Downloaded 299 times

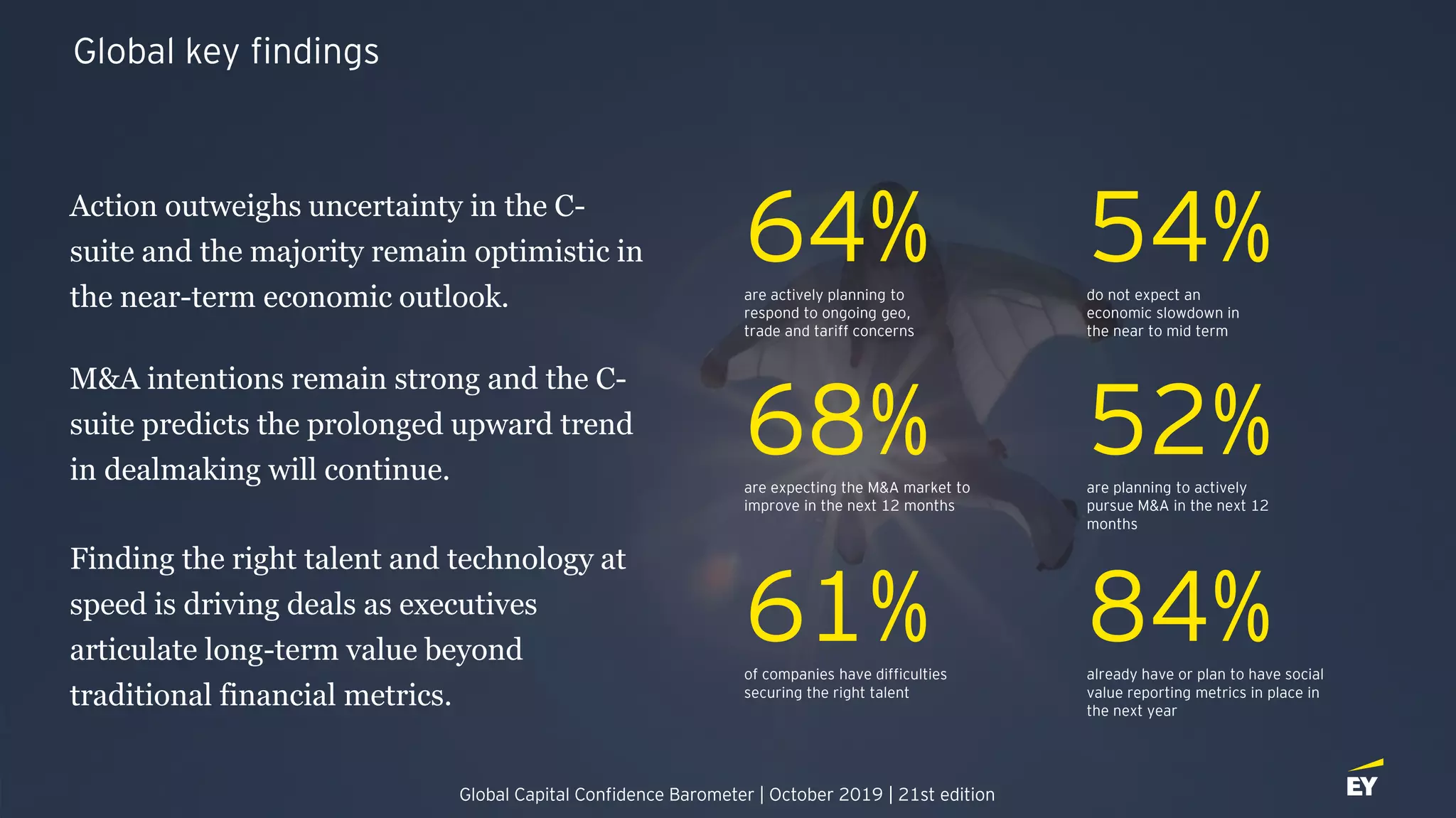

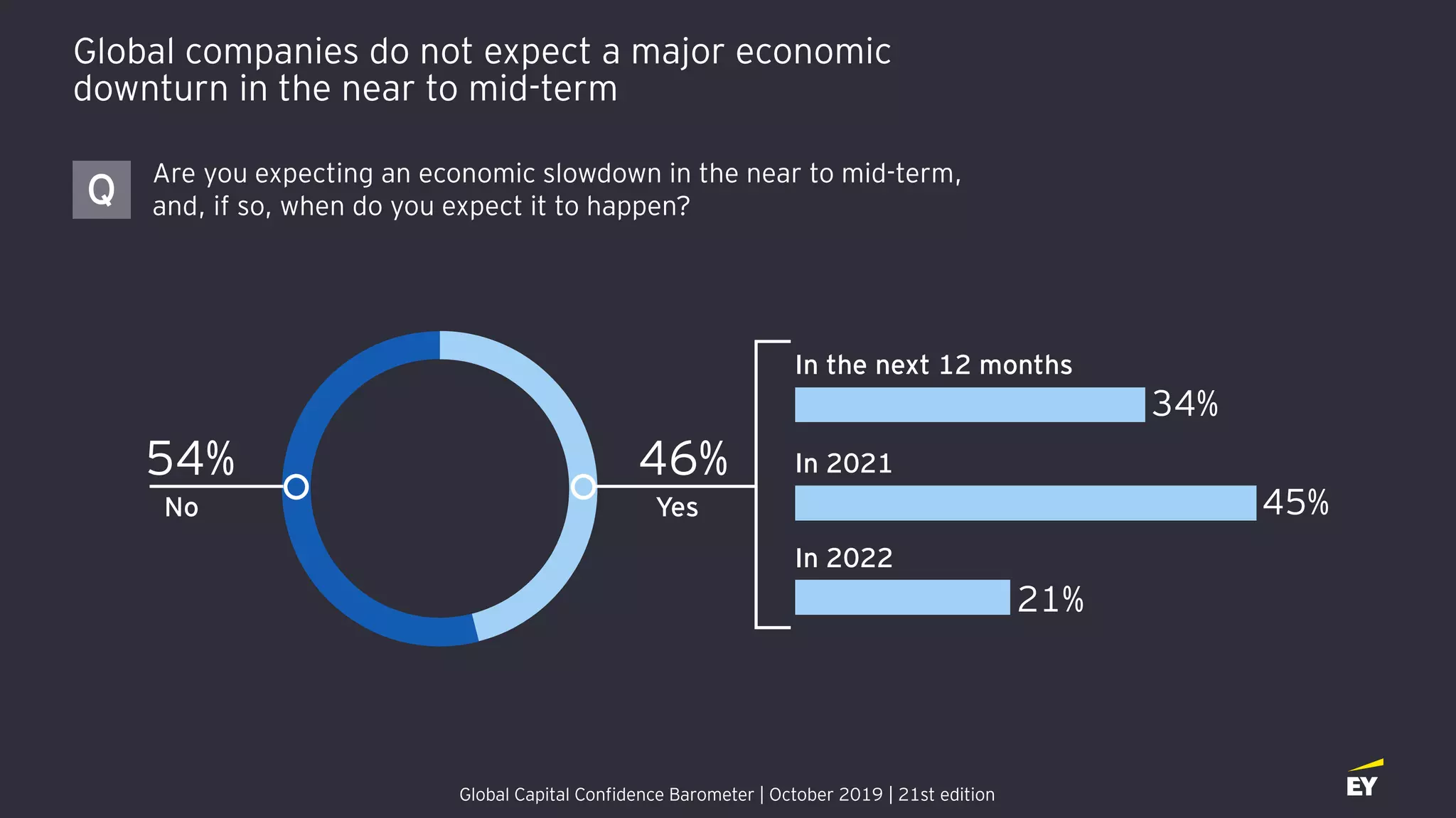

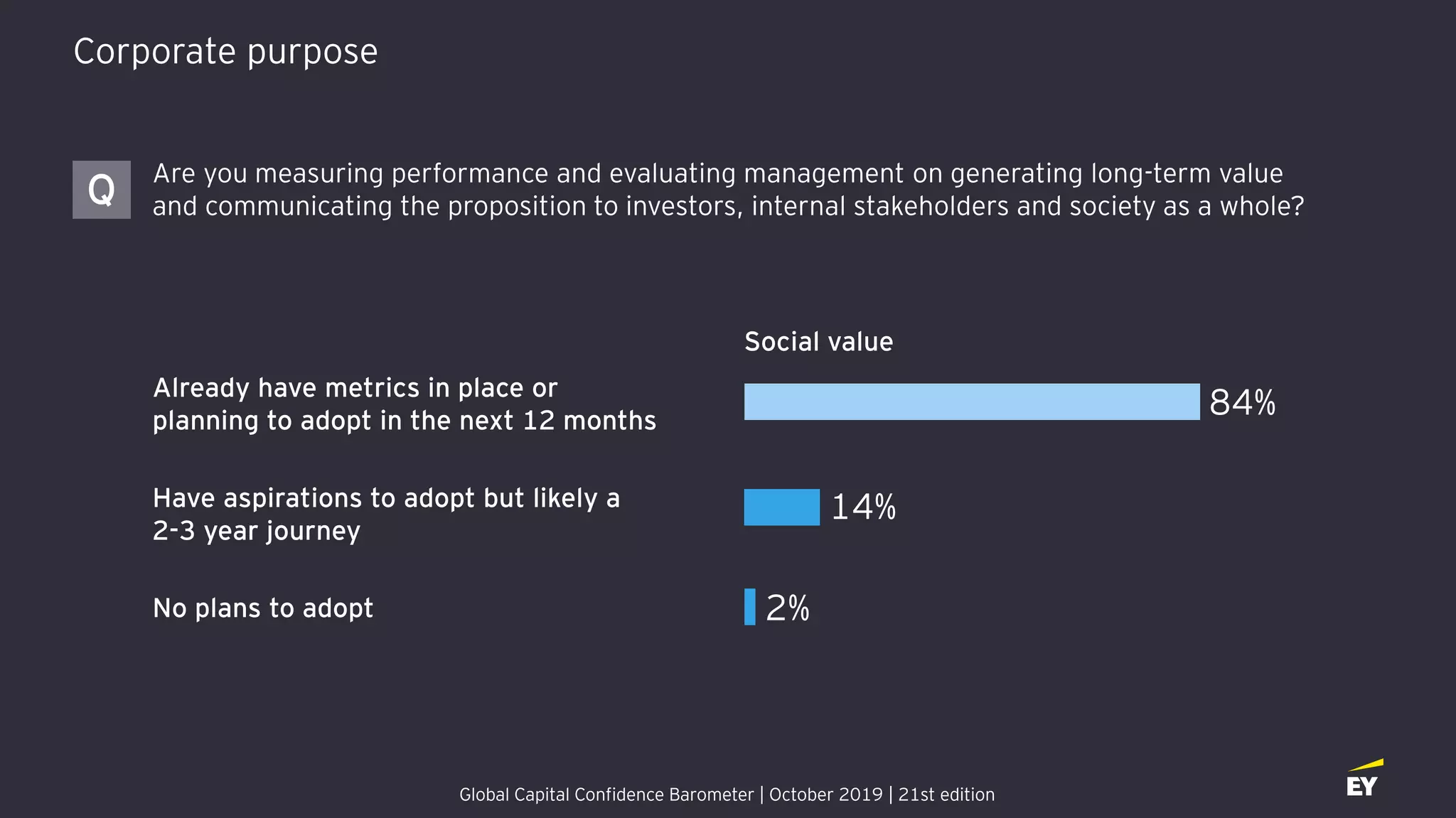

