Downloaded 177 times

The document discusses the integration of data analytics into risk-based audit plans, emphasizing the need for a visionary approach in risk management that transcends technology and includes cultural and philosophical shifts. It highlights the importance of broadening the internal audit's focus towards business strategy and stakeholder satisfaction, while also developing skilled teams and utilizing data analytics to drive insights and efficiencies. The future of auditing is portrayed as increasingly reliant on visual data discoveries and effective communication of audit findings to stakeholders.

Introduction to integrating data analytics in a risk-based audit plan.

Factors influencing risk management include cost reduction, value addition, regulatory changes, and technology.

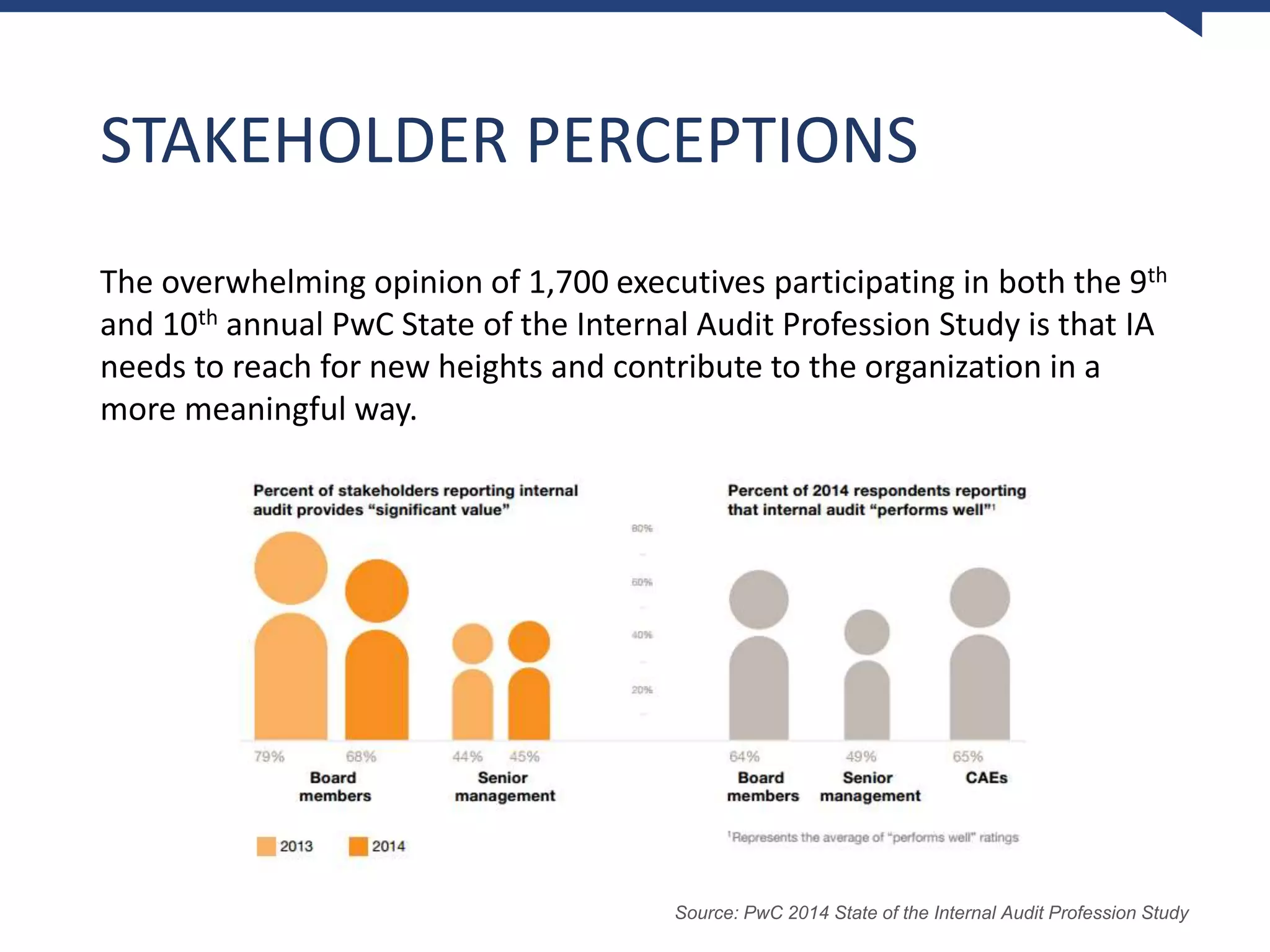

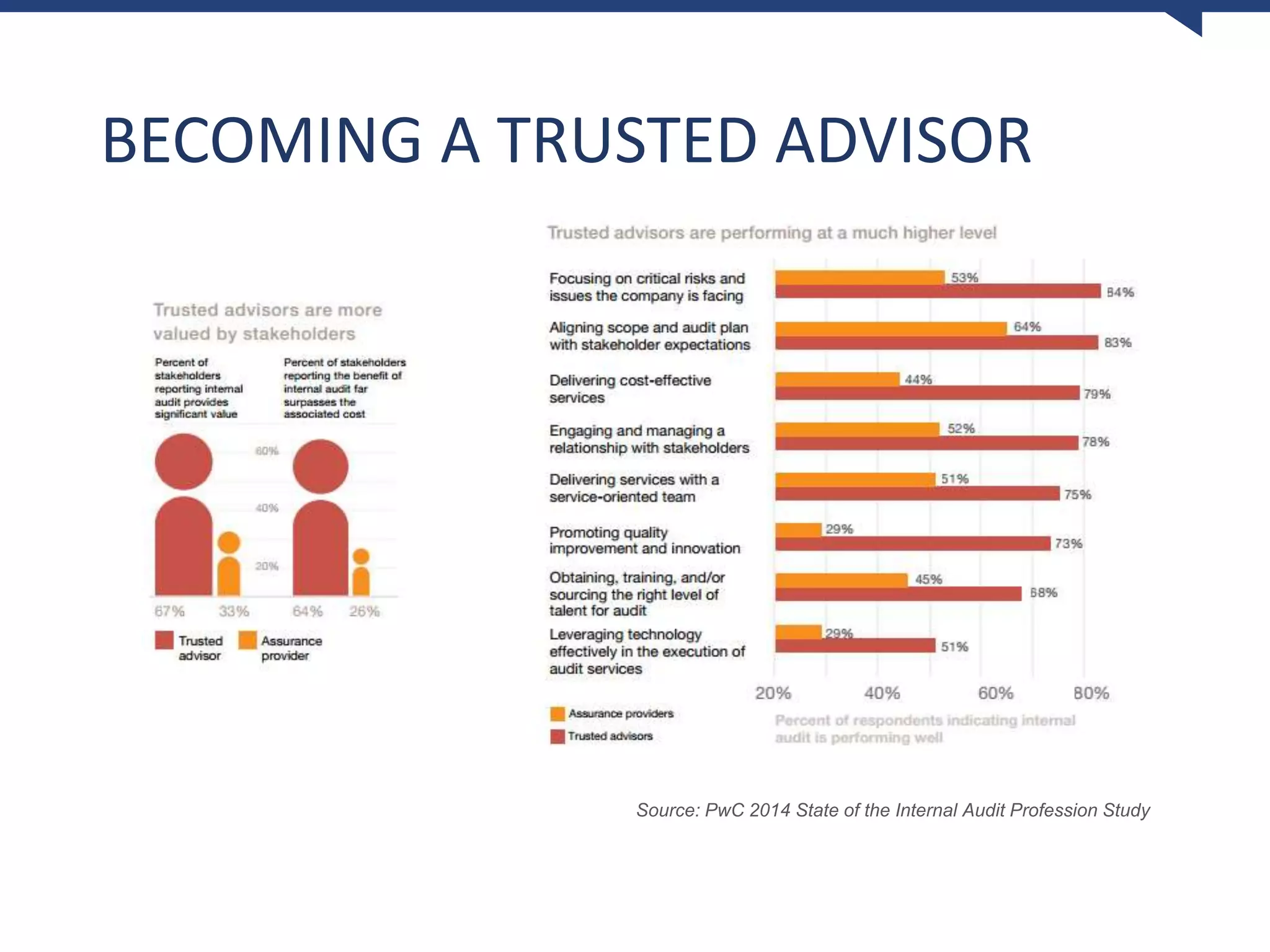

Executives from PwC studies emphasize the need for internal audit to contribute meaningfully.

