Downloaded 11 times

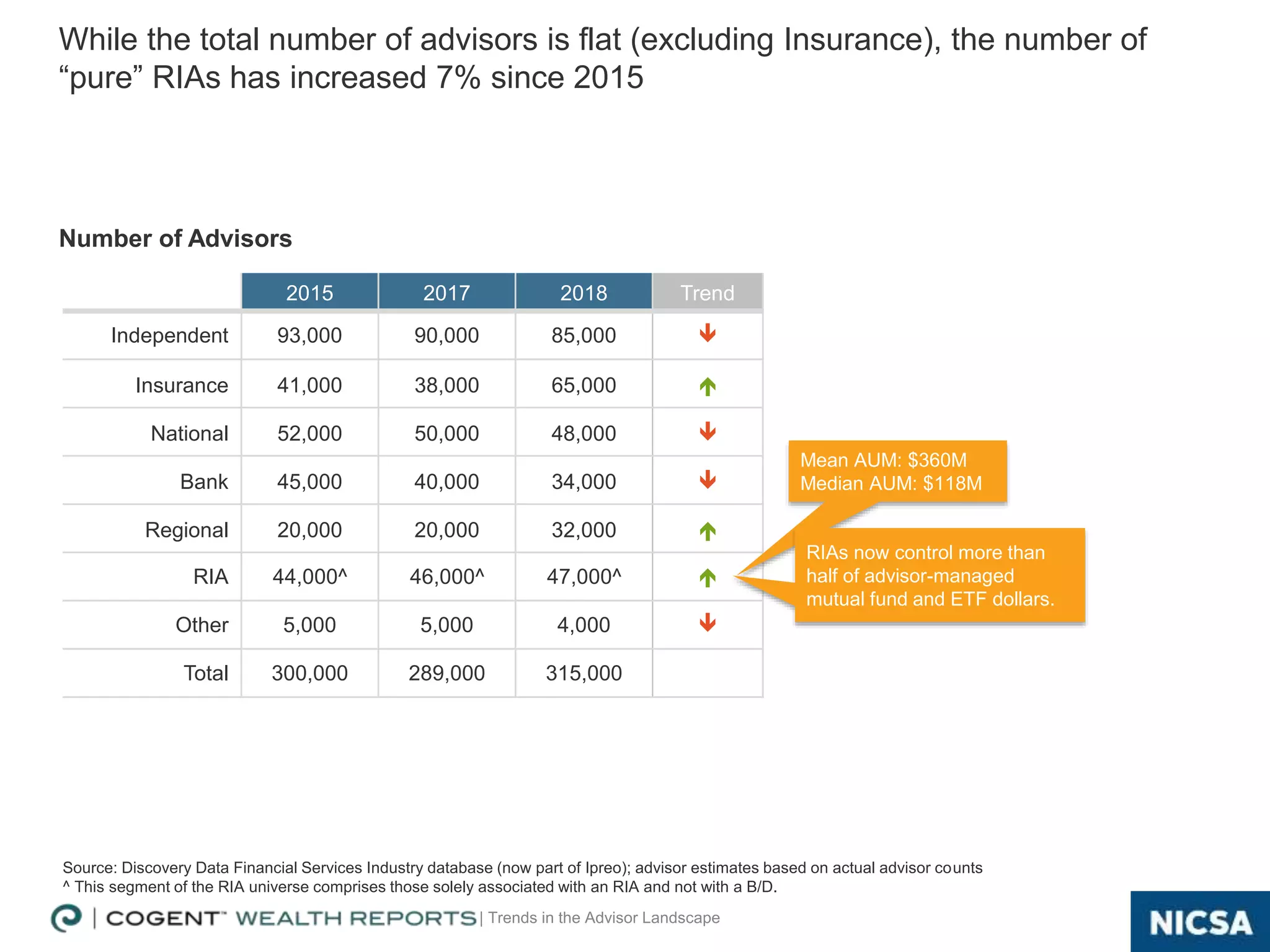

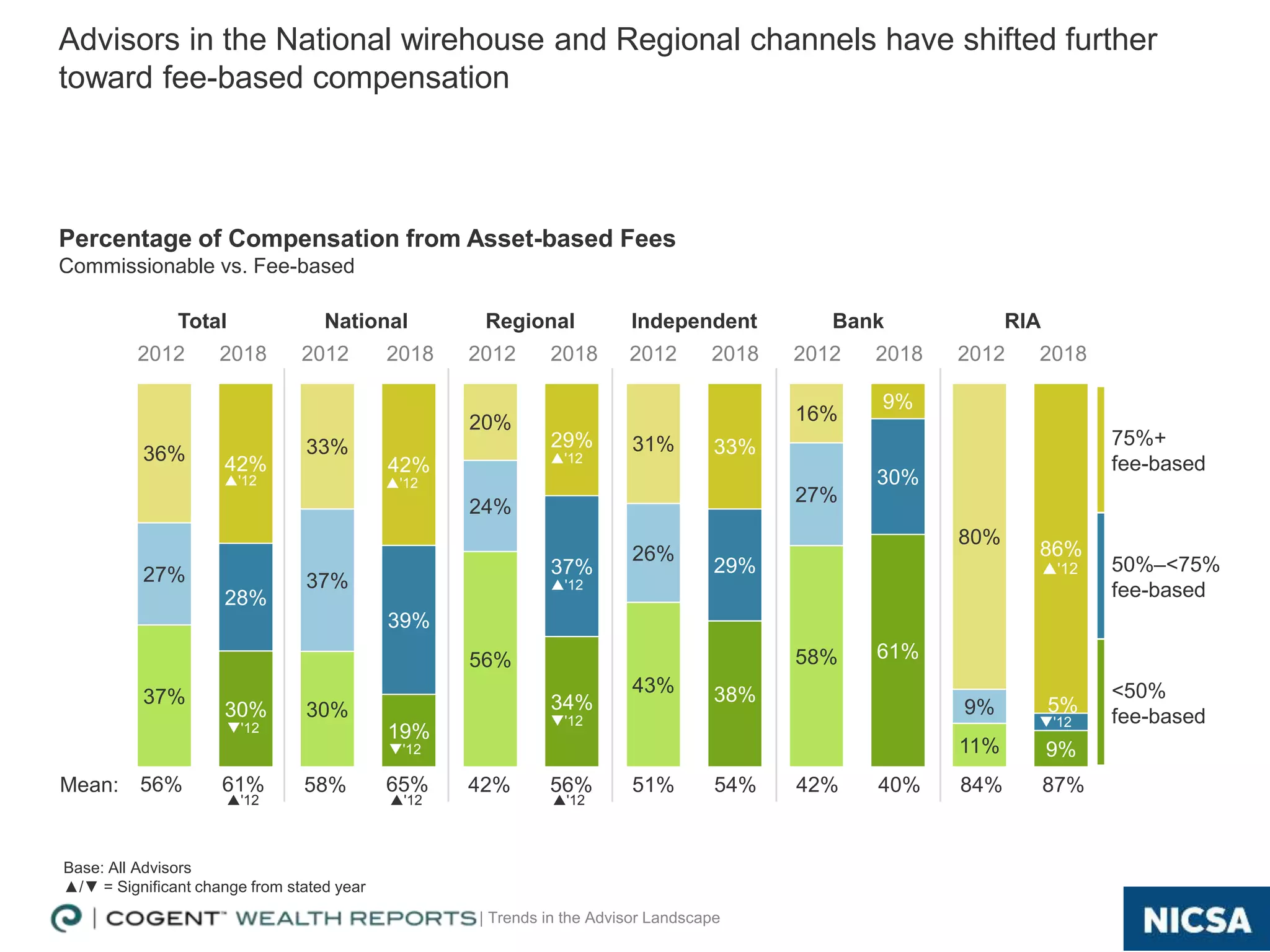

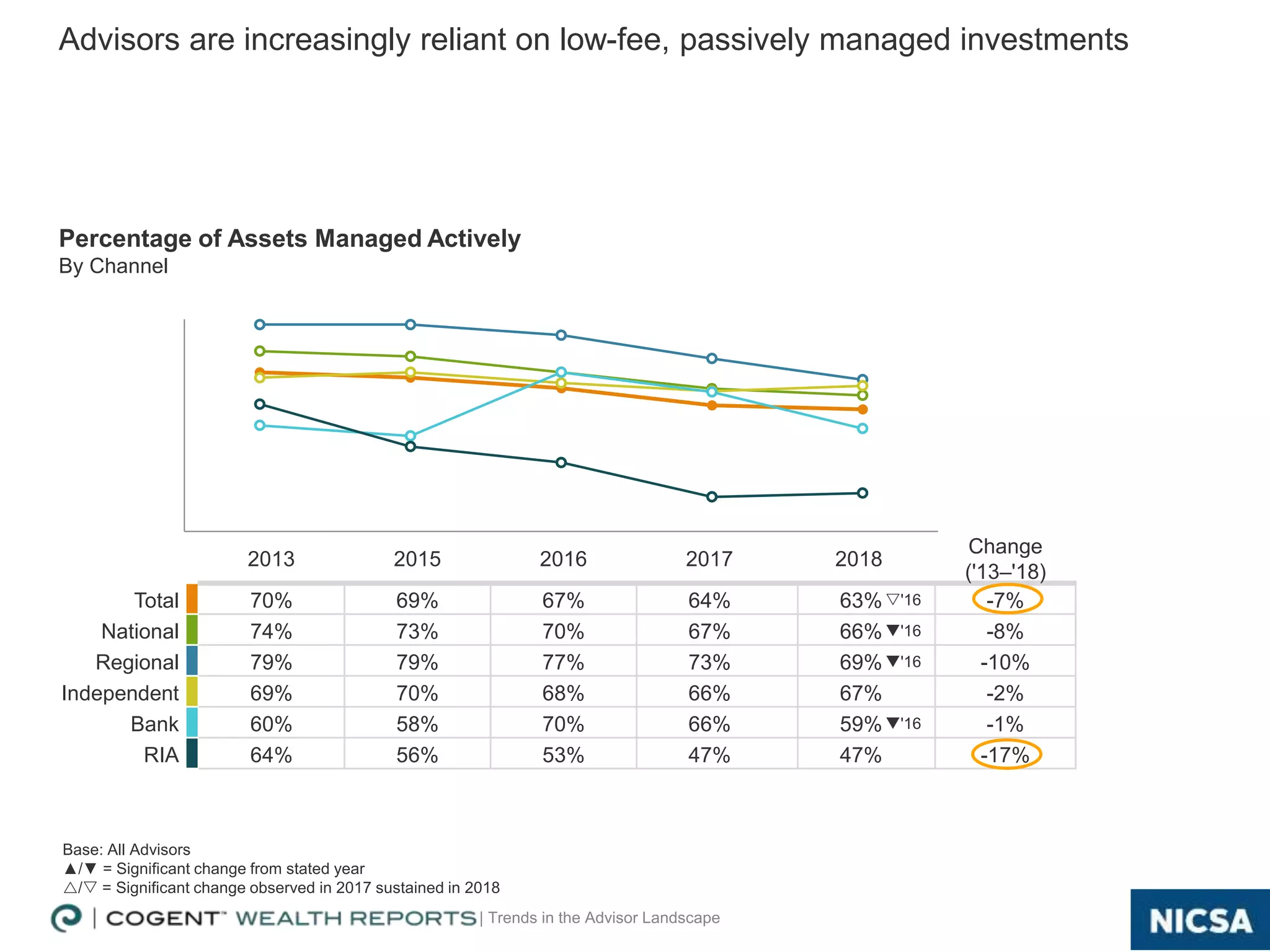

