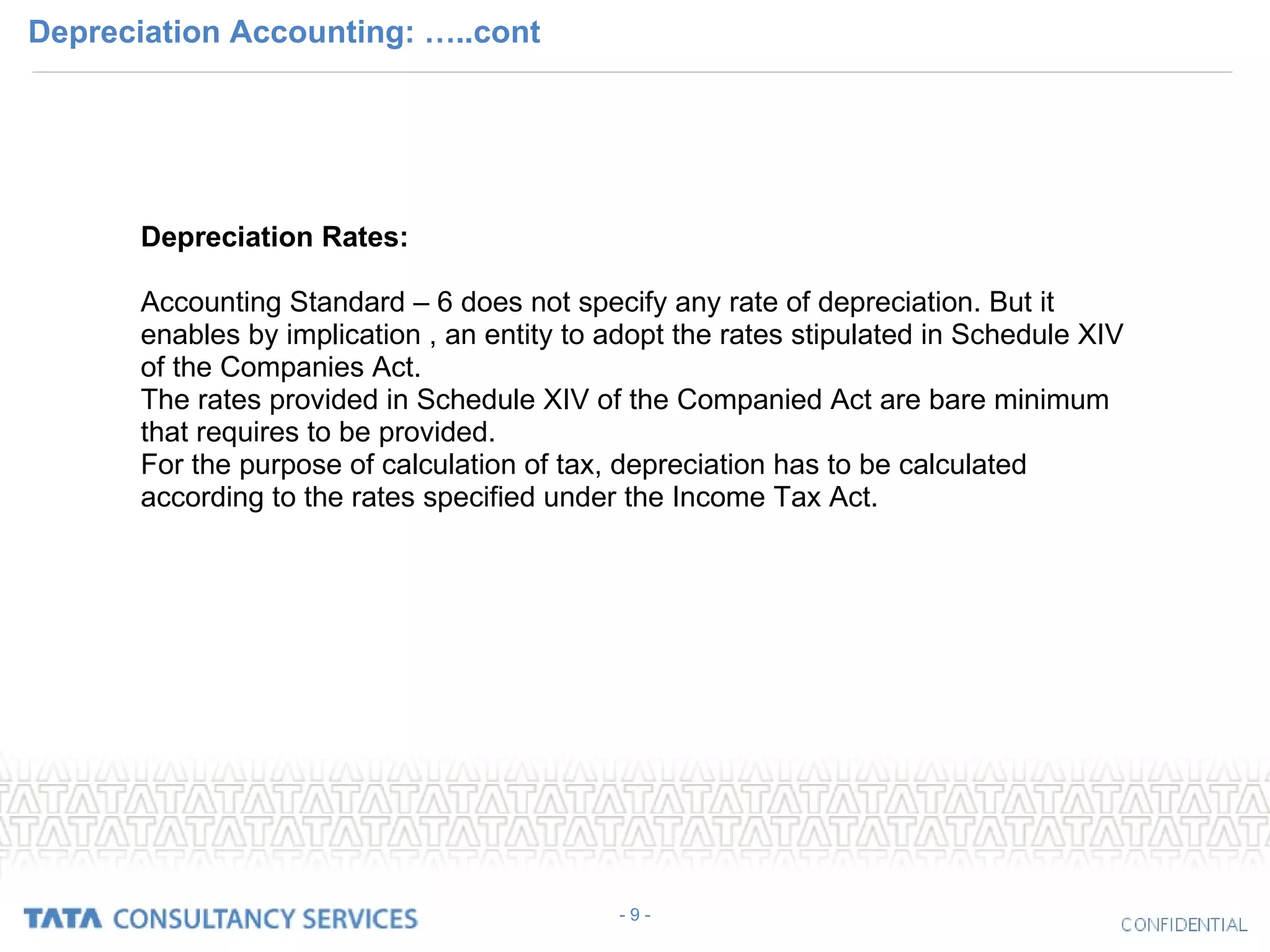

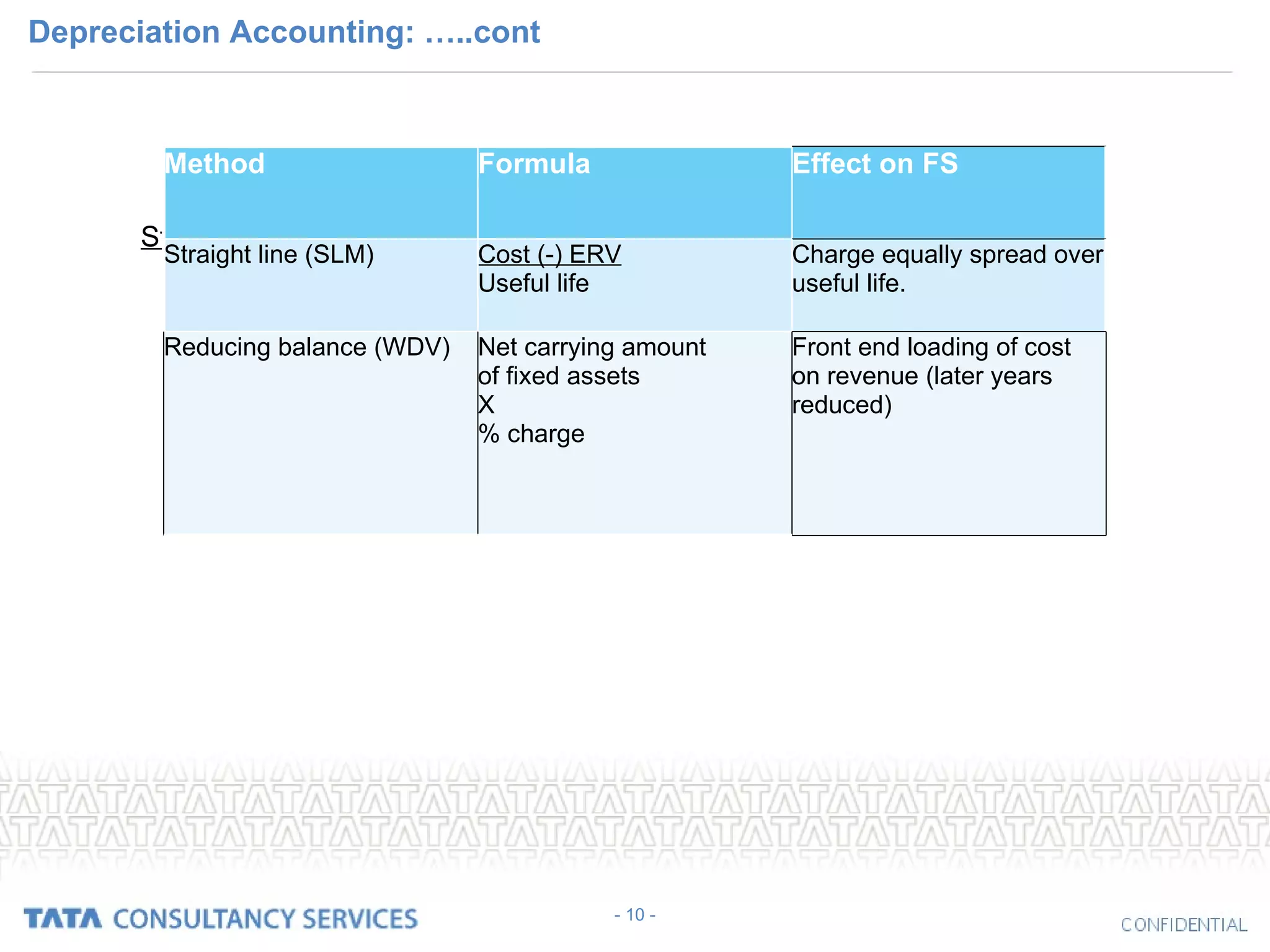

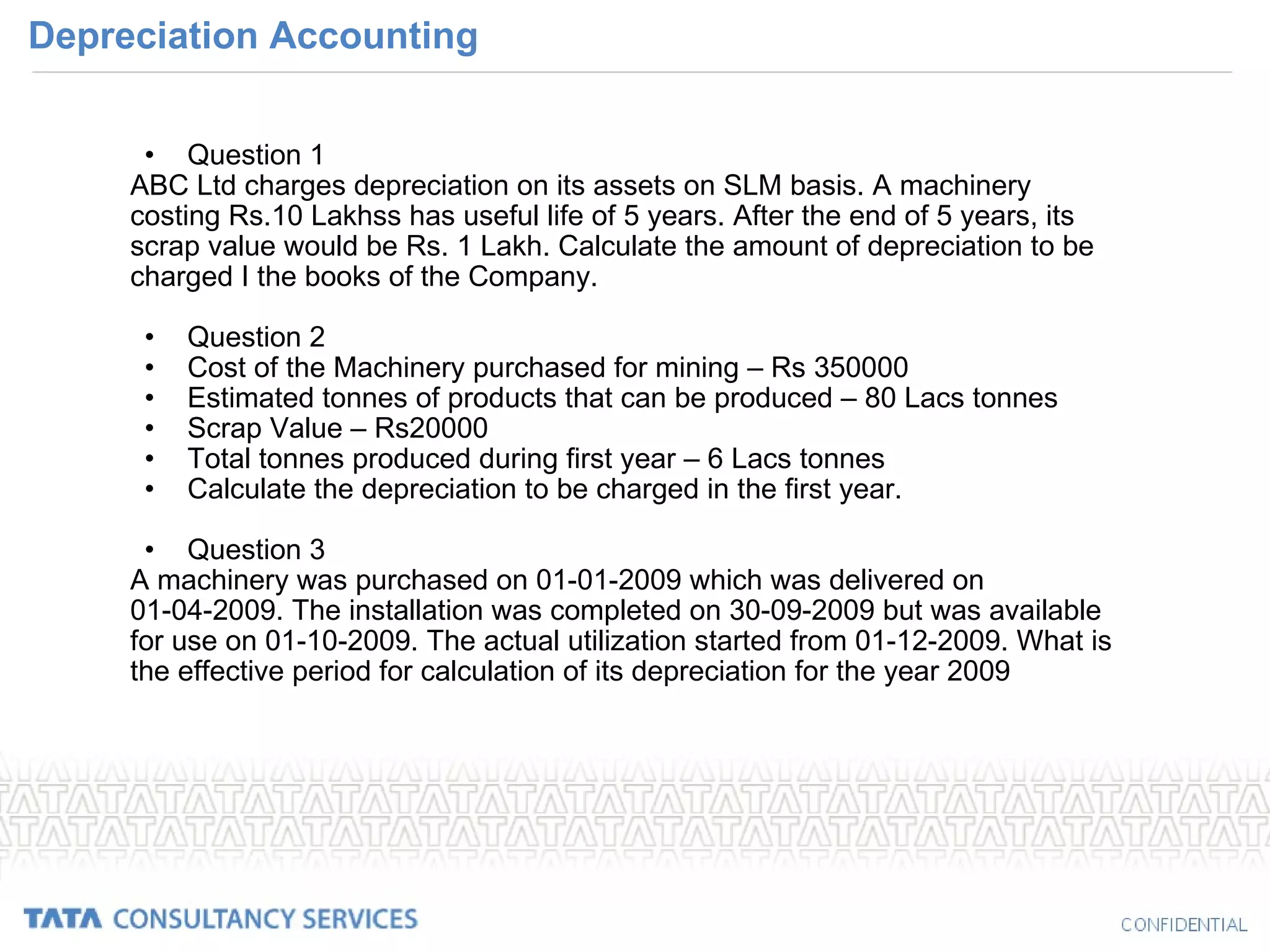

The document discusses depreciation accounting concepts including: 1) Depreciation is the allocation of the cost of a tangible asset over its useful life. It measures the loss of value from wear, tear, obsolescence, and age. 2) Depreciable assets have a limited useful life and are used in business operations for more than one accounting period. Depreciation is calculated based on historical cost, useful life, and expected residual value. 3) Common depreciation methods include straight-line and reducing balance, which have different impacts on financial statements over the asset's life. Accounting standards provide guidance but don't specify depreciation rates.