Download to read offline

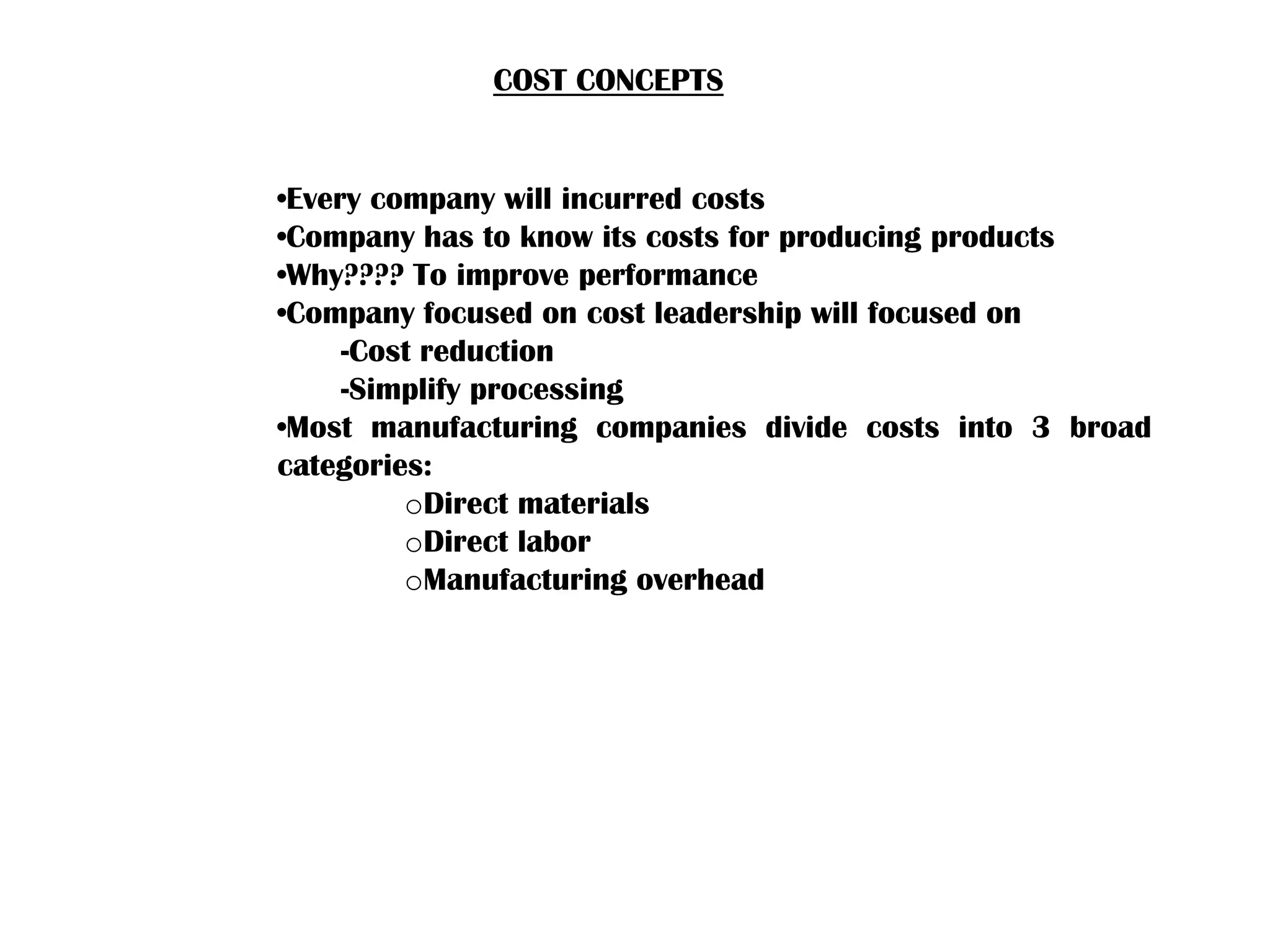