A successful risk management strategy encompasses culture, philosophy, and technology integration.

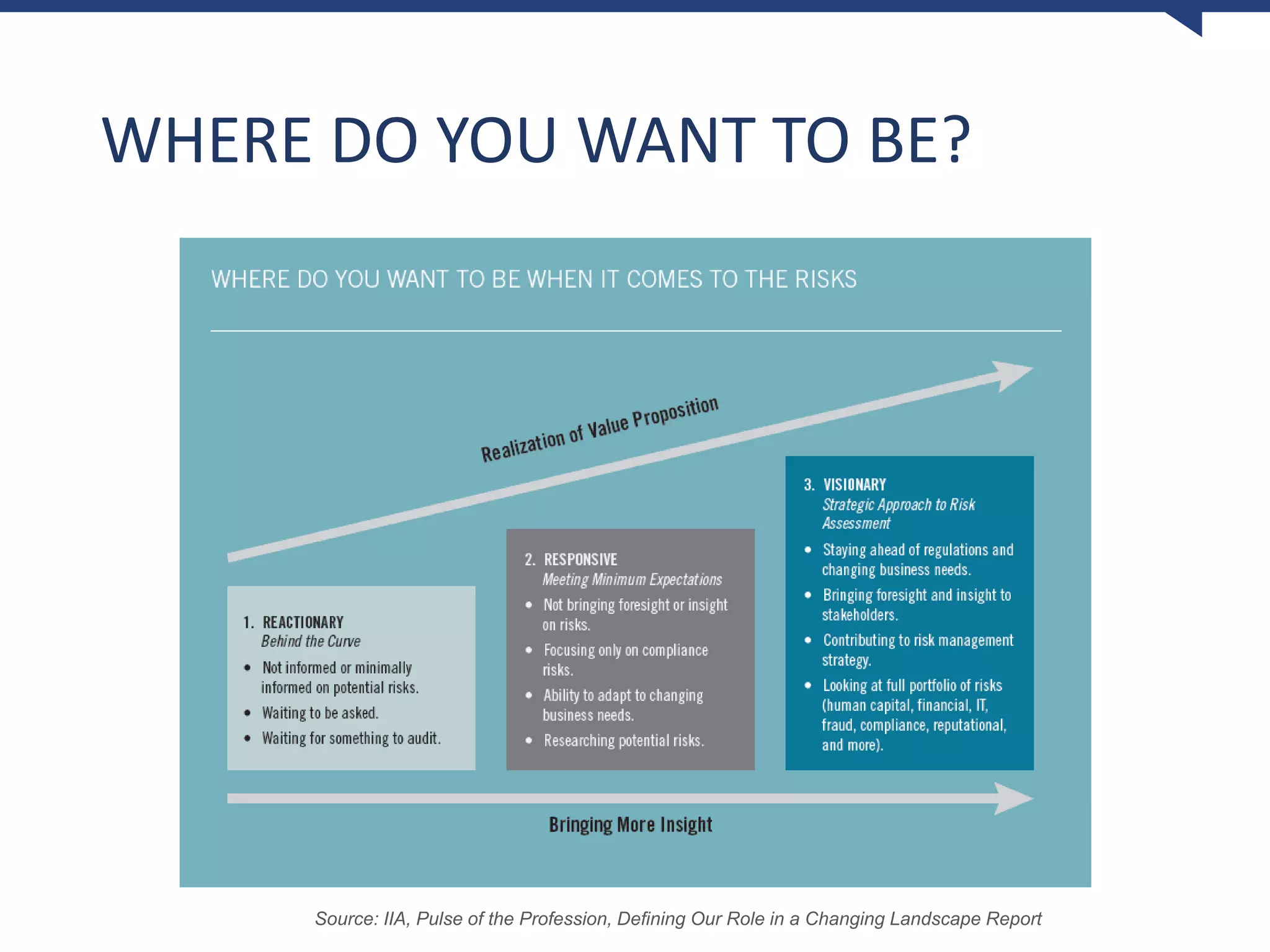