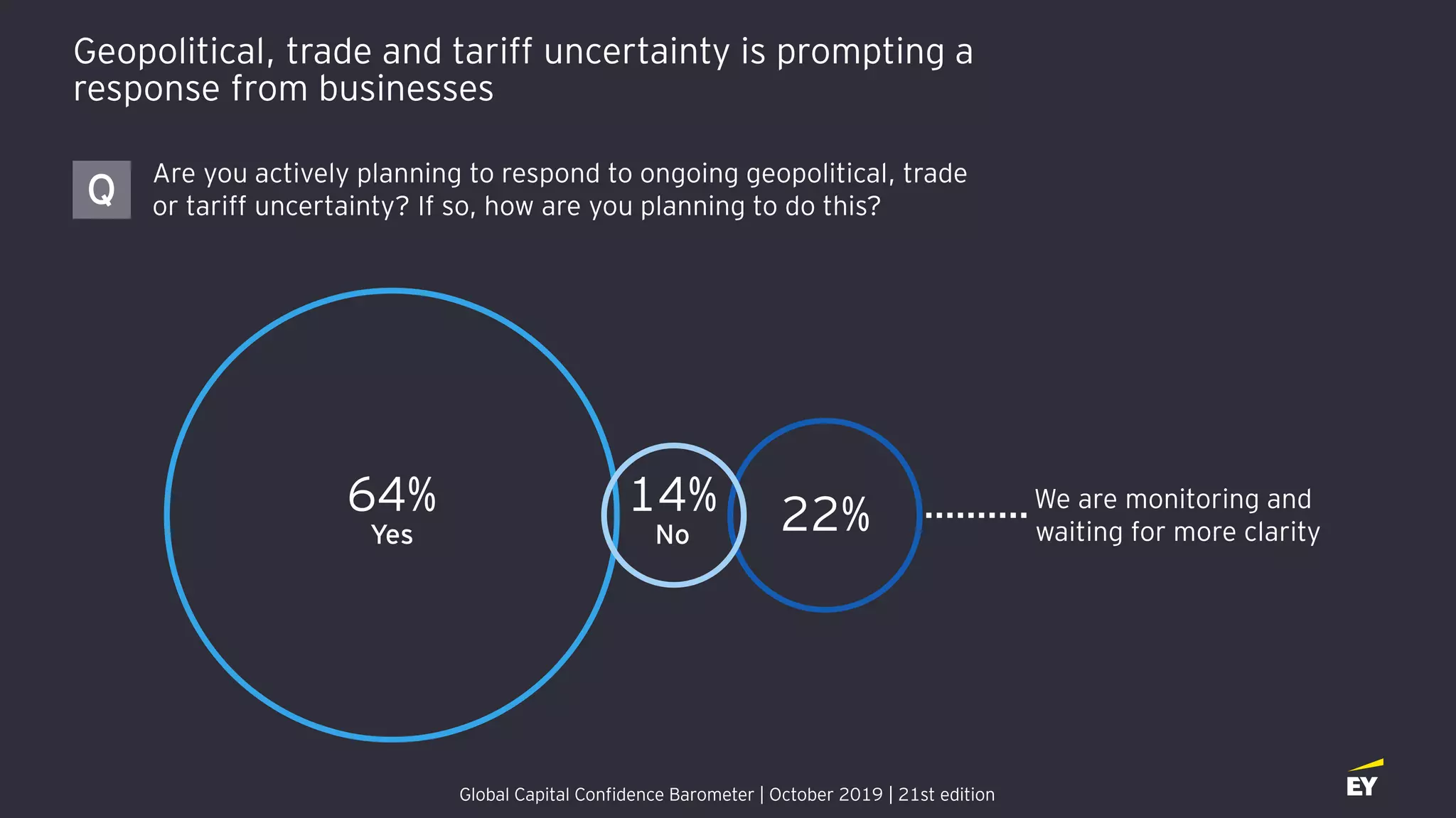

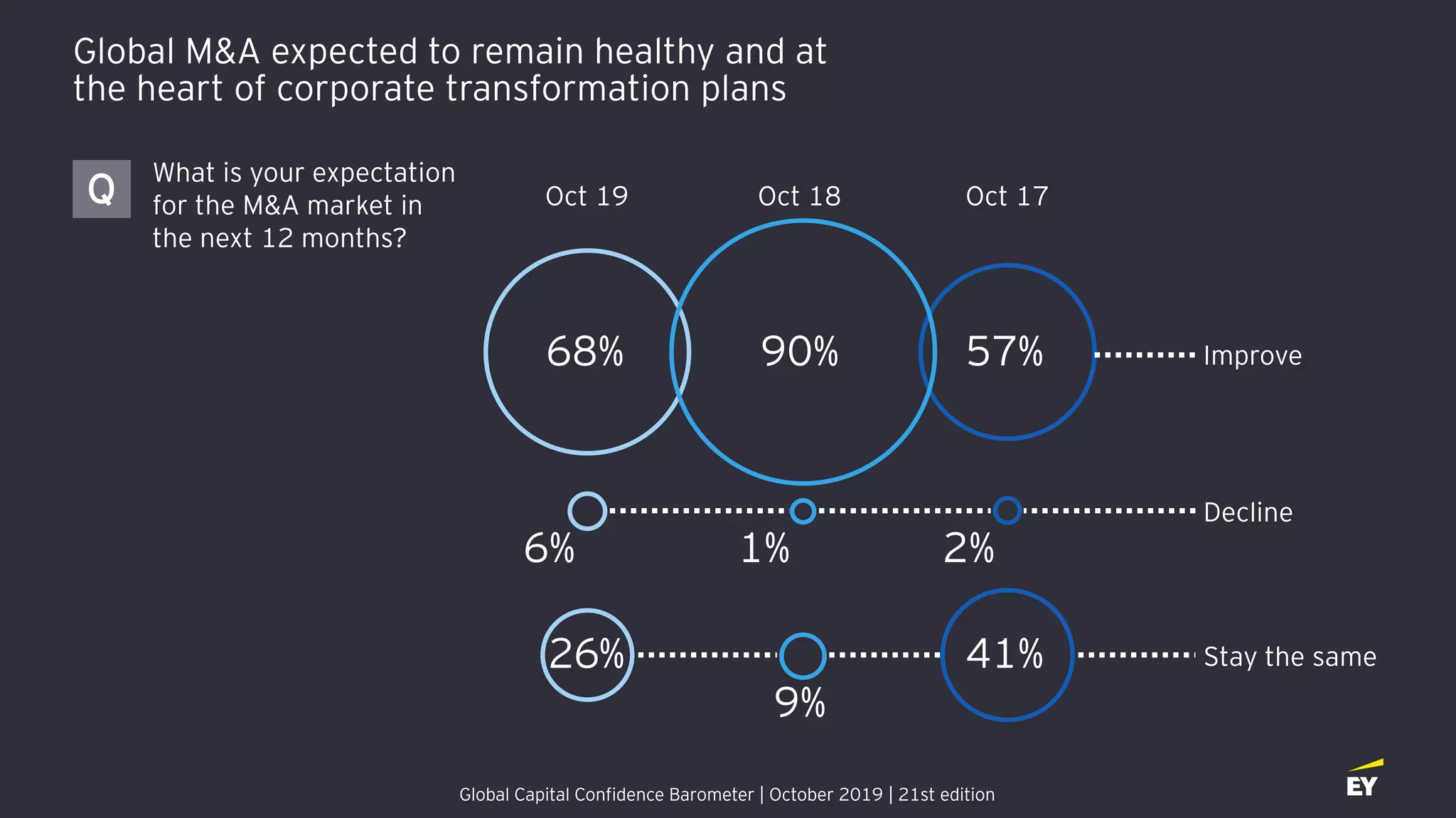

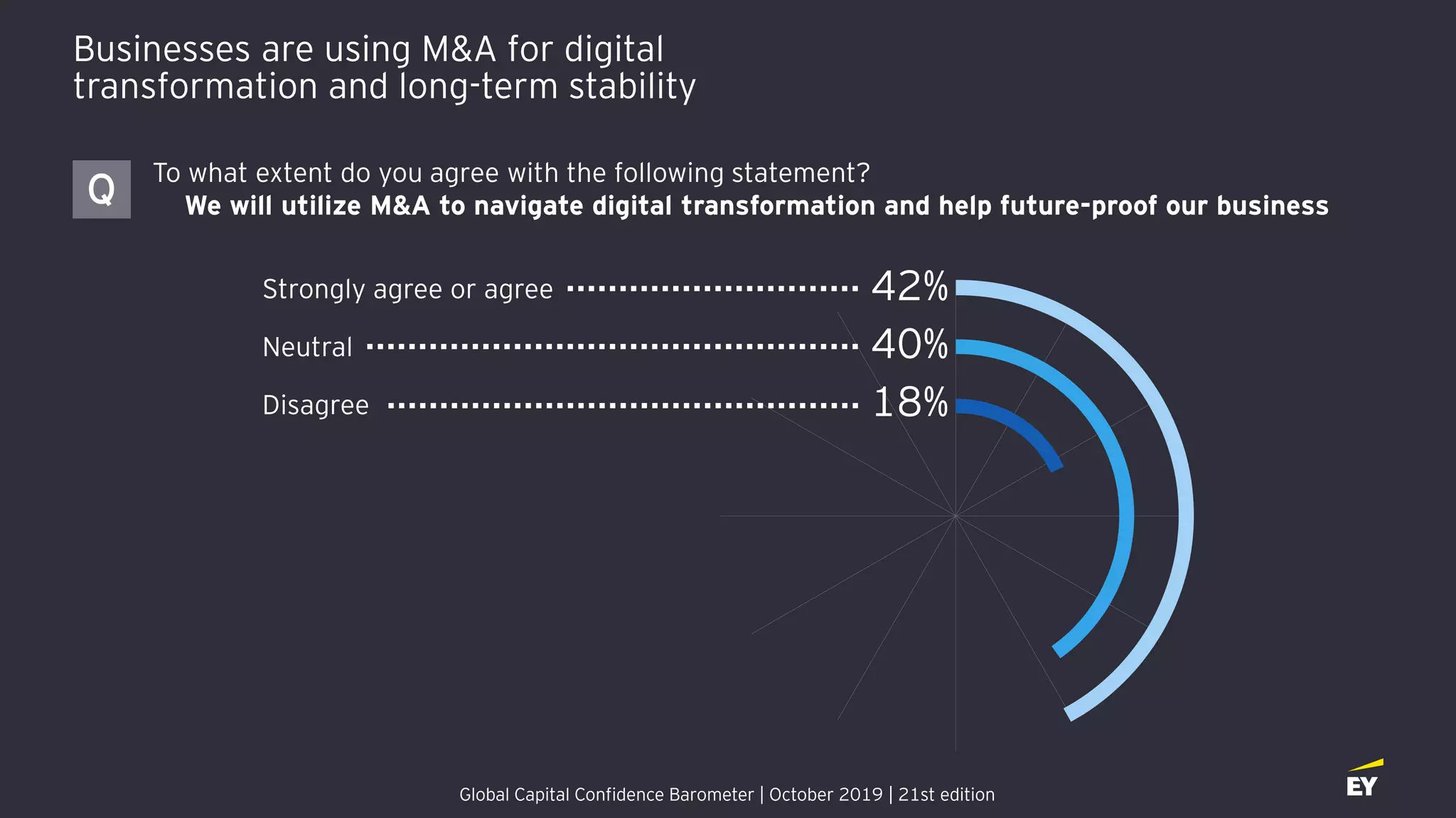