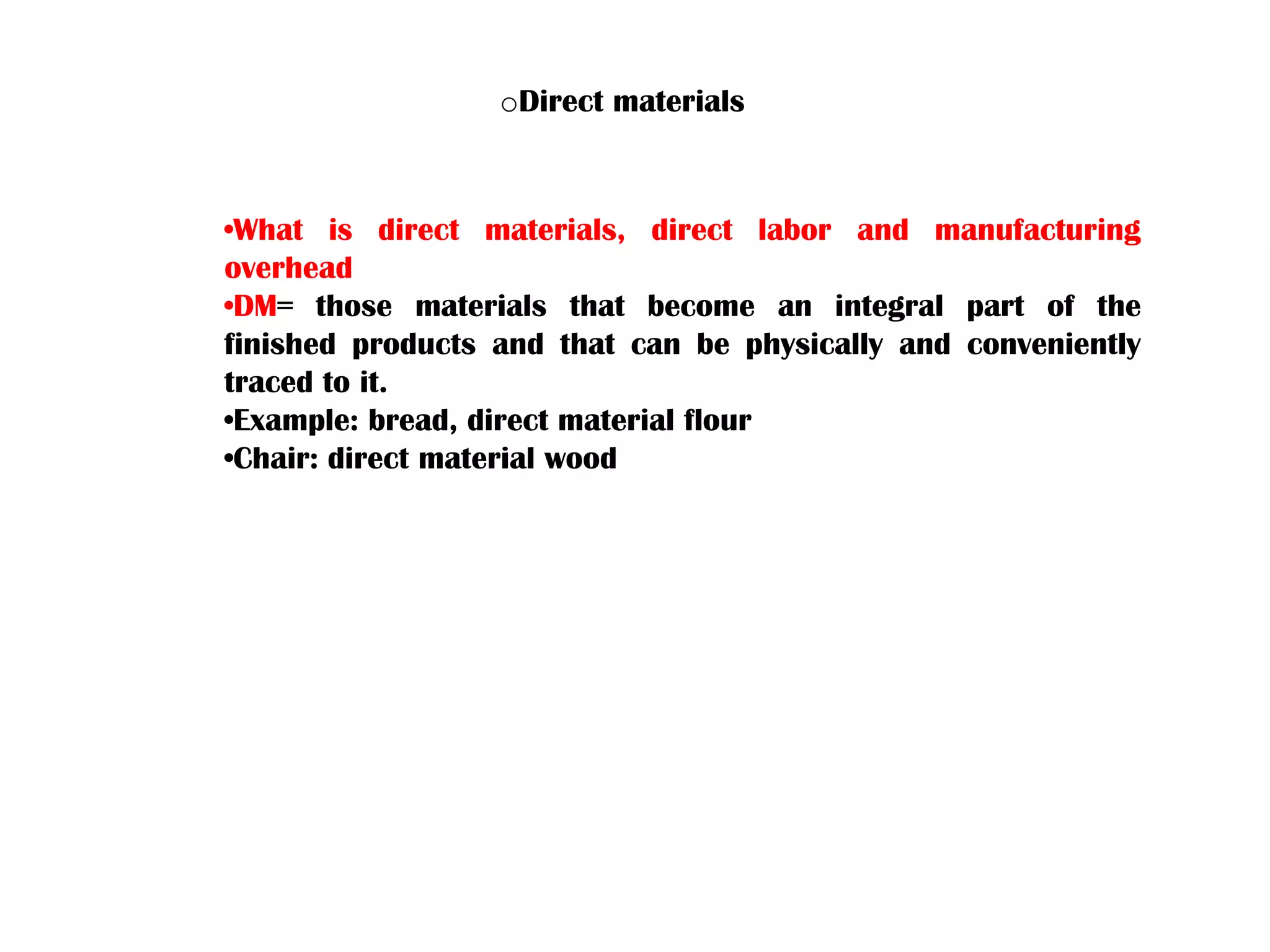

