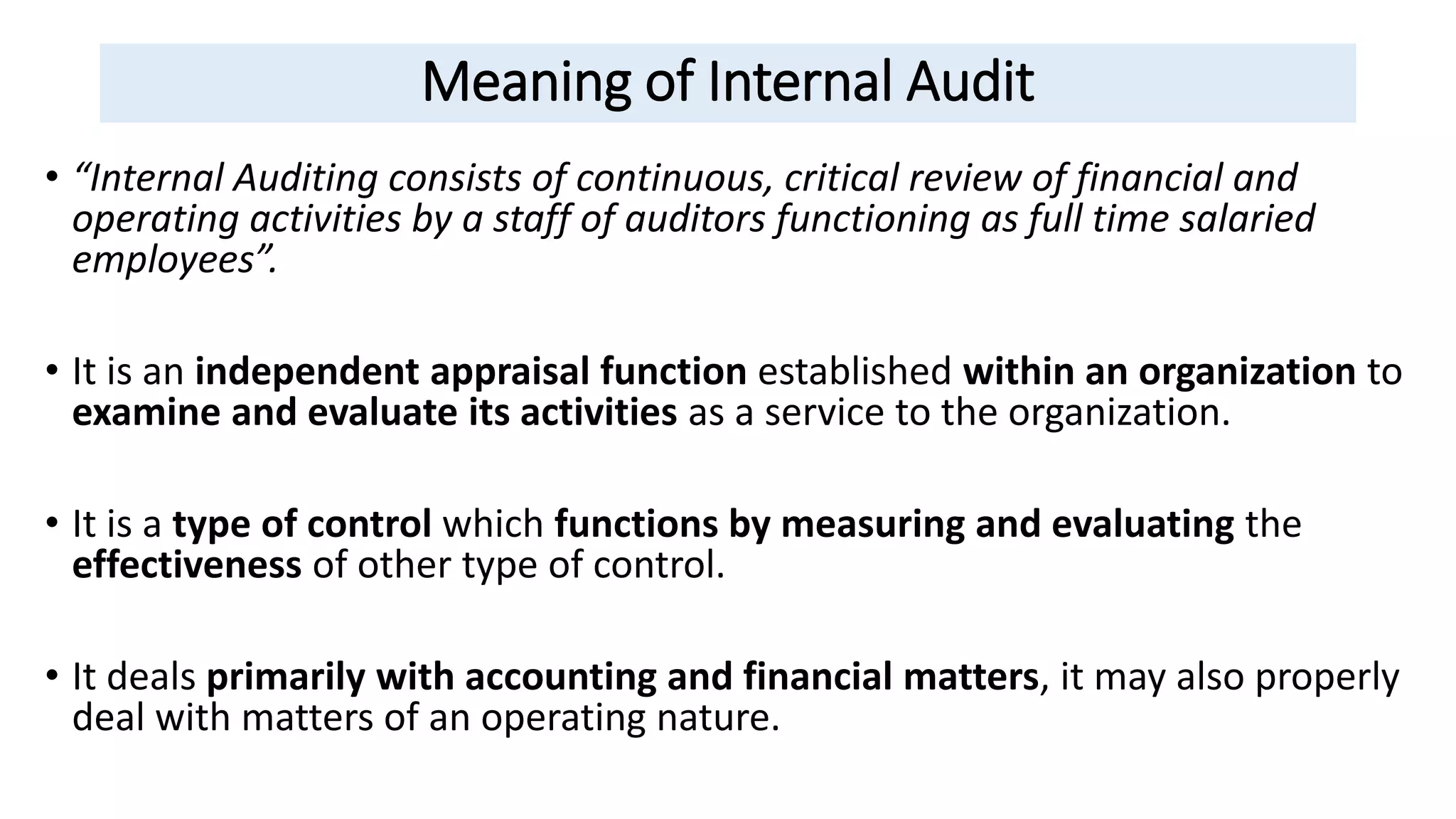

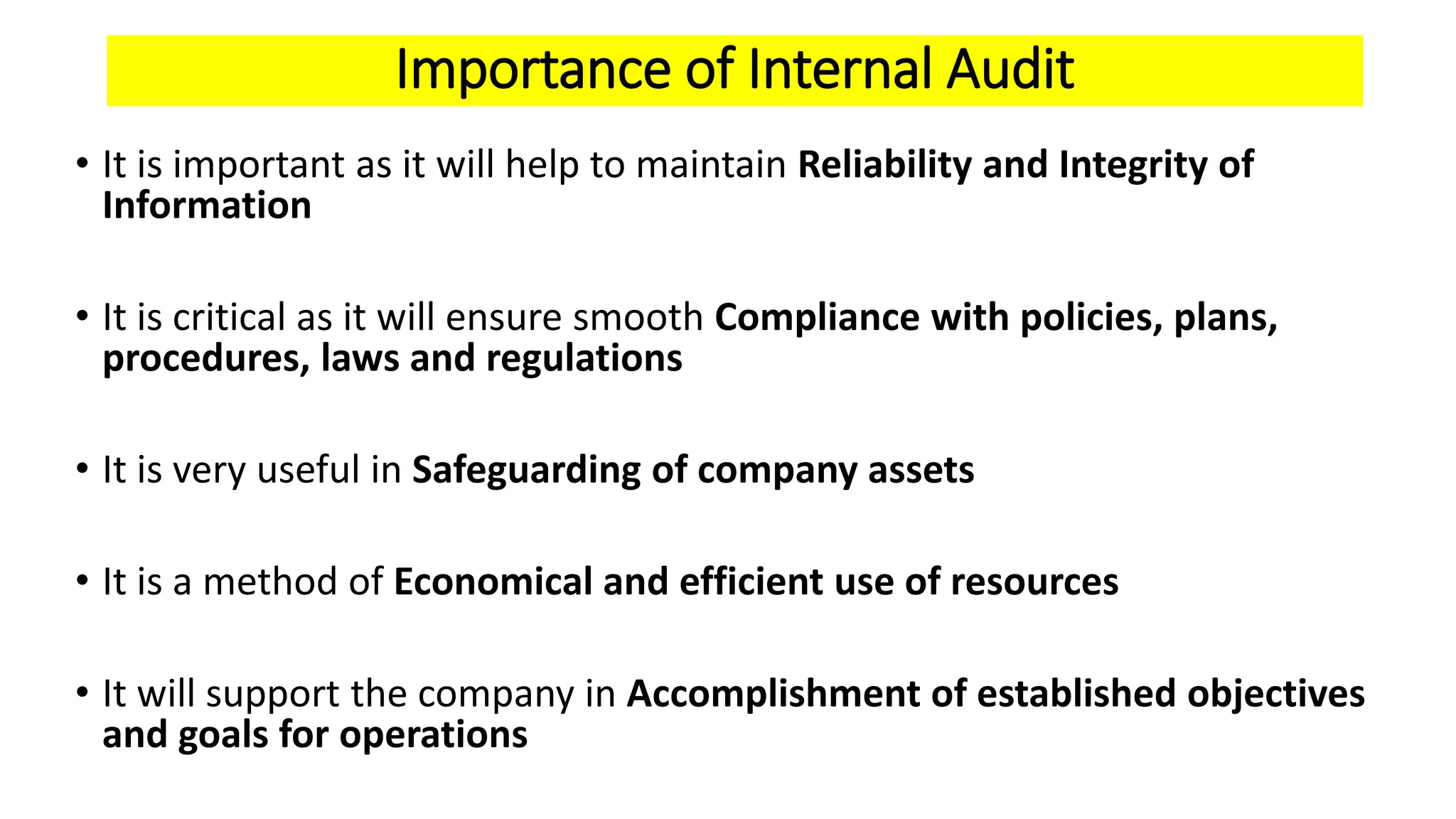

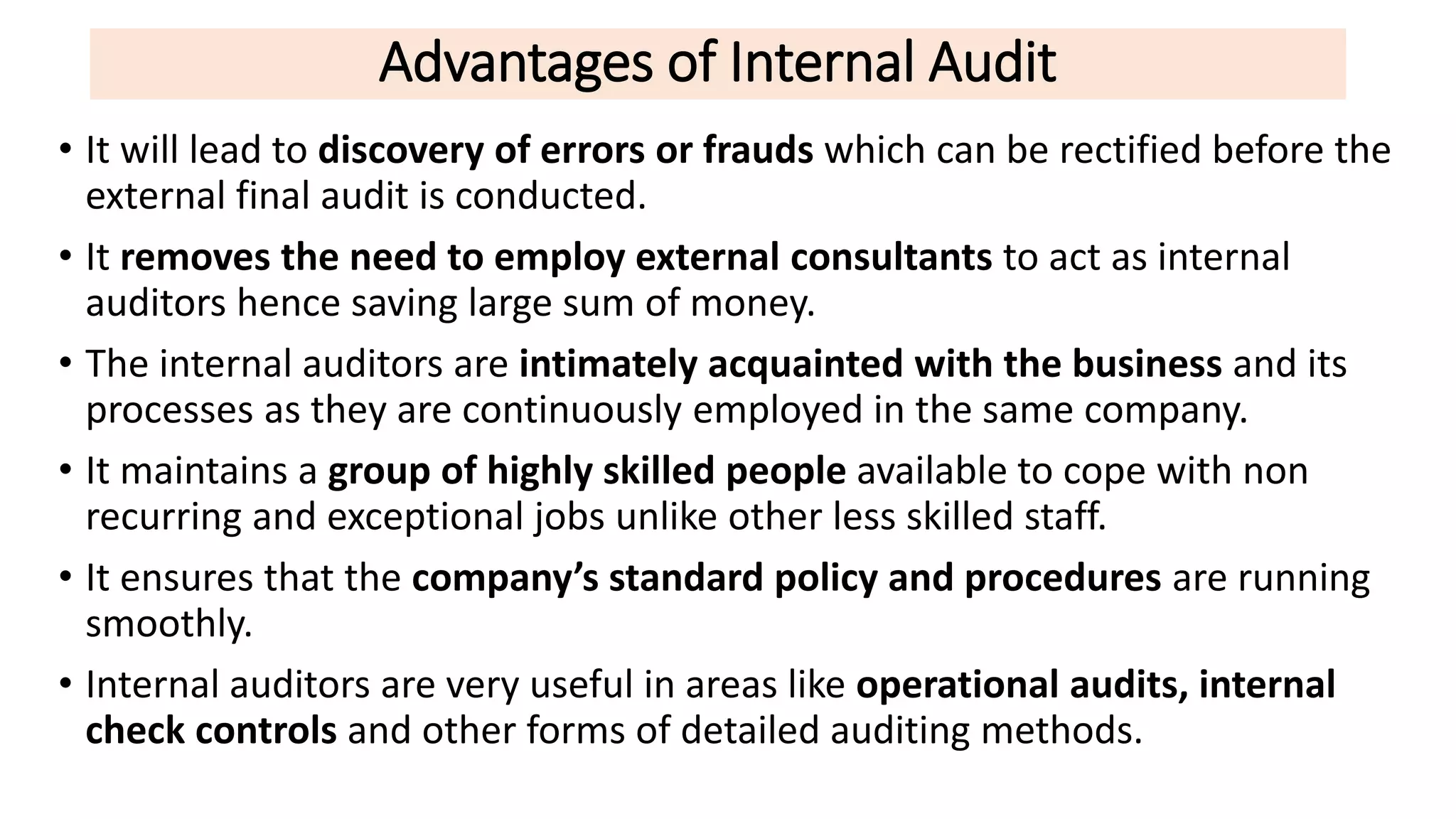