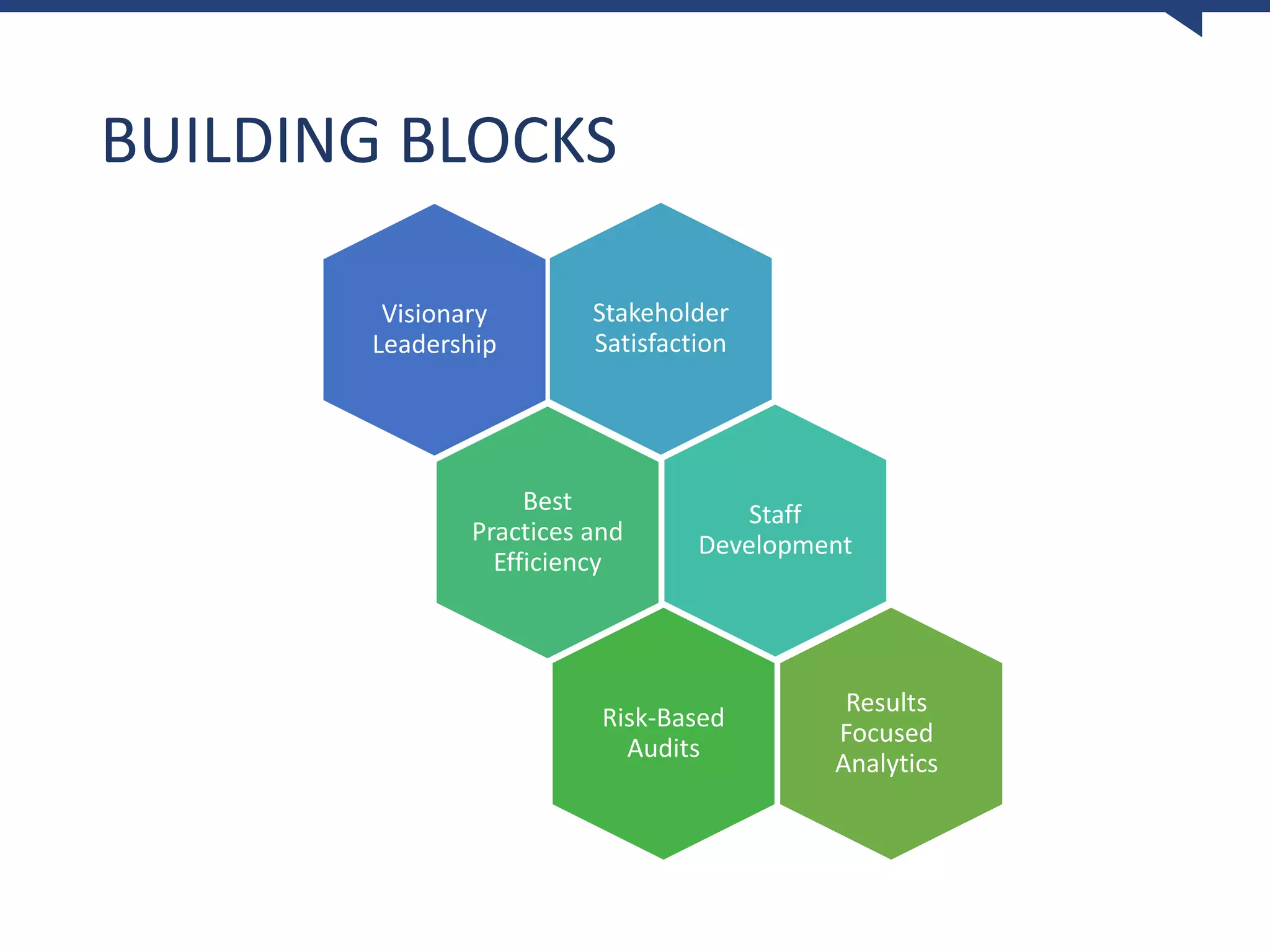

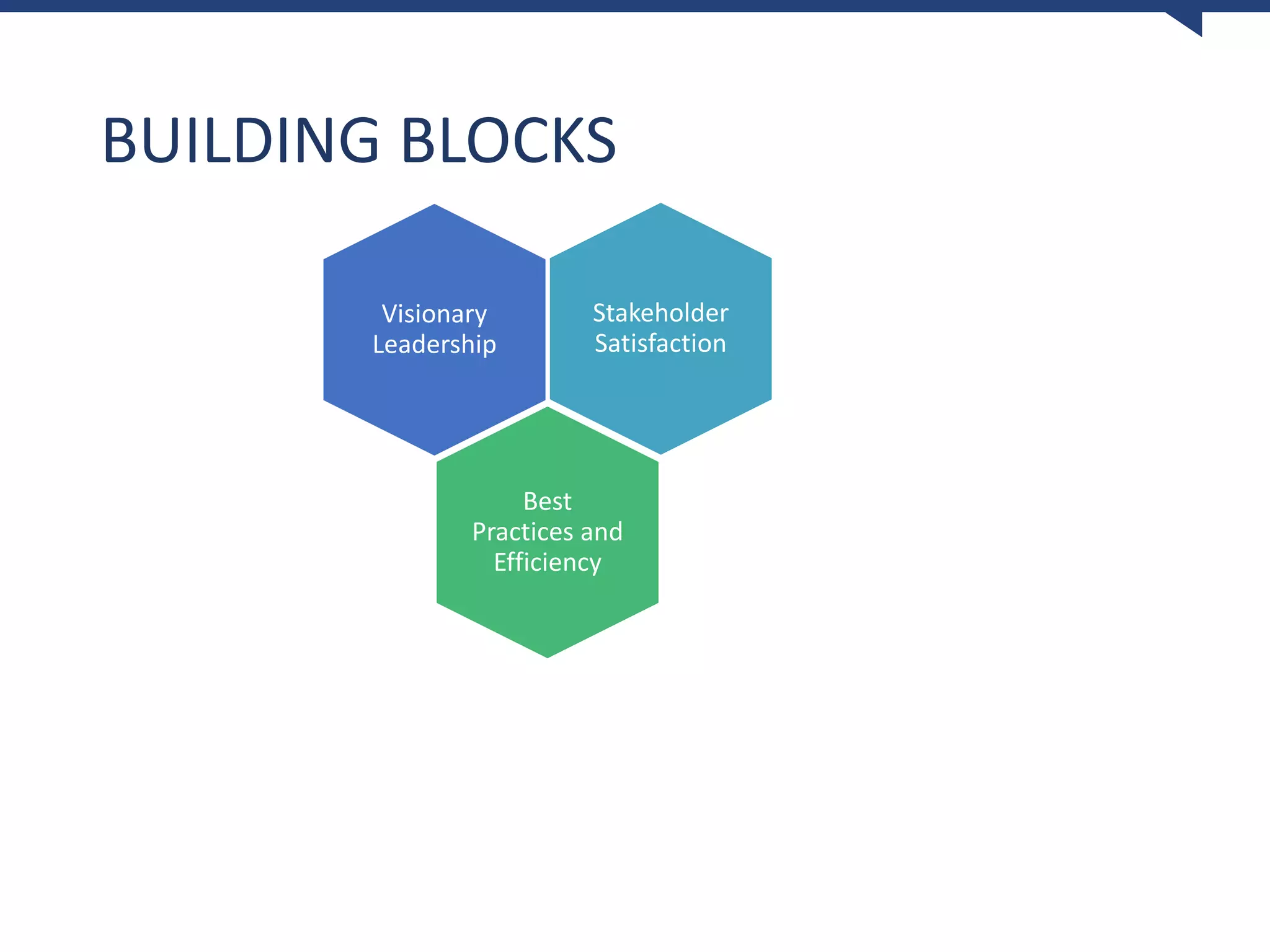

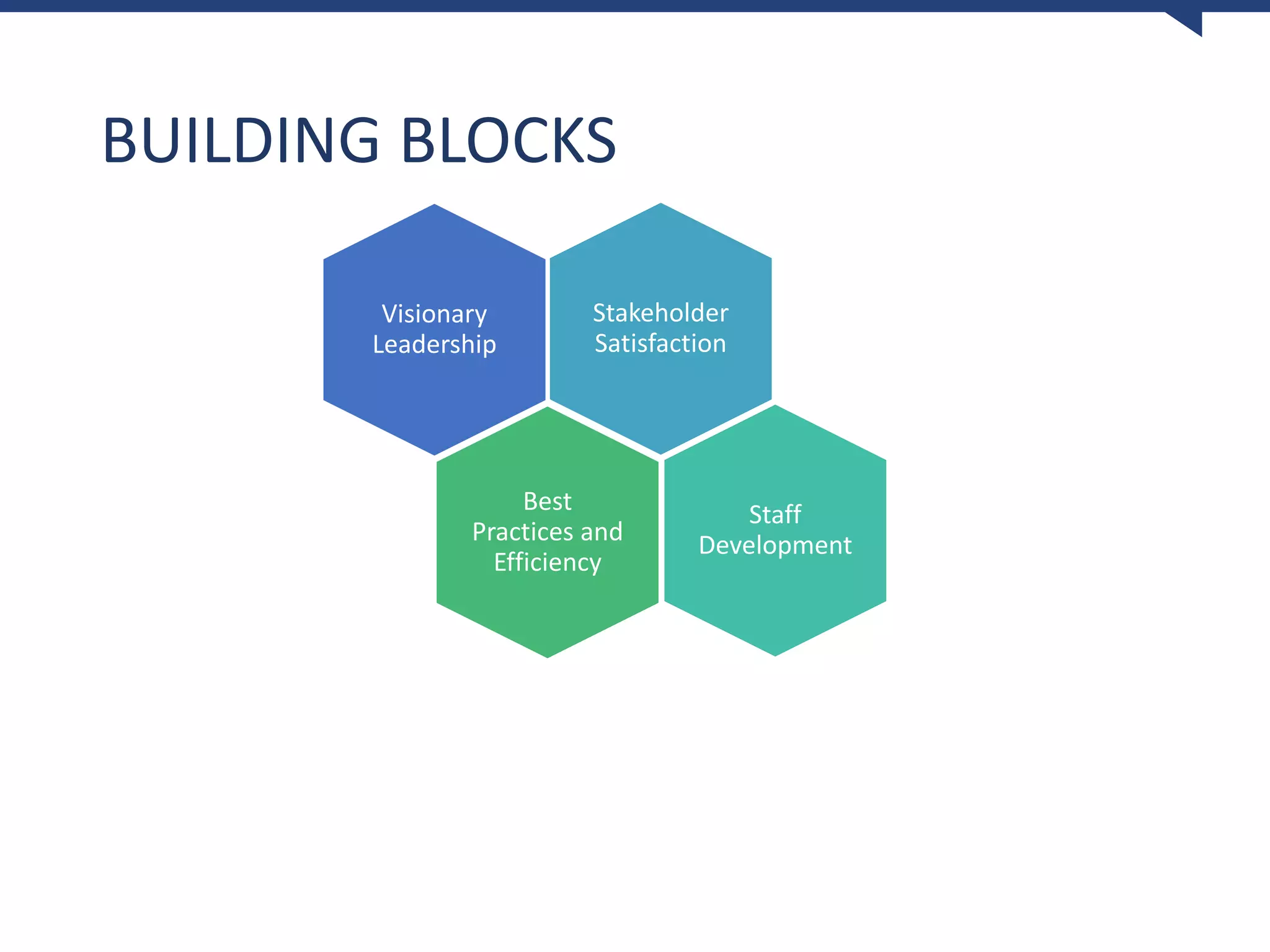

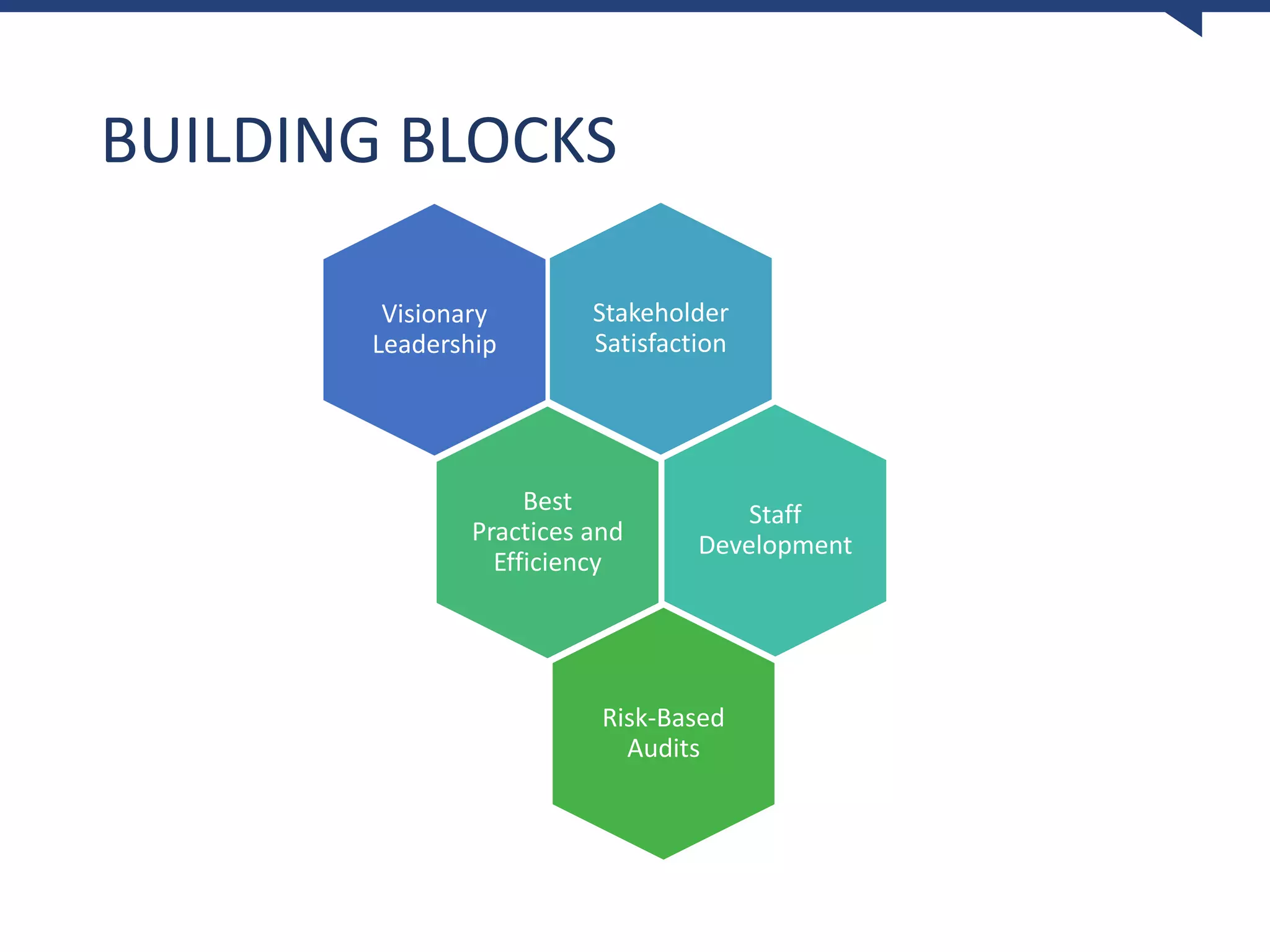