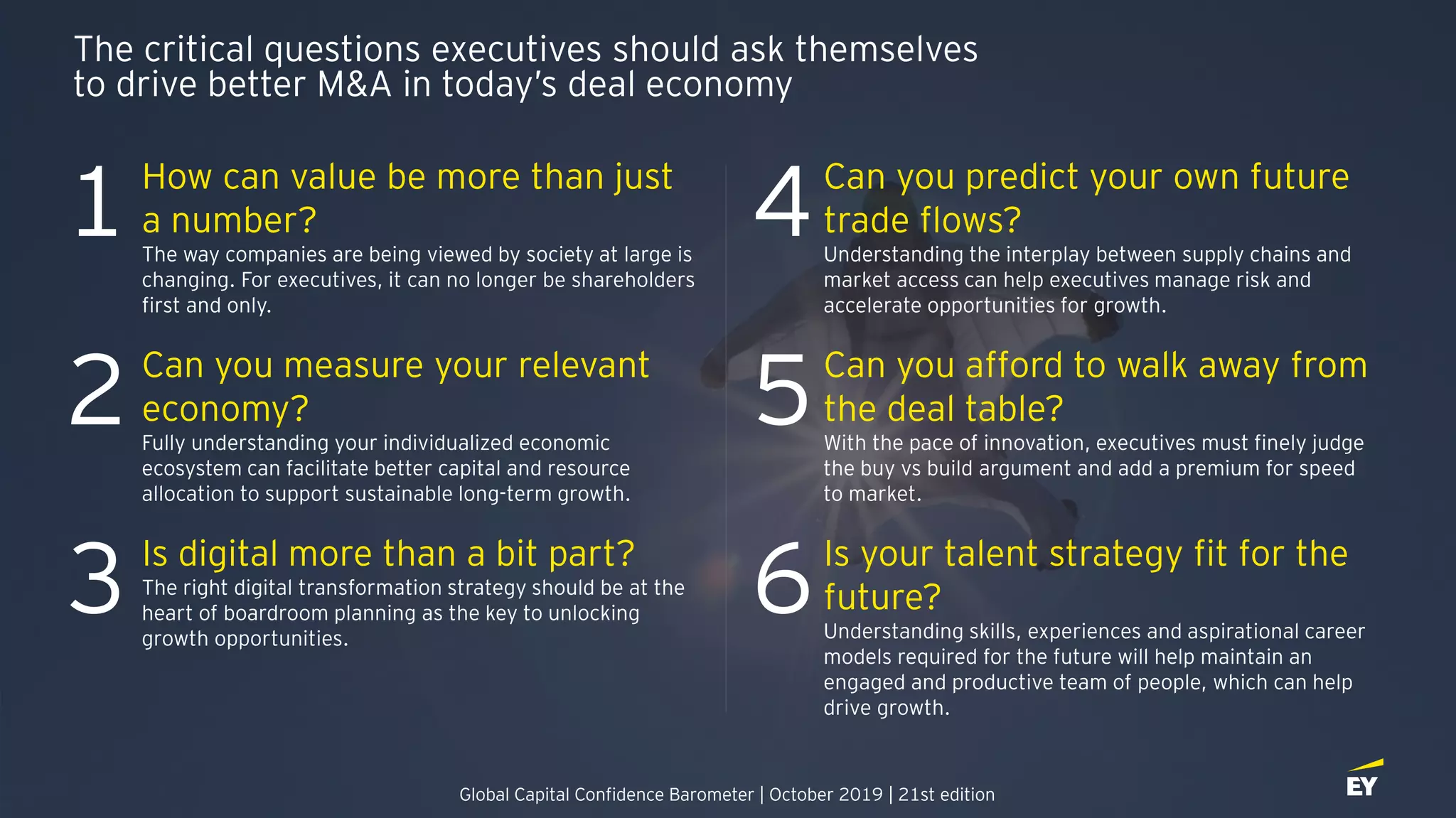

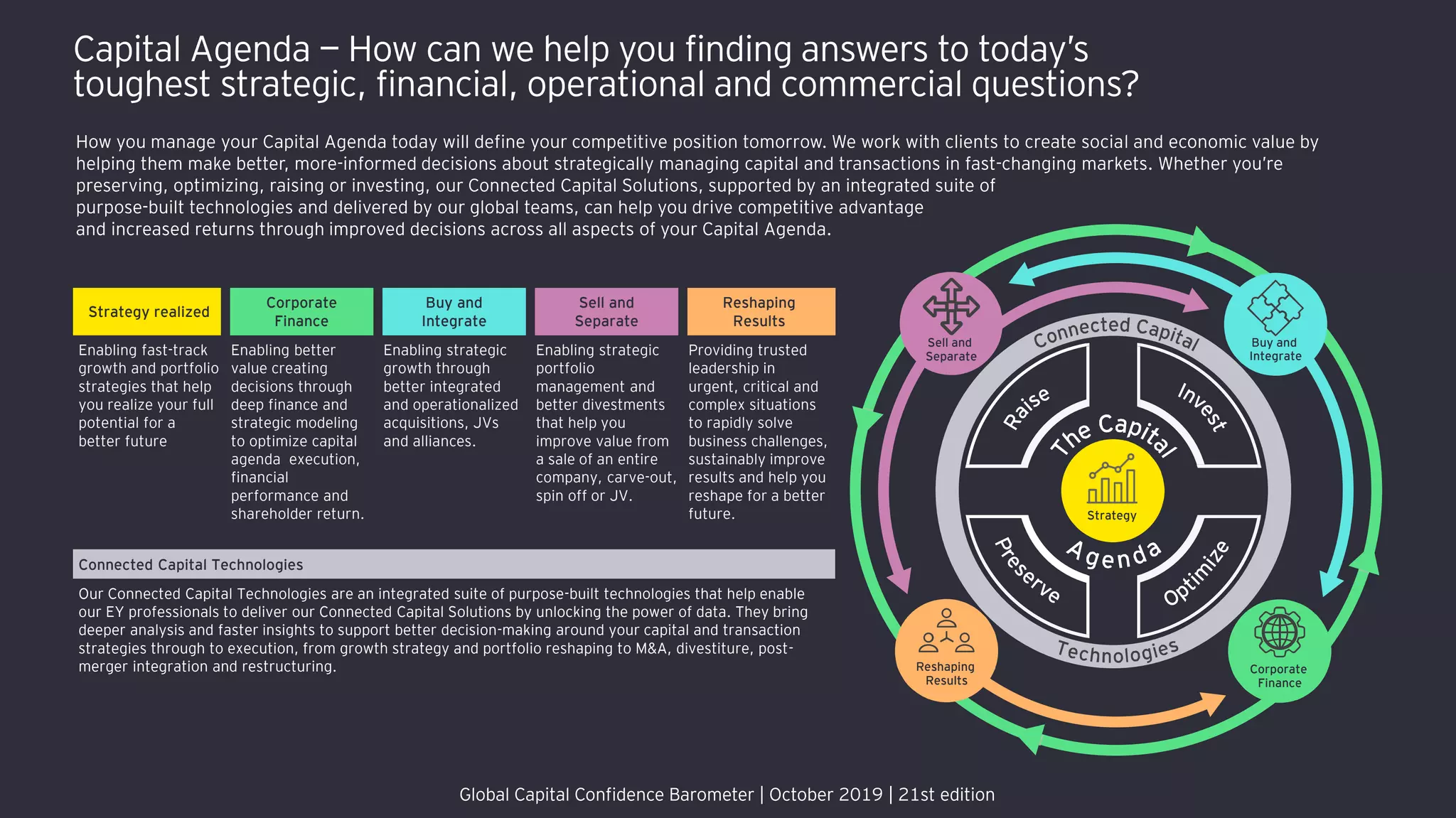

The October 2019 Global Capital Confidence Barometer indicates a strong outlook for mergers and acquisitions (M&A) despite geopolitical and economic uncertainties, with 52% of executives planning to pursue M&A in the next year. Executives are adapting to challenges by focusing on talent acquisition and digital transformation, highlighting a shift towards long-term value generation rather than just financial metrics. The report emphasizes the importance of social value metrics and assesses the expected improvements in the M&A market, with 68% of executives optimistic about its growth in the coming year.

![Where to Buy LinkedIn Accounts_ [12 Best Sites] (3).pdf](https://cdn.slidesharecdn.com/ss_thumbnails/wheretobuylinkedinaccounts12bestsites3-251124162550-95b6ddfa-thumbnail.jpg?width=640&height=640&fit=bounds)