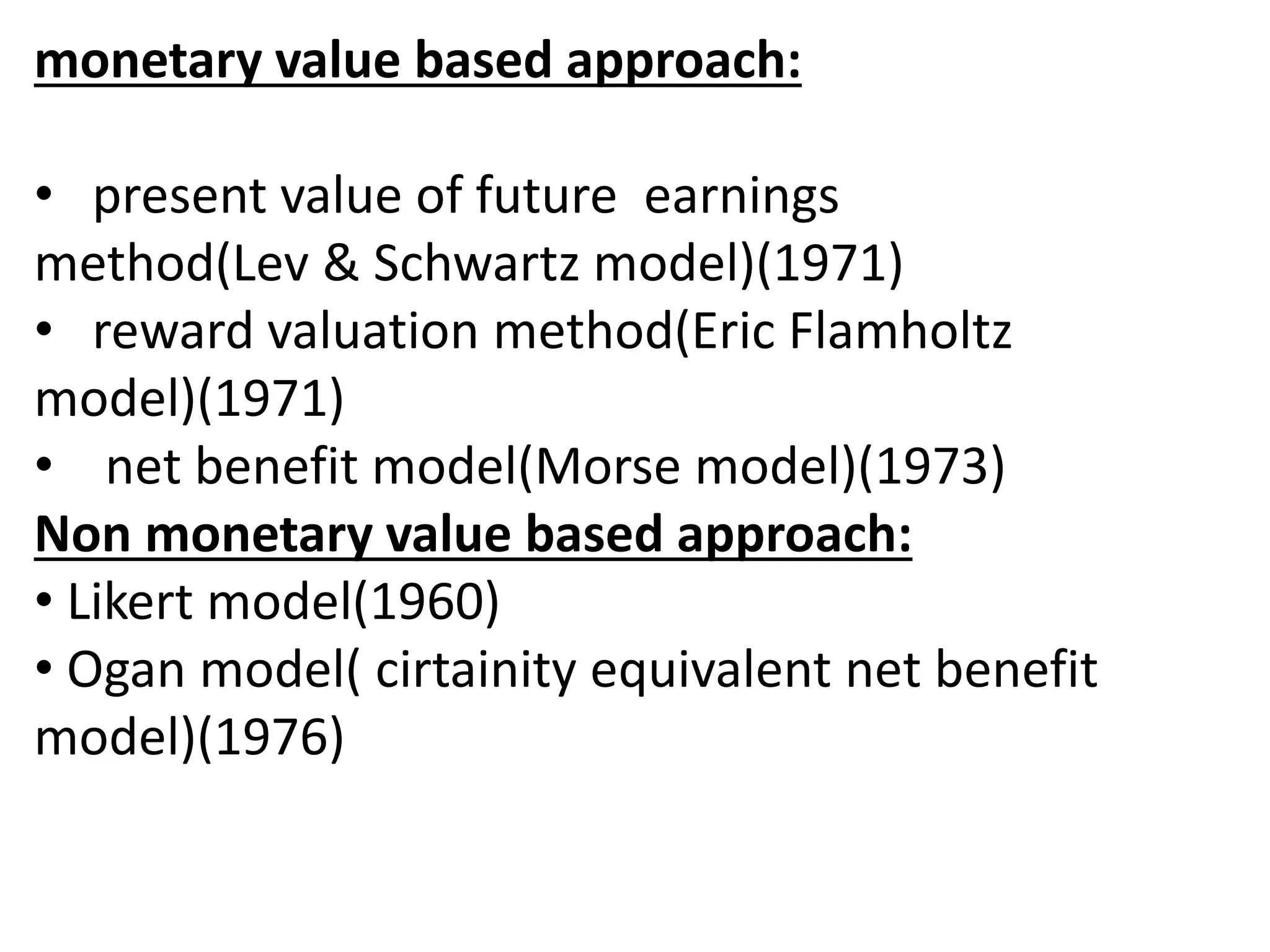

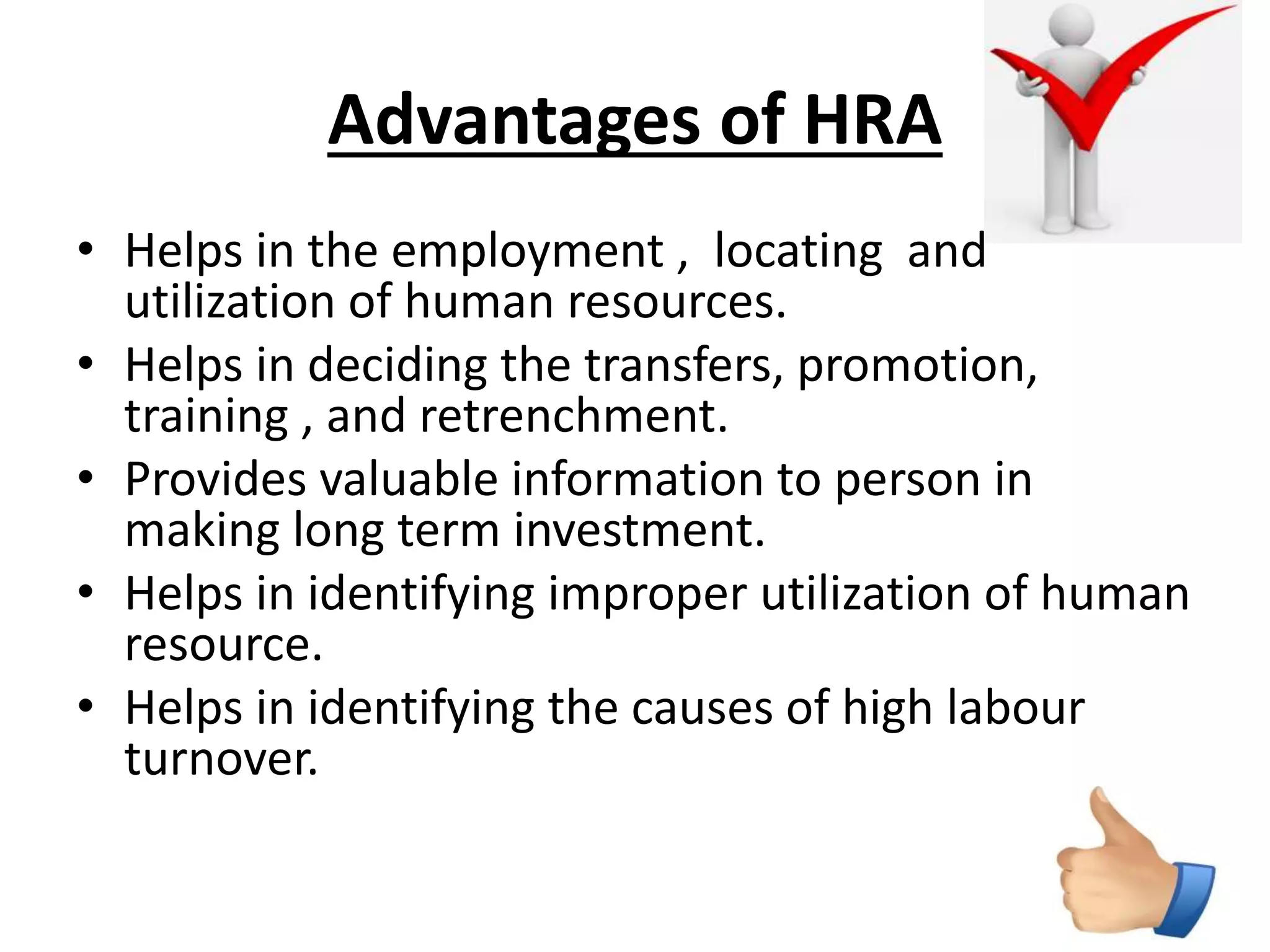

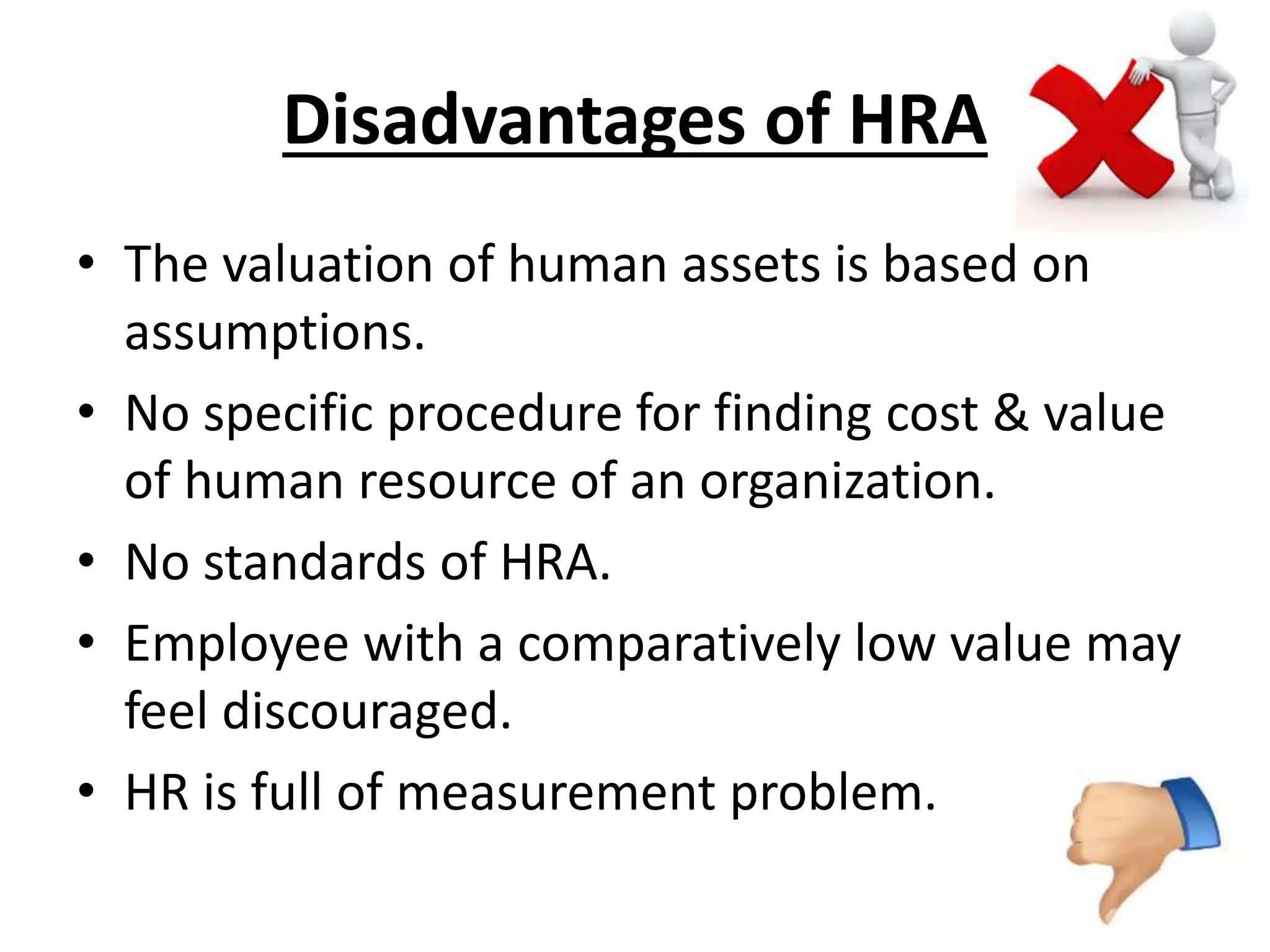

This document discusses human resource accounting, which is the process of assigning, budgeting, and reporting costs related to human resources in an organization, including wages, salaries, and training expenses. It outlines two approaches to valuing human resources - the cost-based approach which focuses on the investment made by the organization using methods like historical cost, replacement cost, and opportunity cost, and the value-based approach which focuses on the difference between present and future earnings using monetary and non-monetary valuation models. The advantages and disadvantages of implementing human resource accounting are also presented.