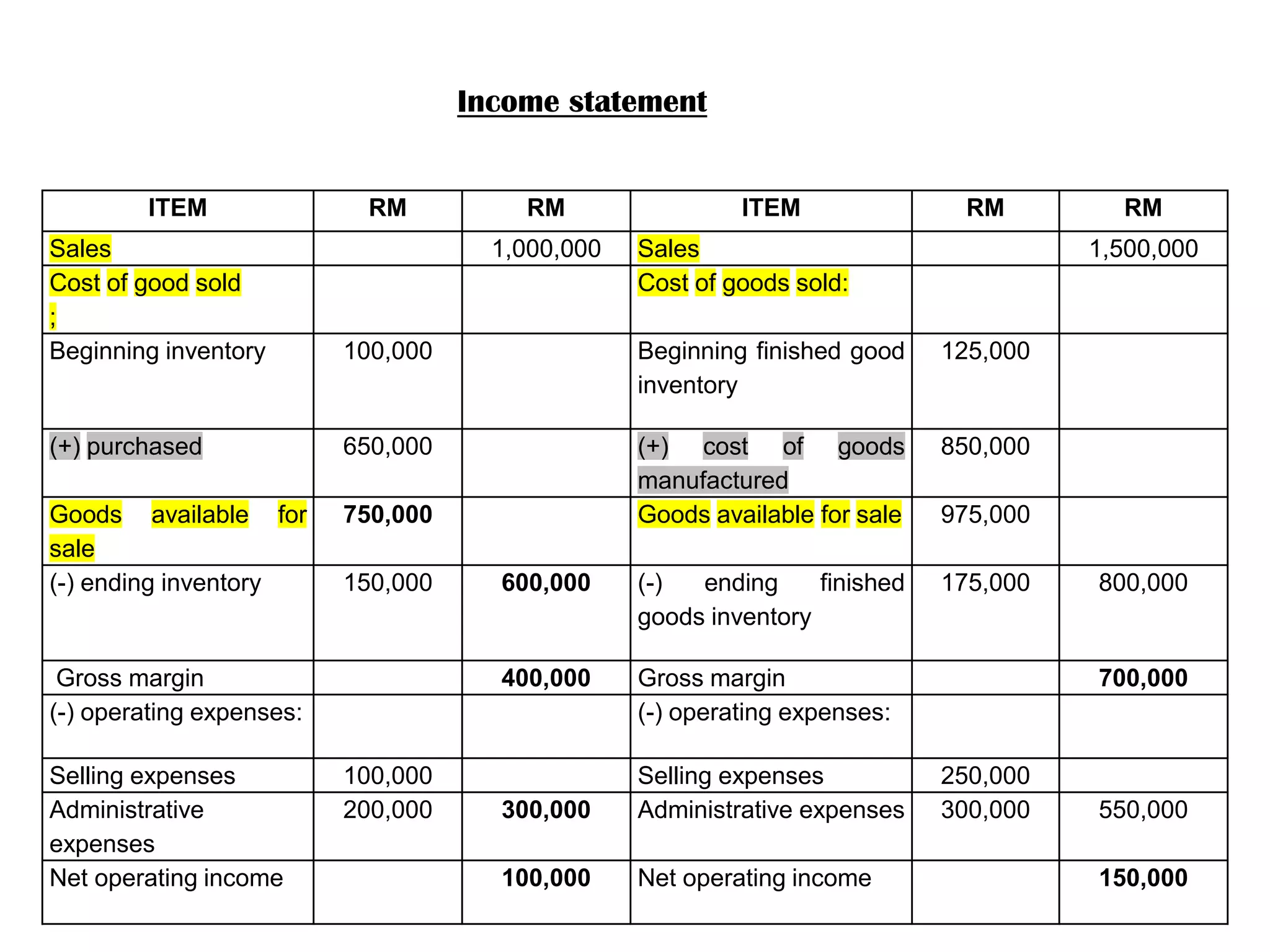