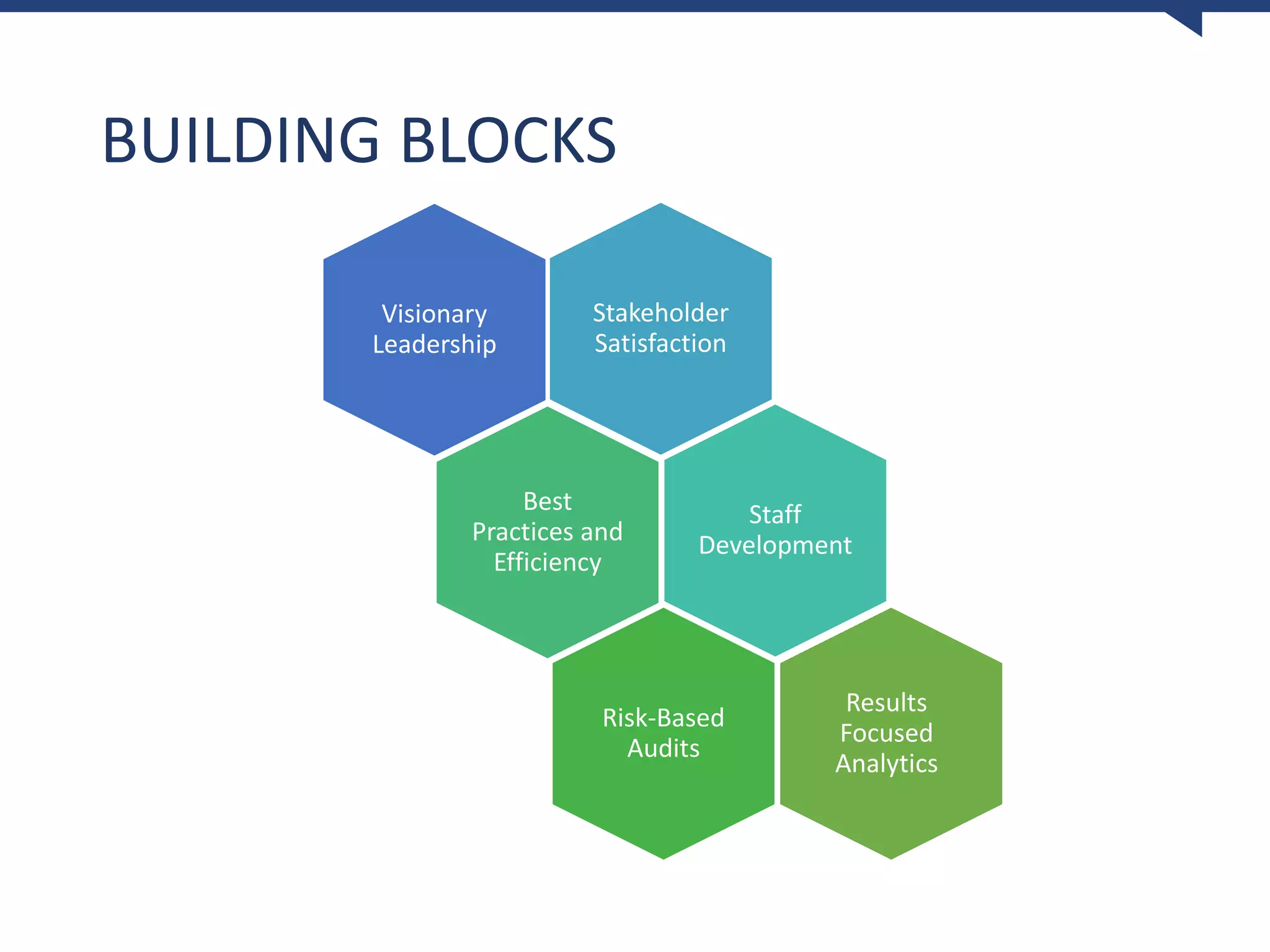

Key components for effective audits: visionary leadership, stakeholder satisfaction, best practices, and efficiency.

