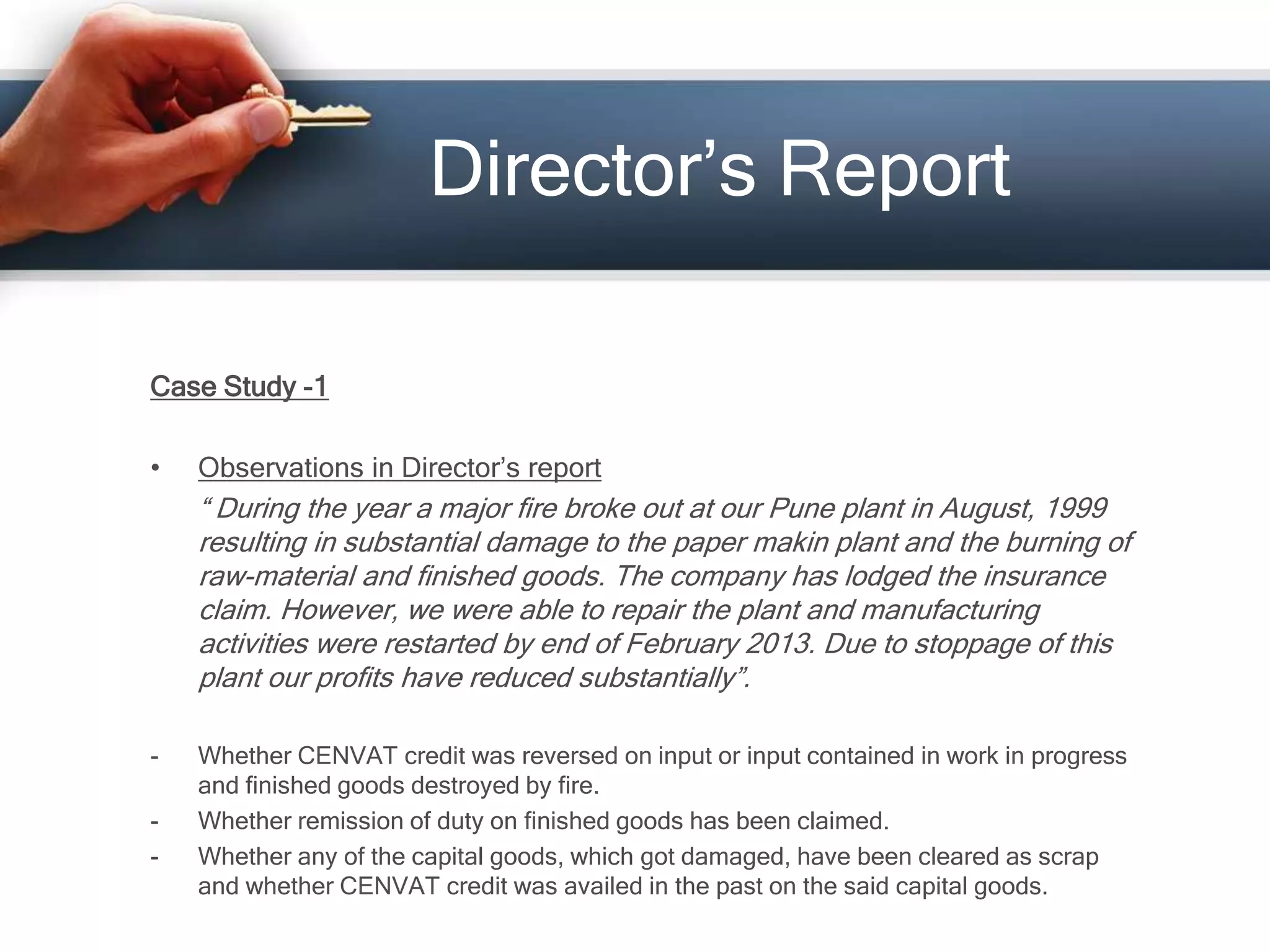

The document summarizes key aspects of financial statements that should be reviewed during an audit, including the director's report, notes, trial balance, and balance sheet. It provides examples of items to examine, such as details on inventory valuation, treatment of damaged goods, capital expenditures, related party transactions, and credit availment. The presentation emphasizes reviewing ratios, prior period expenses, service tax payments, and information in the tax audit report to thoroughly evaluate the financials.