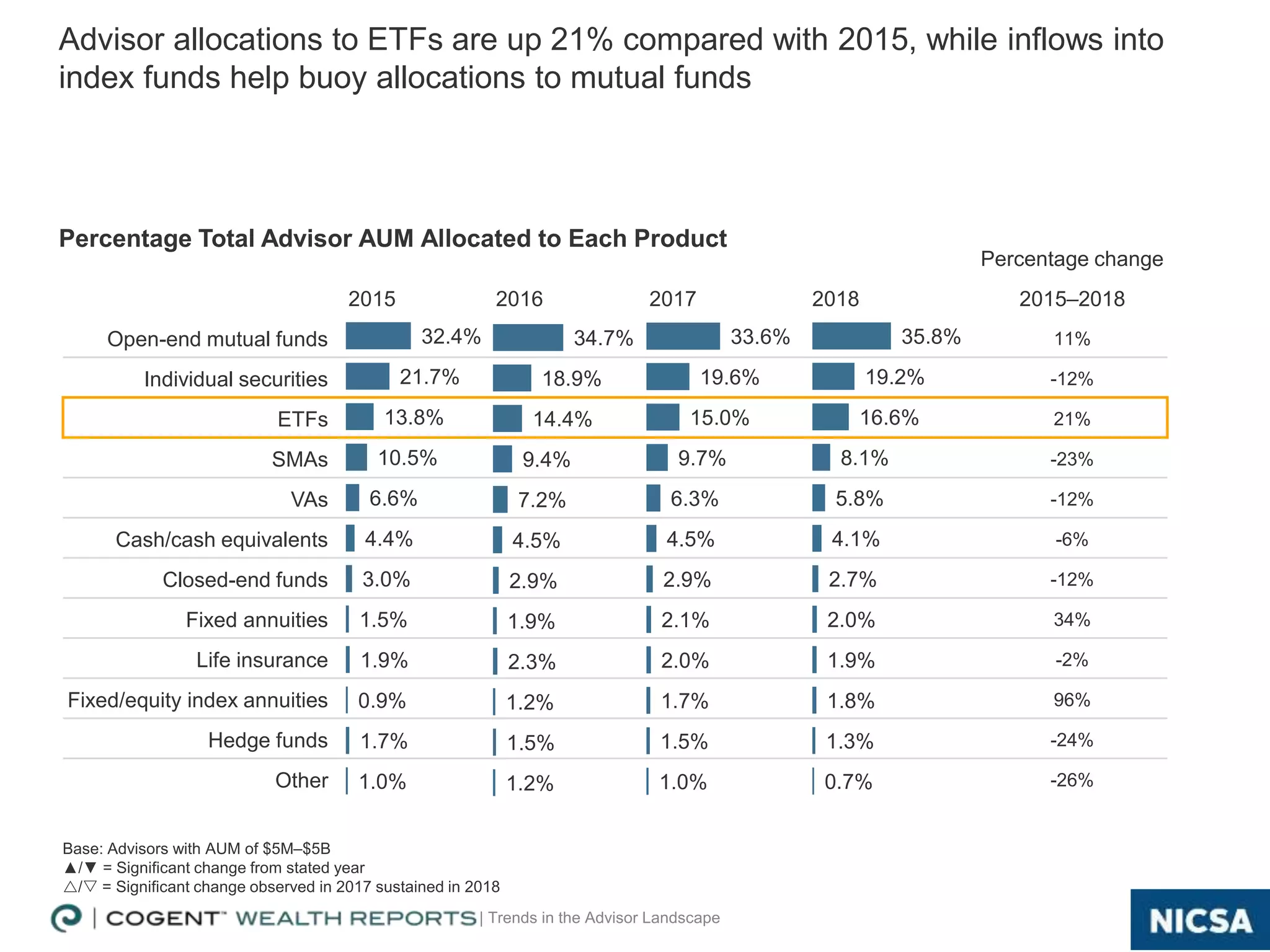

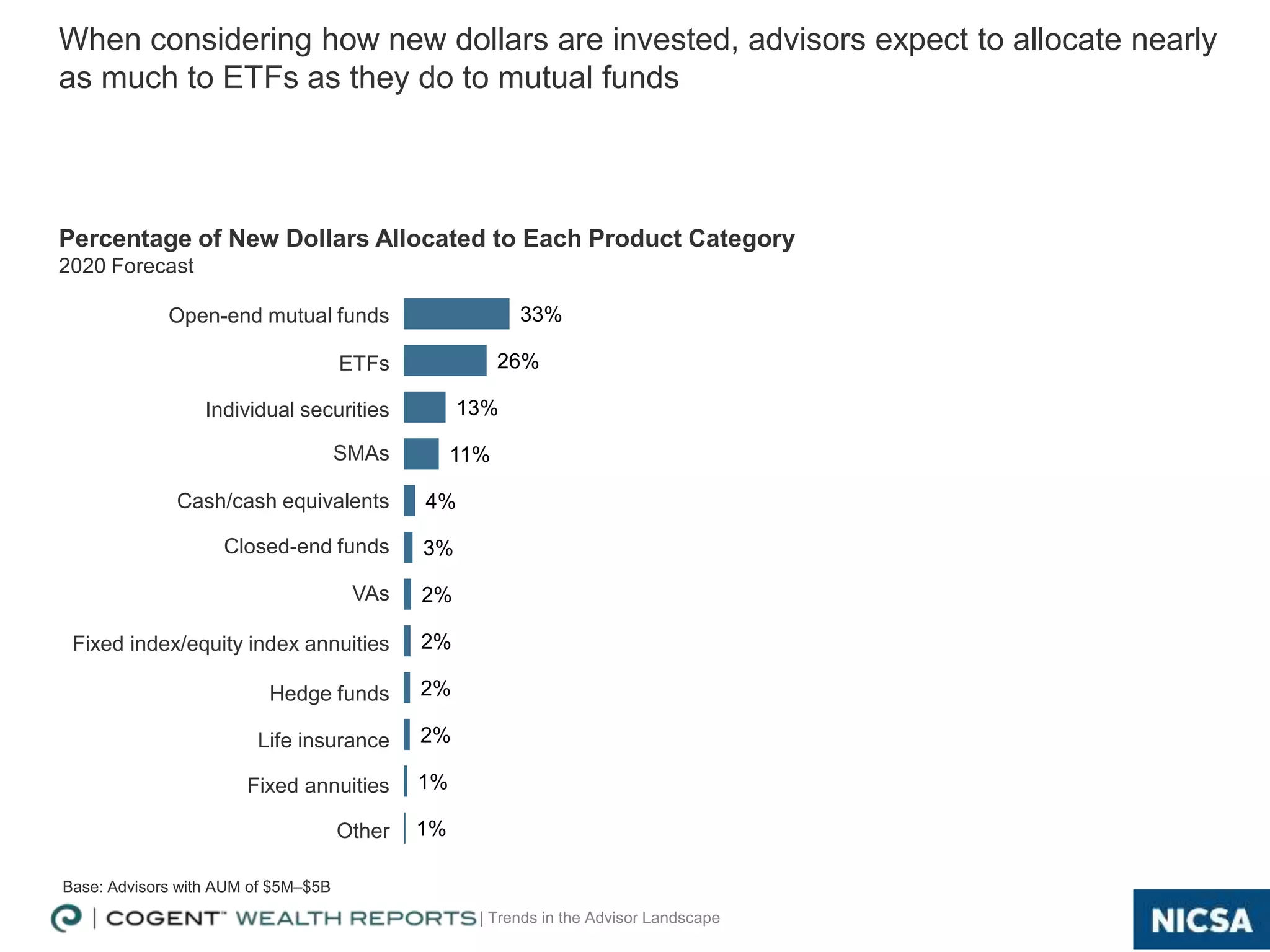

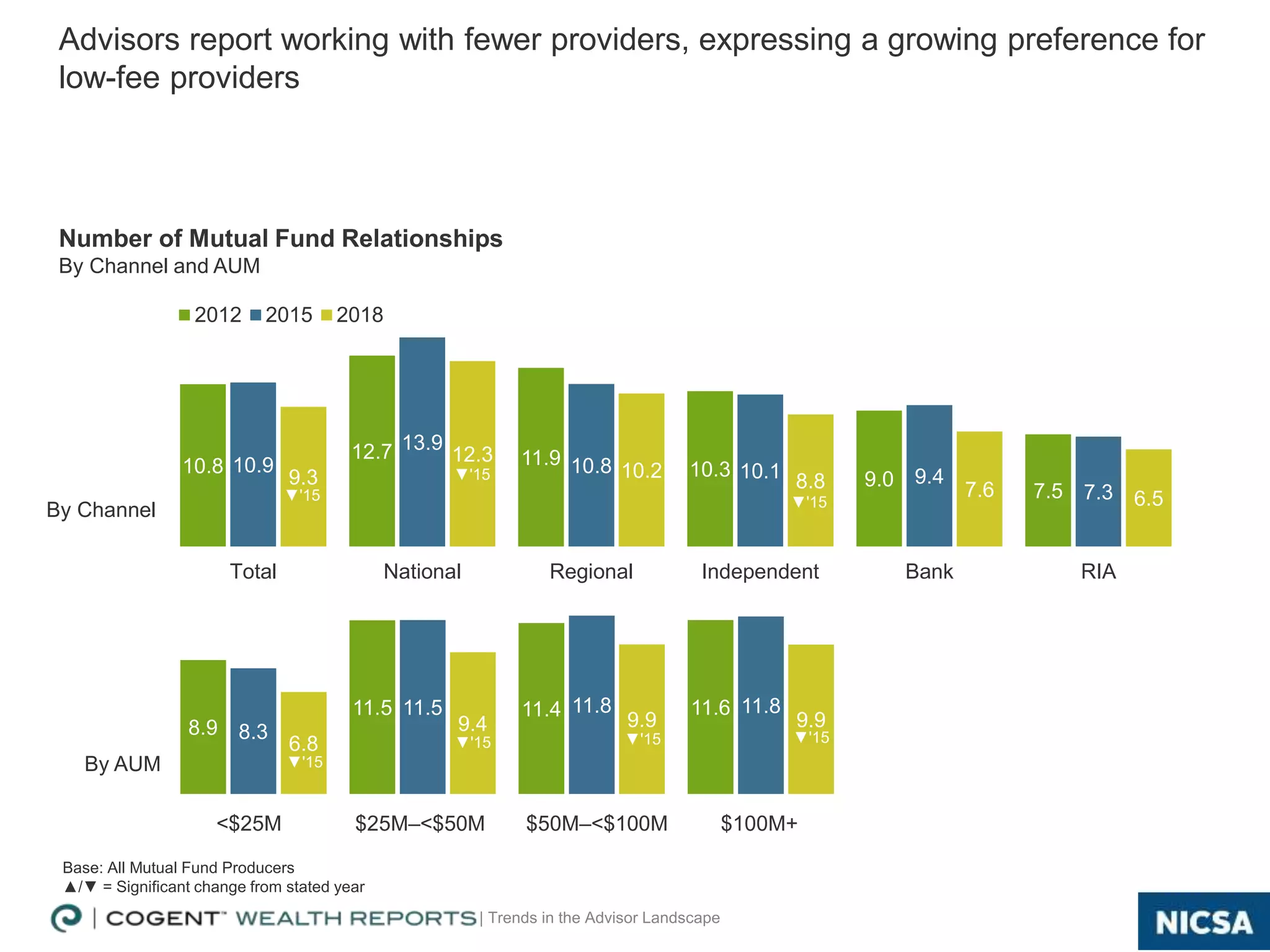

- The document discusses trends in the financial advisor landscape based on research from Cogent Reports. - It finds that while the total number of advisors is flat, the number of RIAs has increased 7% since 2015. Most advisors now derive over half their compensation from fee-based sources rather than commissions. - Advisors are increasingly using passively managed and low-fee investments like ETFs and index funds, with allocations to ETFs up 21% since 2015. They also report relationships with fewer mutual fund providers.