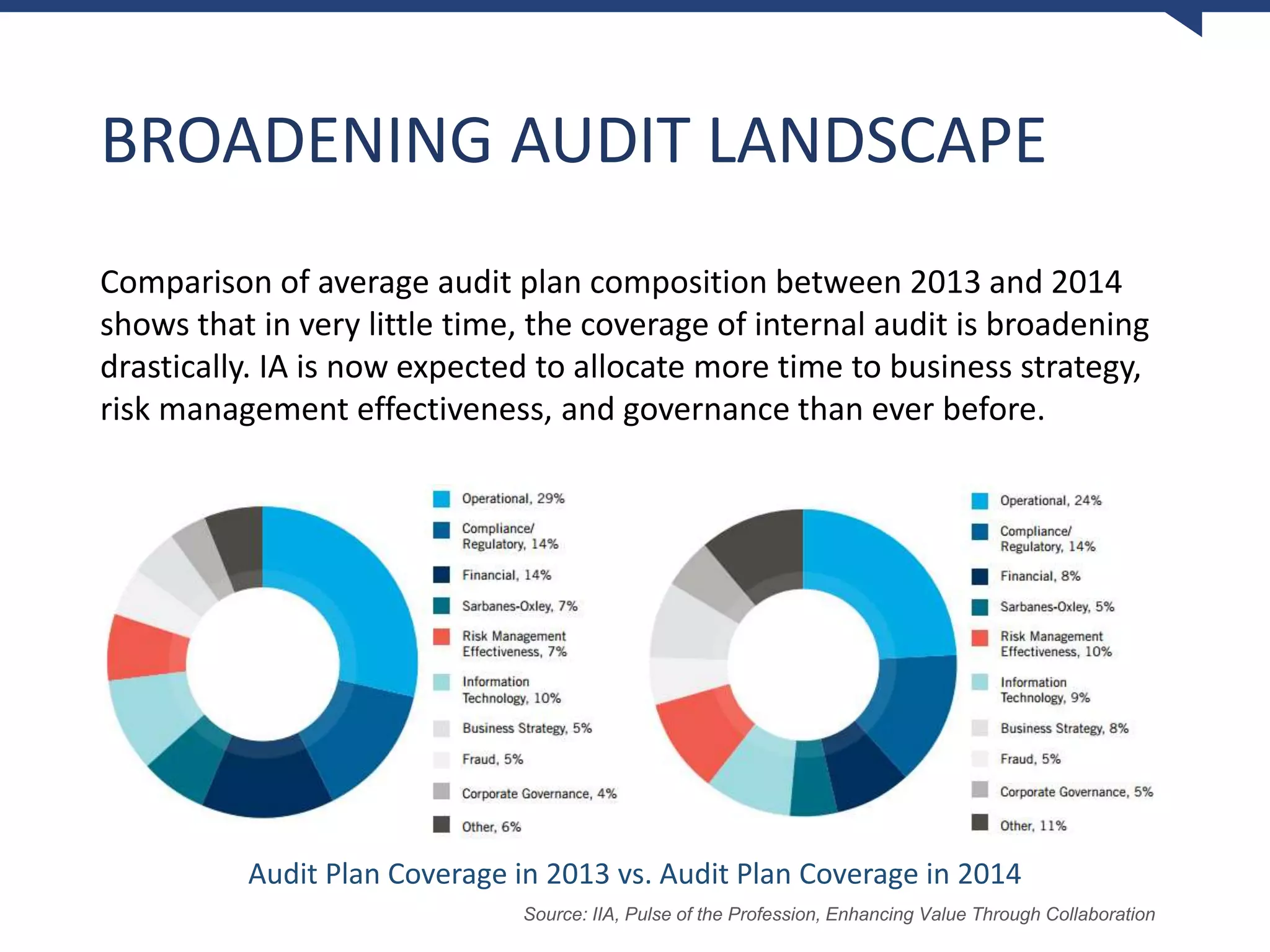

Rapid changes in audit plan compositions show increased focus on strategy, risk management, and governance.