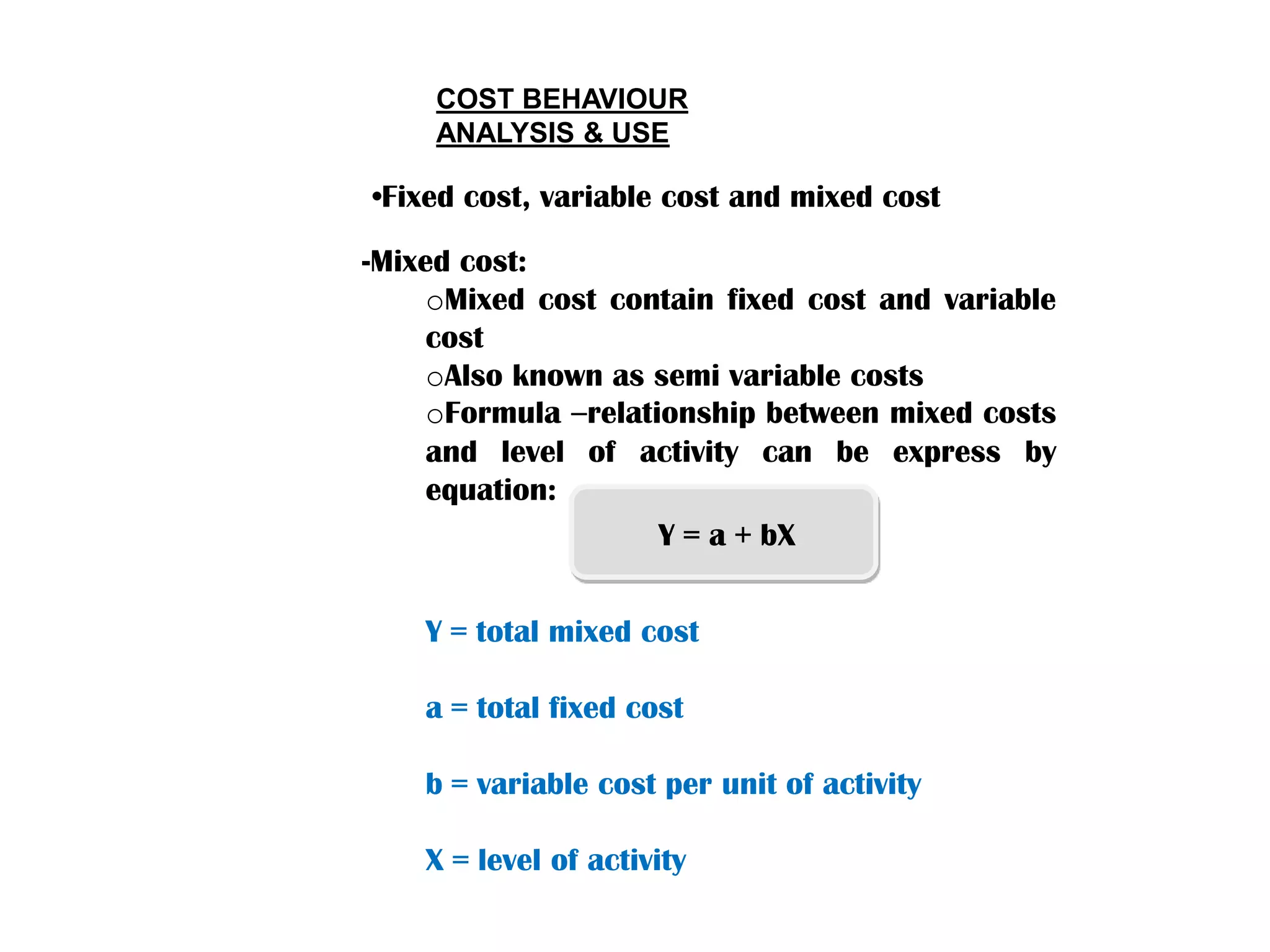

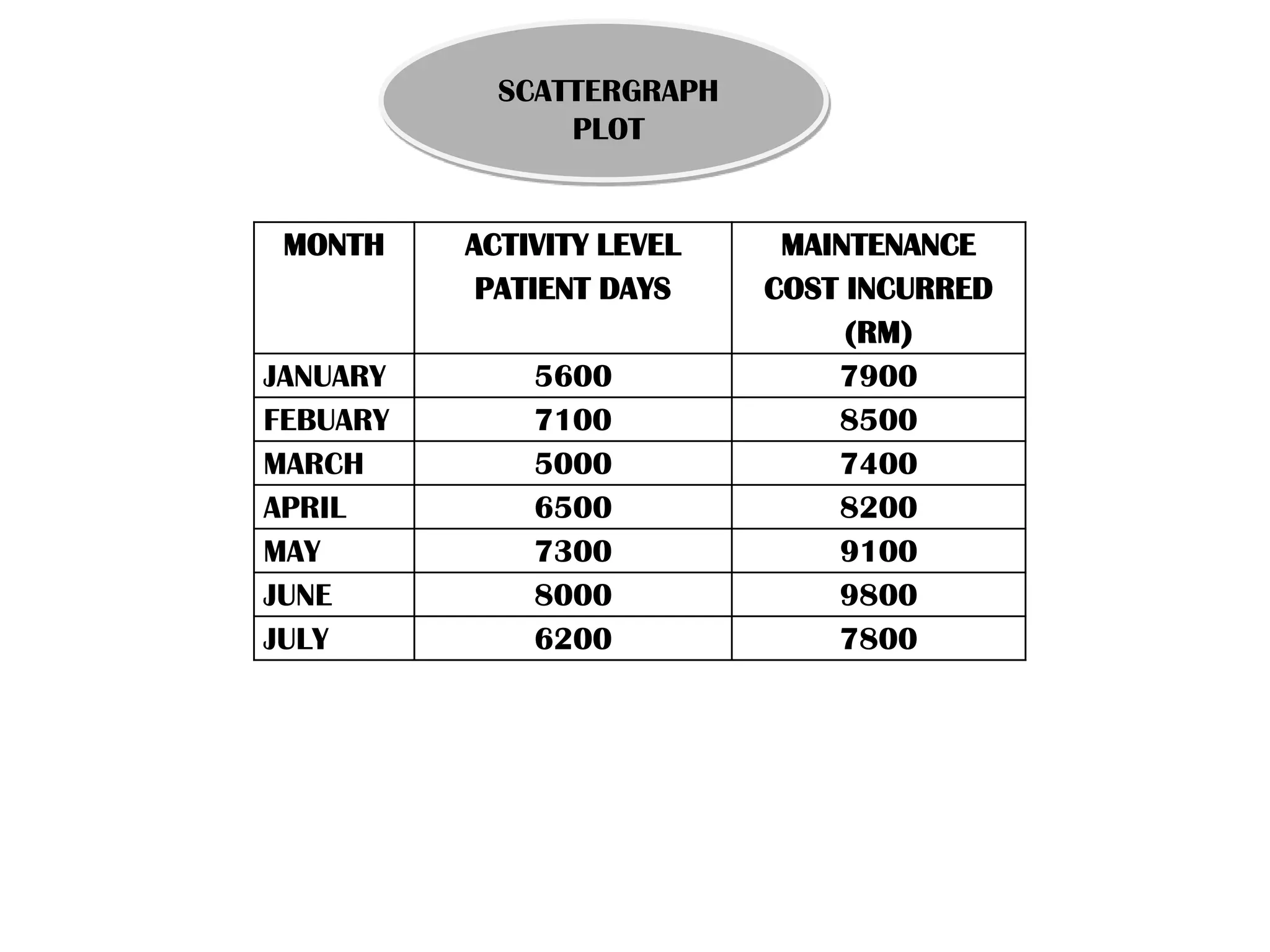