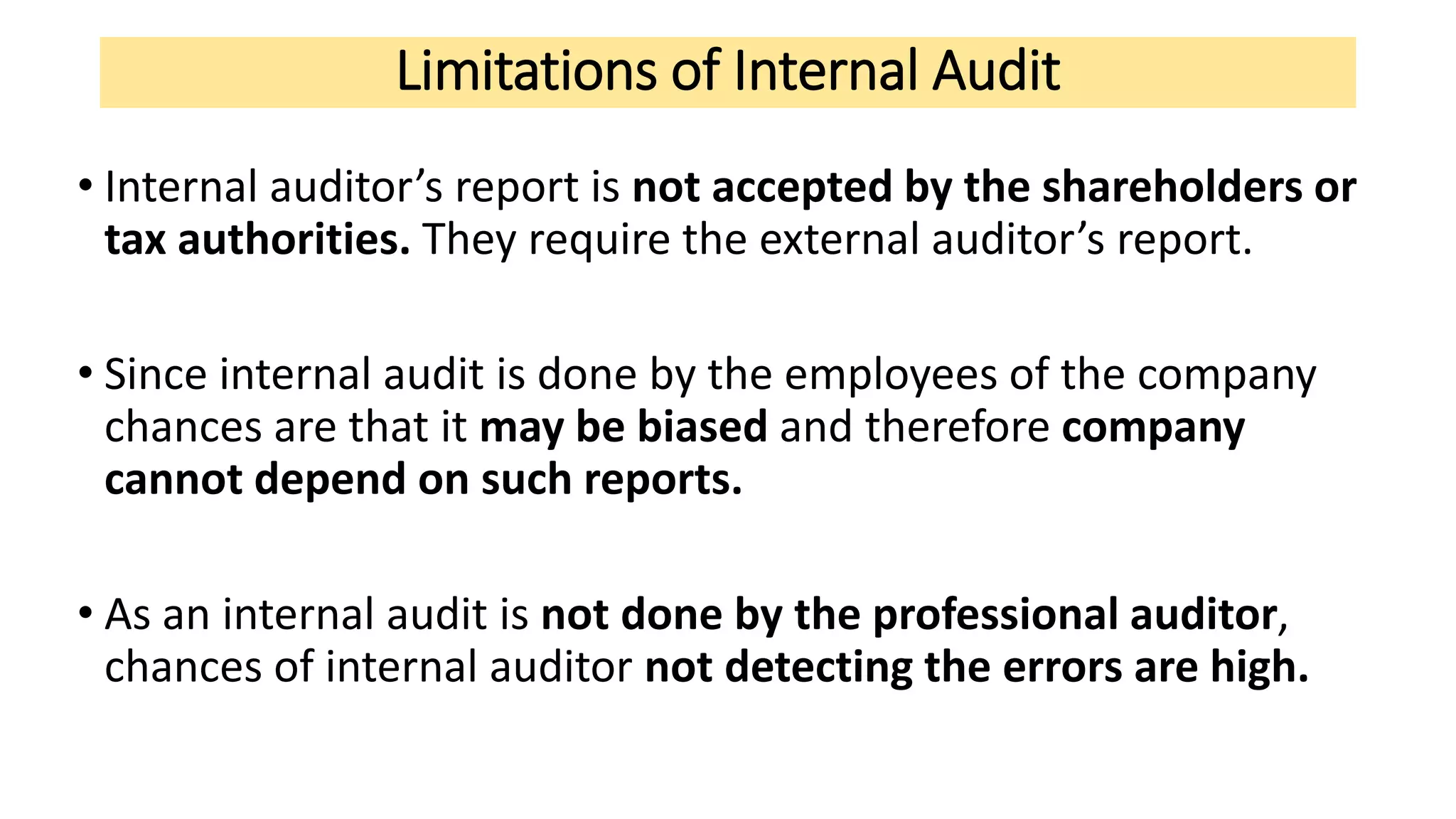

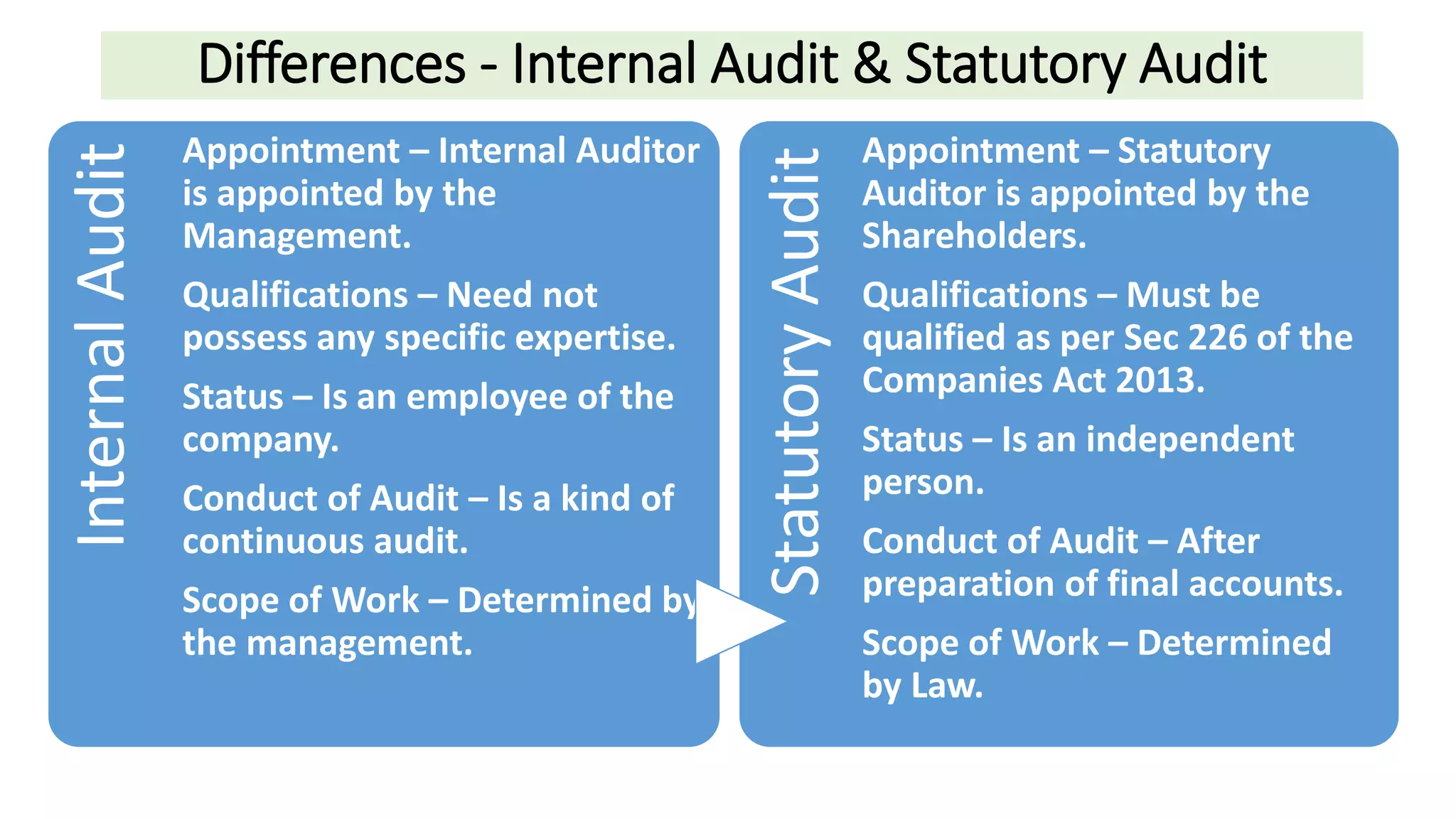

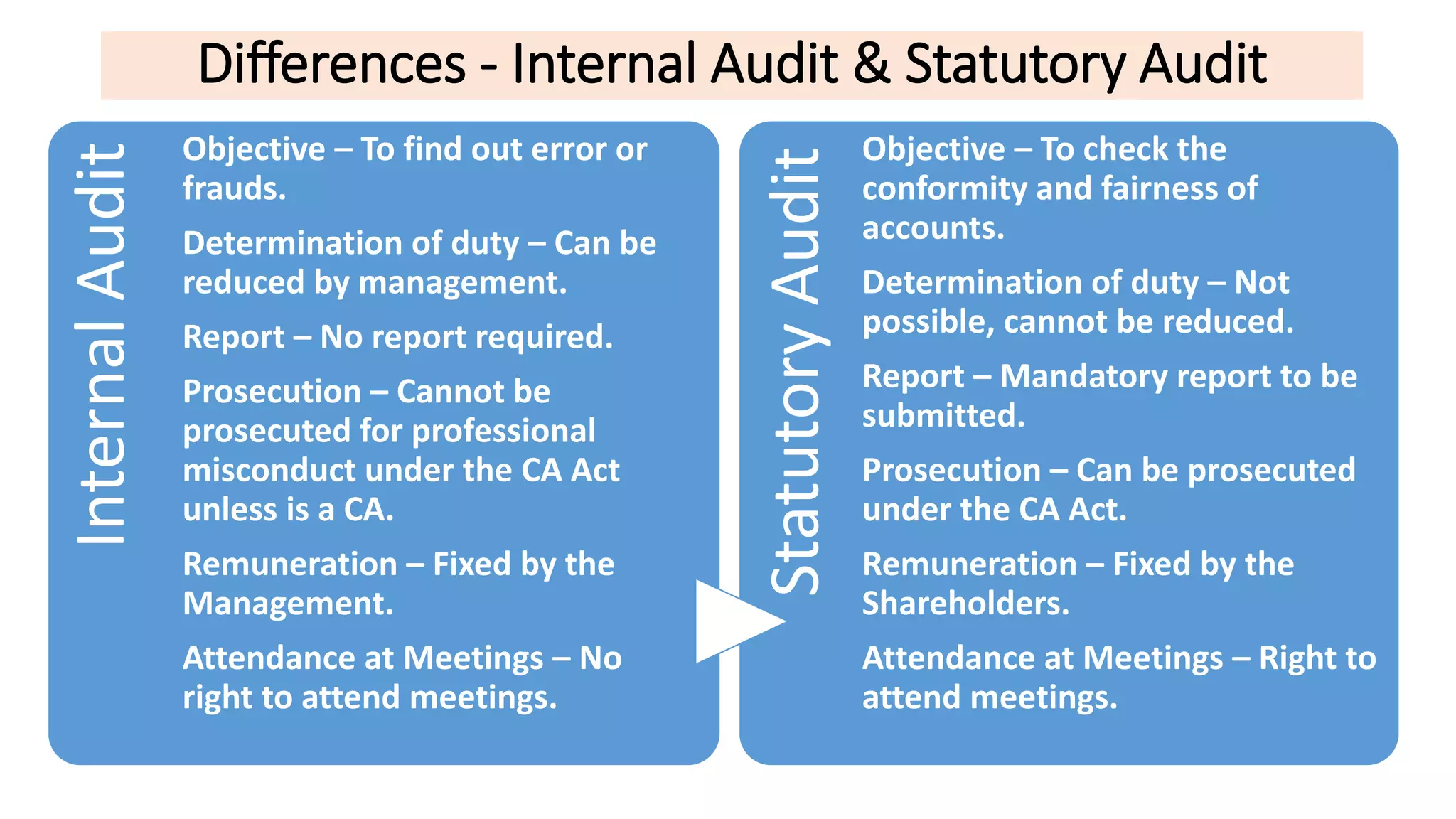

This document outlines the principles and practices of internal auditing, including its meaning, importance, advantages, limitations, and differences from statutory audit. Internal auditing is described as a continuous review function performed by employees to help organizations maintain reliability and compliance, while also uncovering errors and saving costs. The document also highlights key distinctions between internal and statutory audits in terms of appointment, qualifications, scope, and reporting requirements.