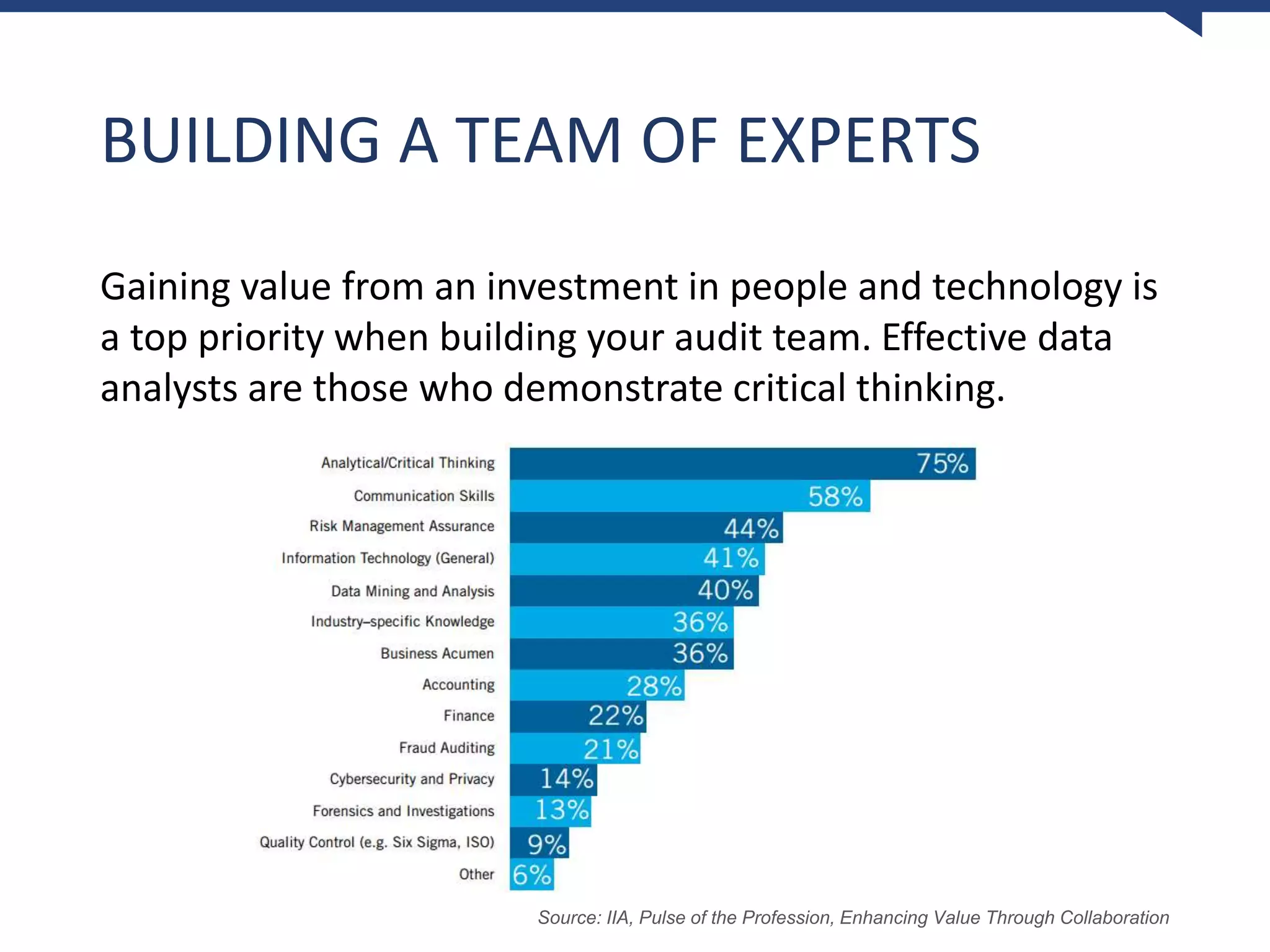

Importance of investing in skilled people and technology for effective data analysis in audits.