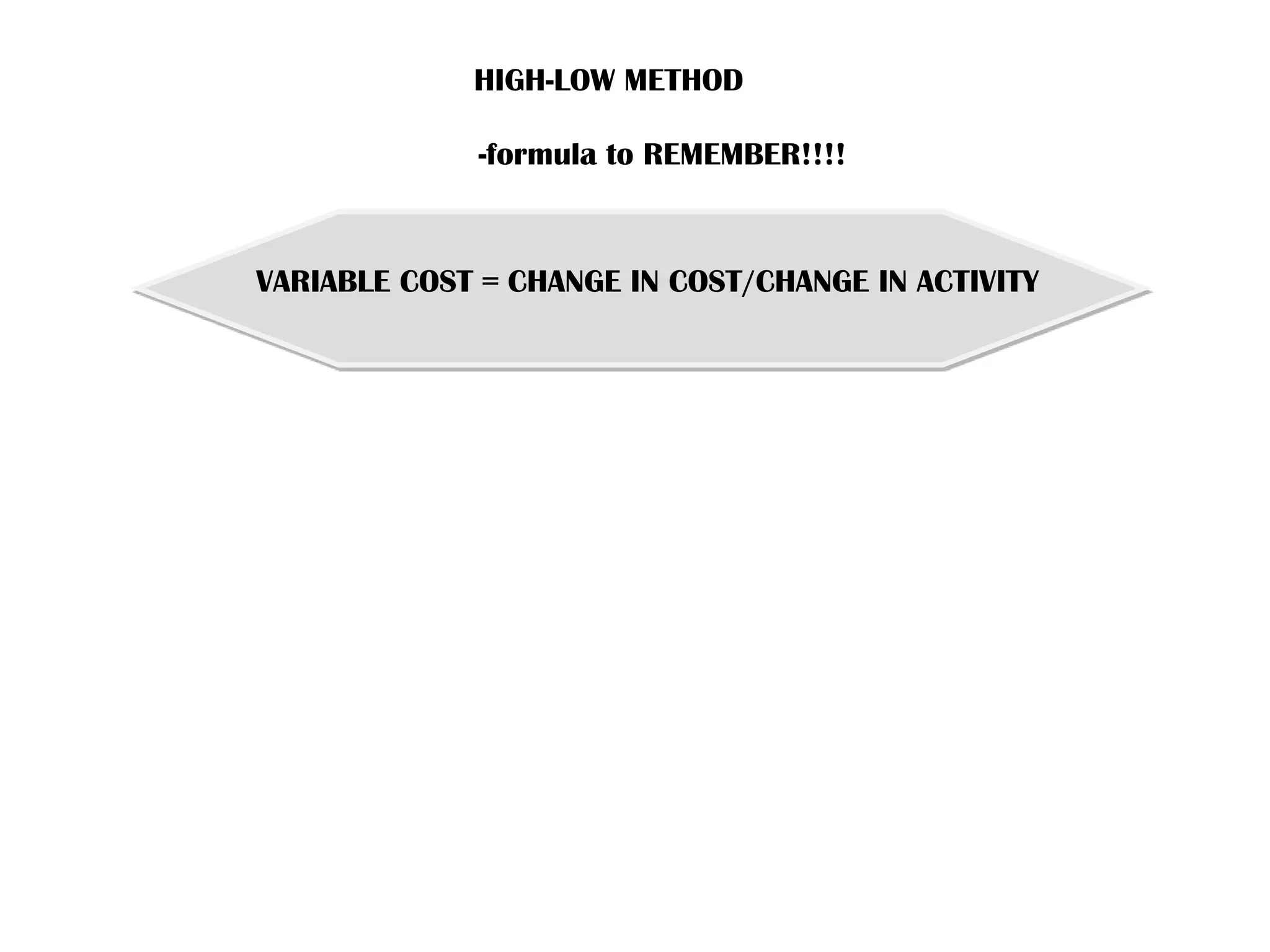

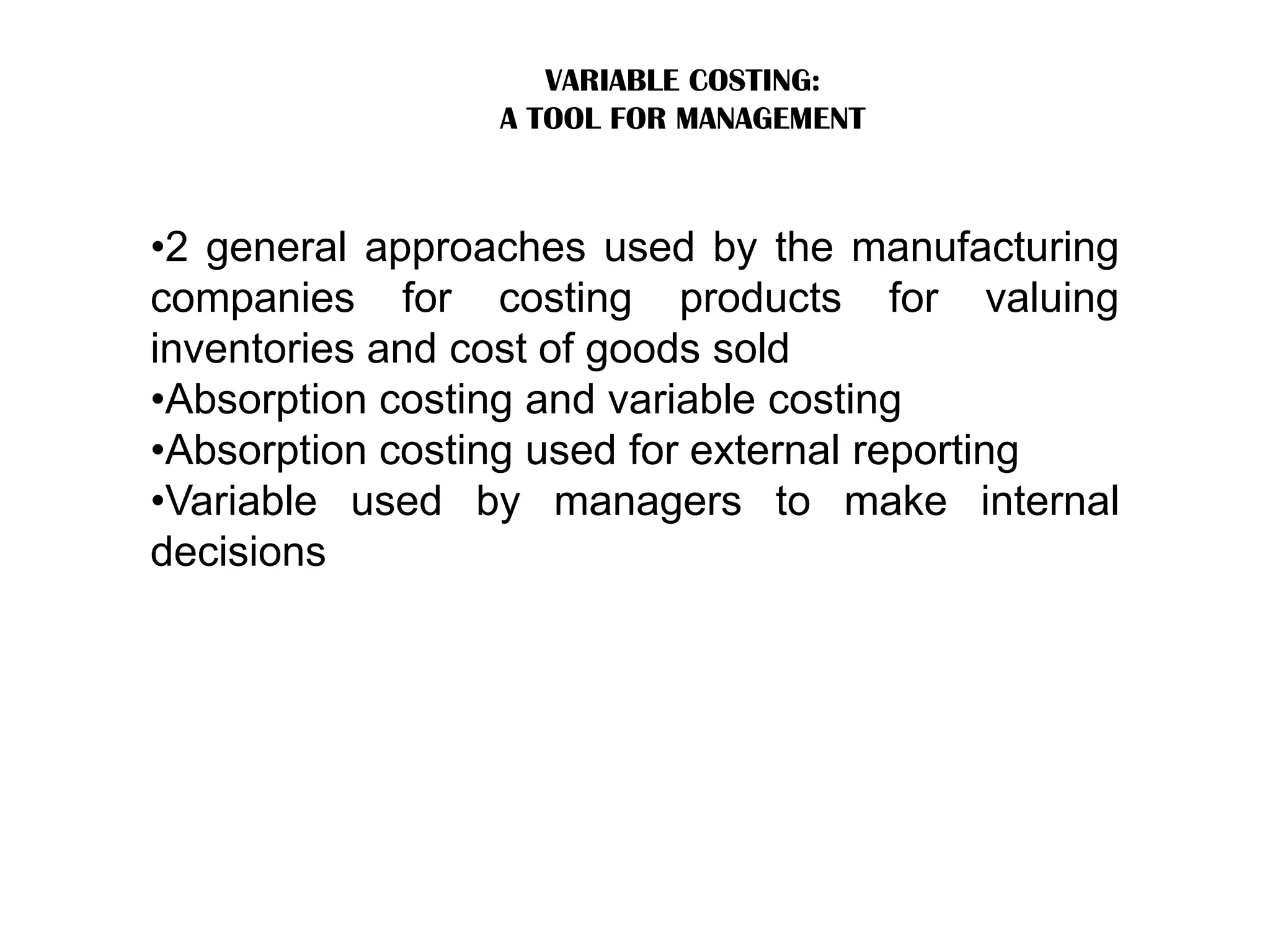