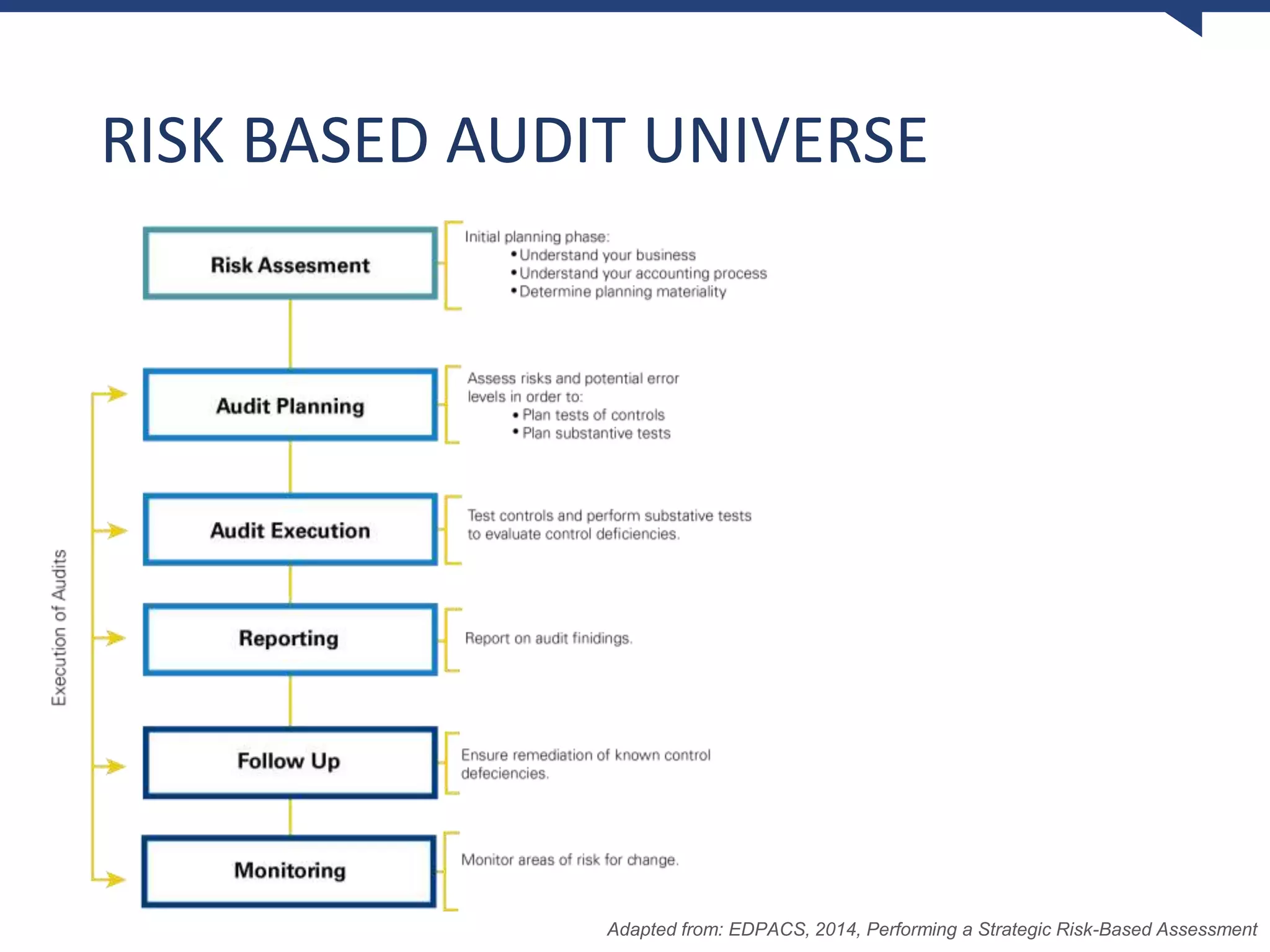

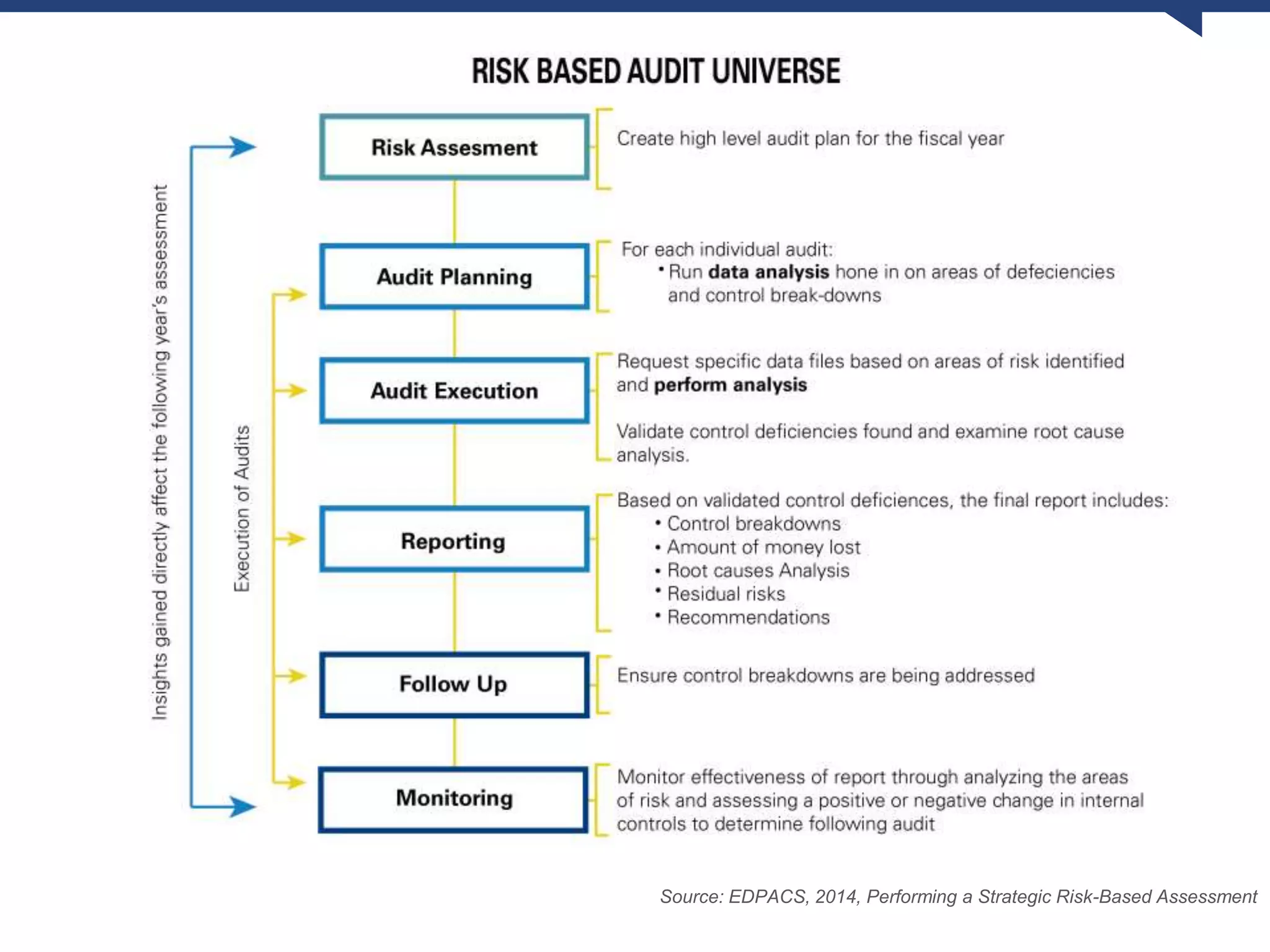

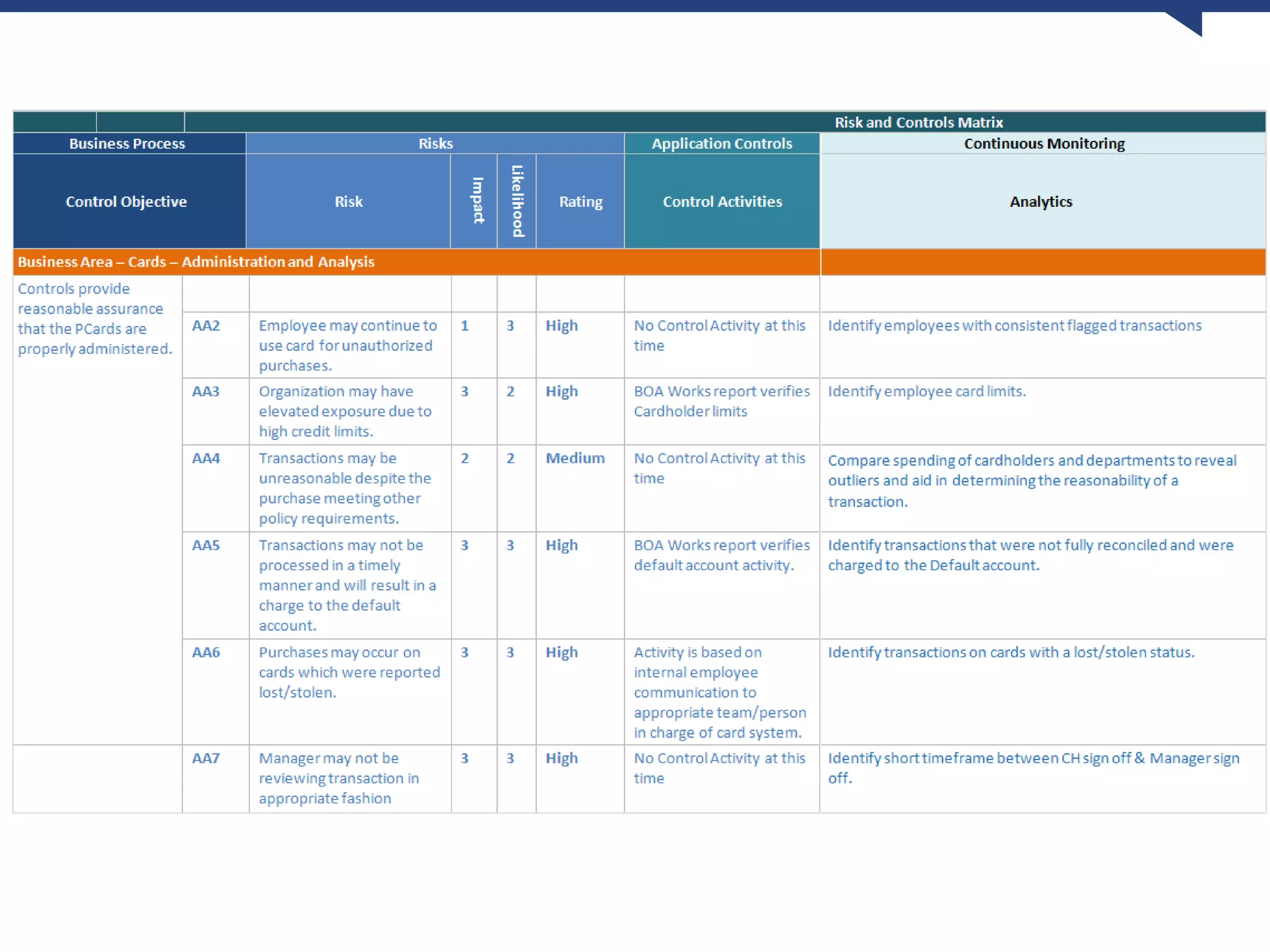

Discussion on assessing risks effectively within the audit universe for better outcomes.