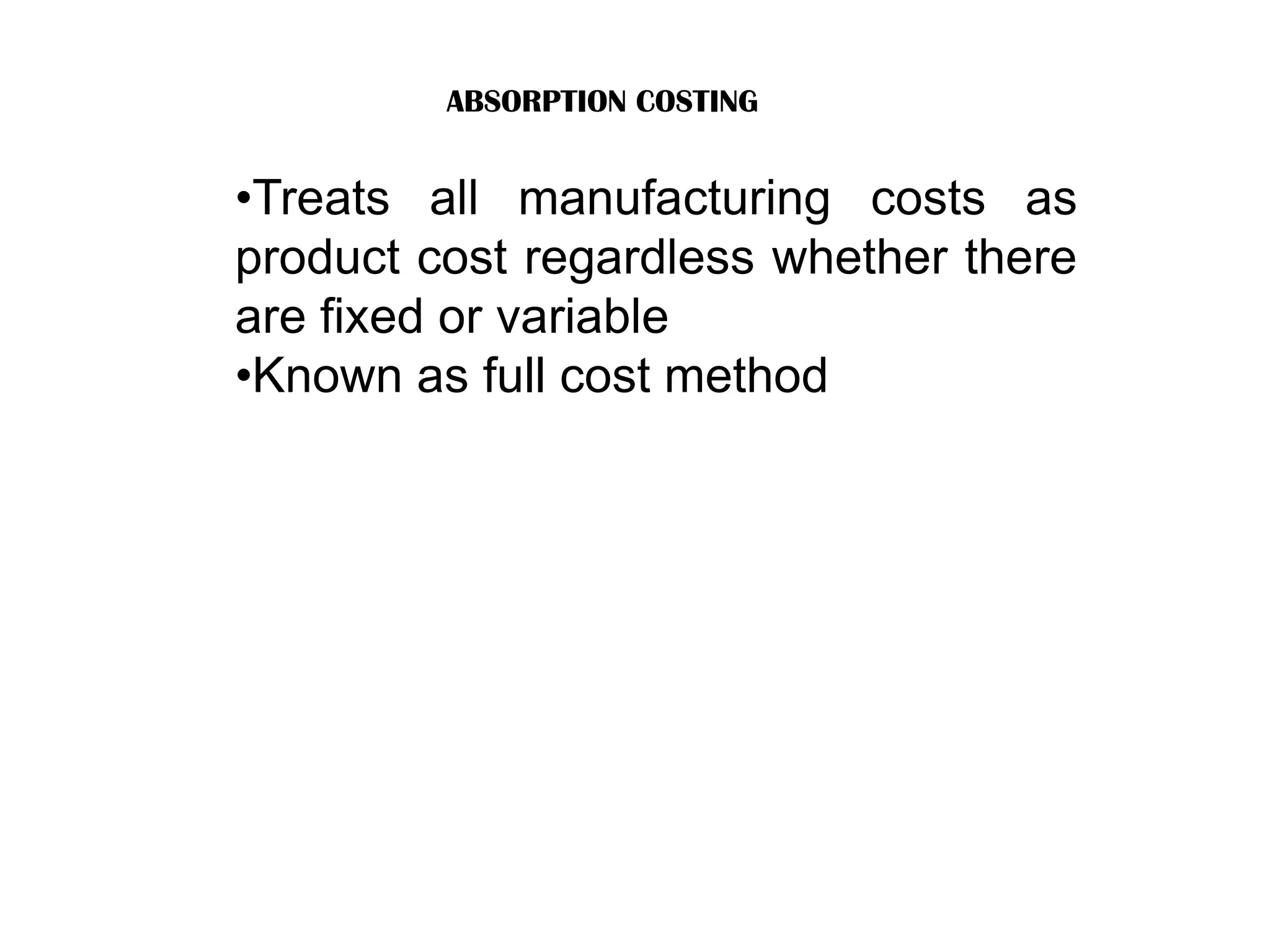

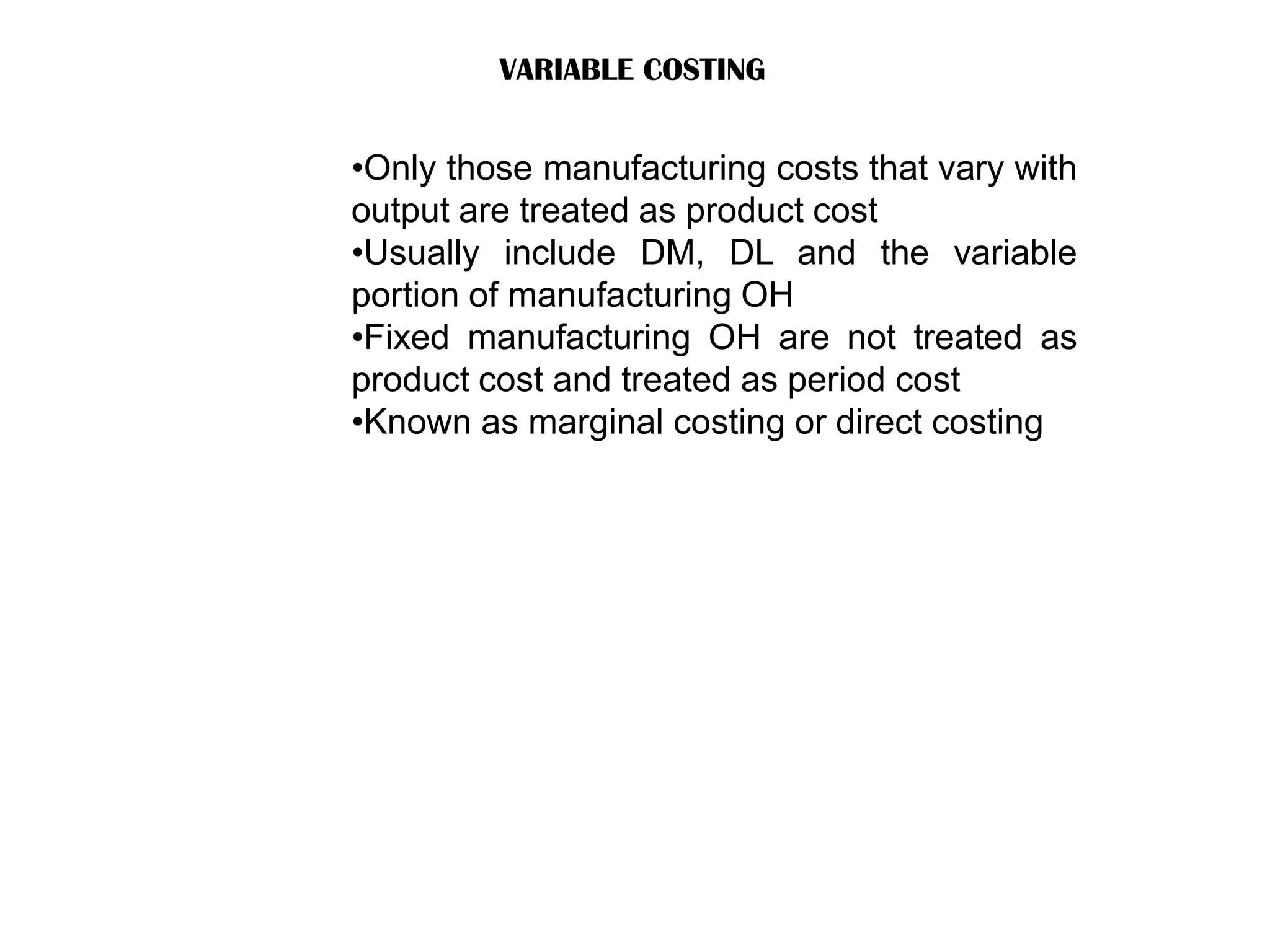