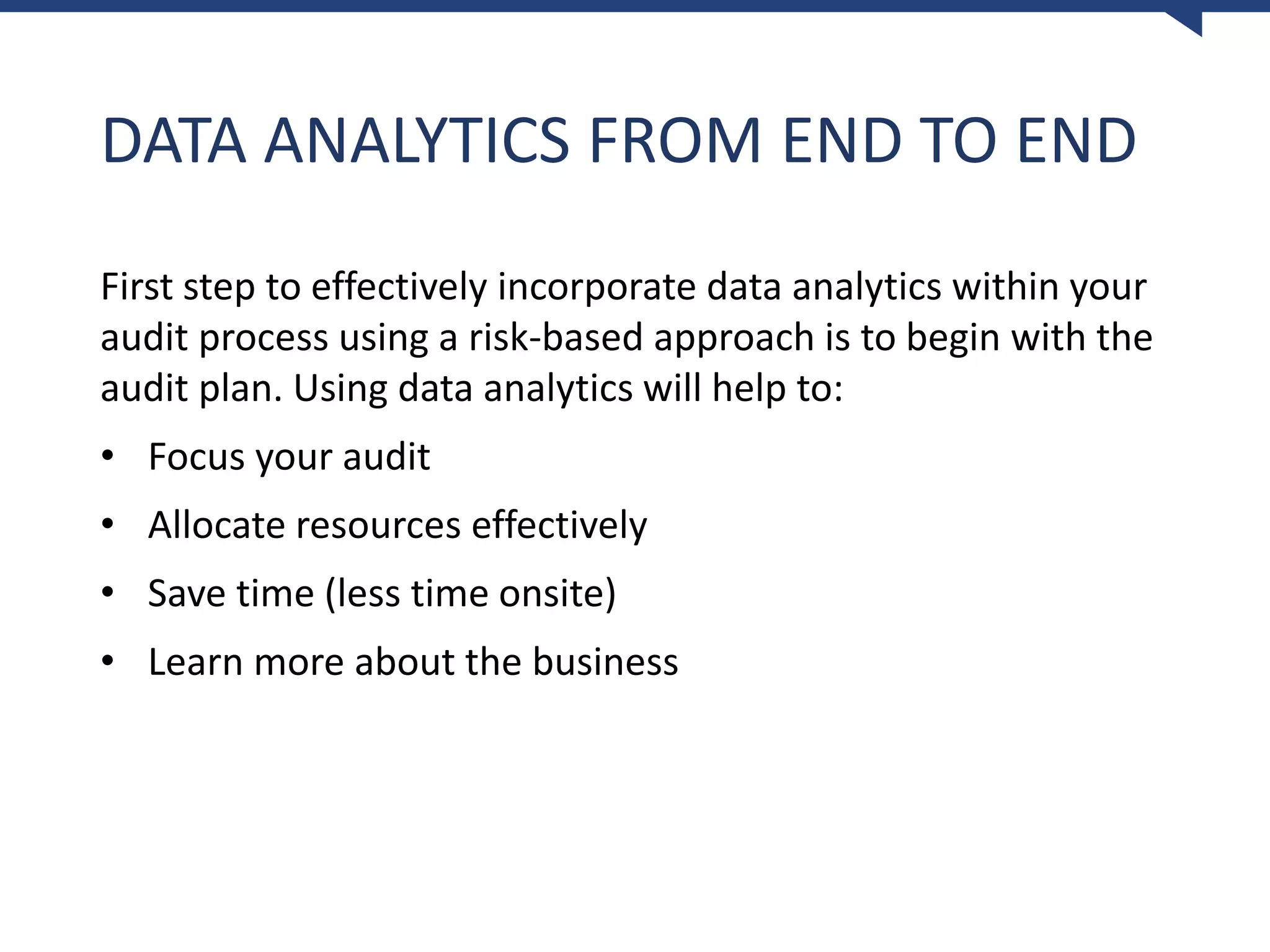

Using insights effectively in risk-based audits by incorporating data analytics in planning and execution.

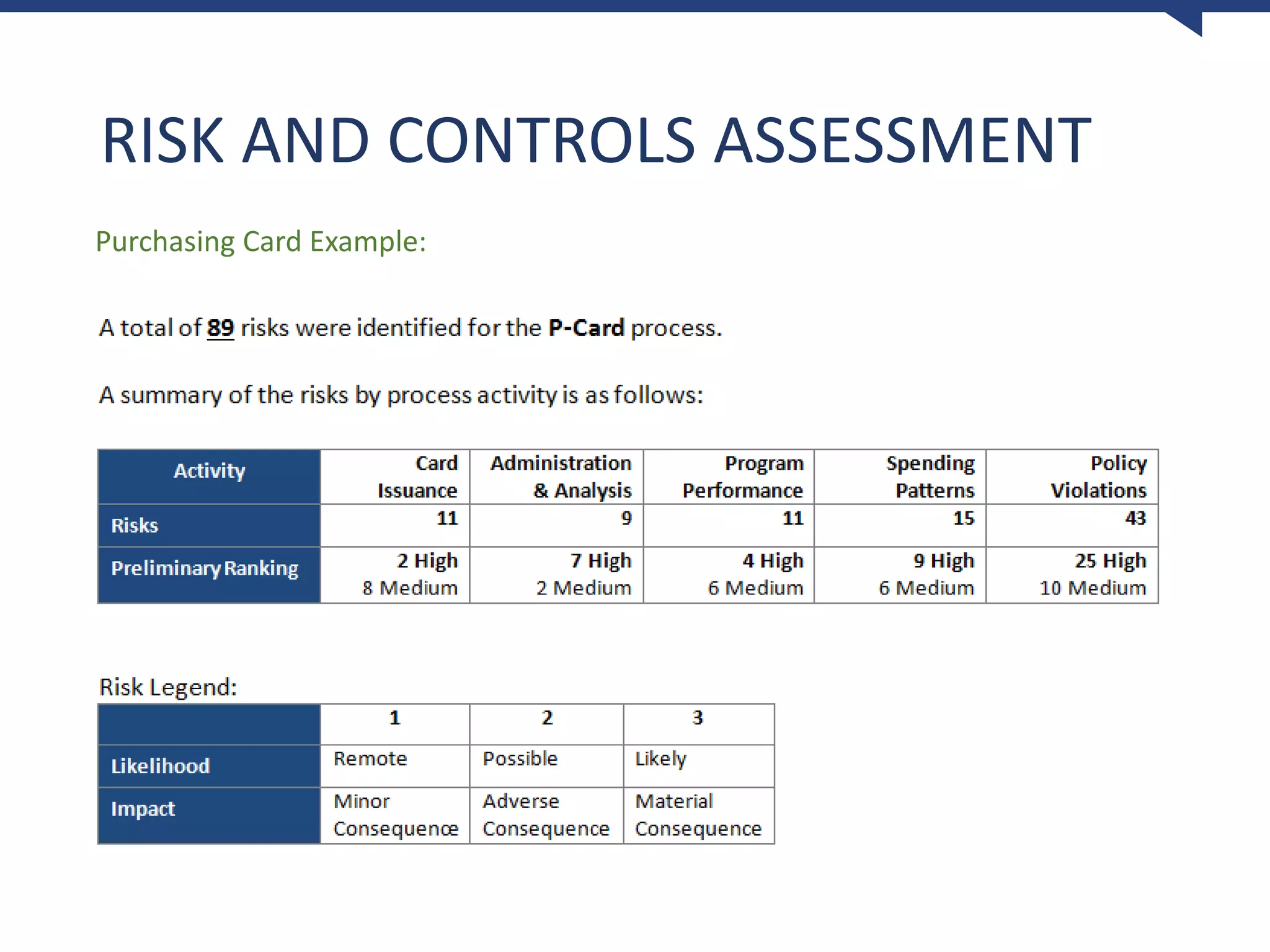

Analyzing comprehensive data to eliminate risk in controls assessments and enhance audits.

The ongoing need for analytics in audit reporting to highlight deficiencies and provide clear recommendations. Visual data tools can enhance audit practices and decision-making through insightful data analysis.

![[DSC Europe 25] Natasha Savic - Agentic AI in Production: Lessons from Real-W...](https://cdn.slidesharecdn.com/ss_thumbnails/91fscf7rraabydlmw6xj-natasha-savic-251127093914-7098d487-thumbnail.jpg?width=640&height=640&fit=bounds)