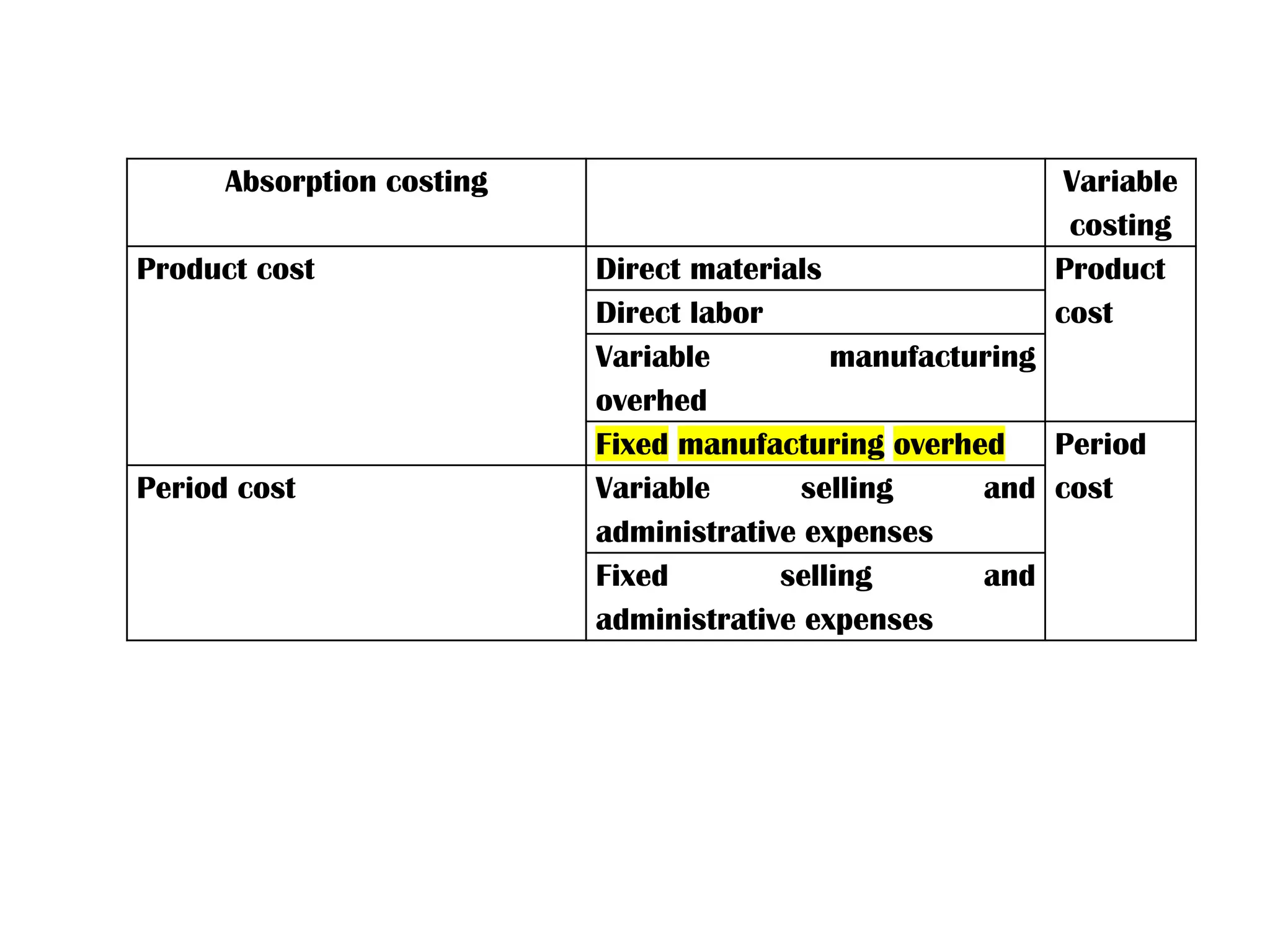

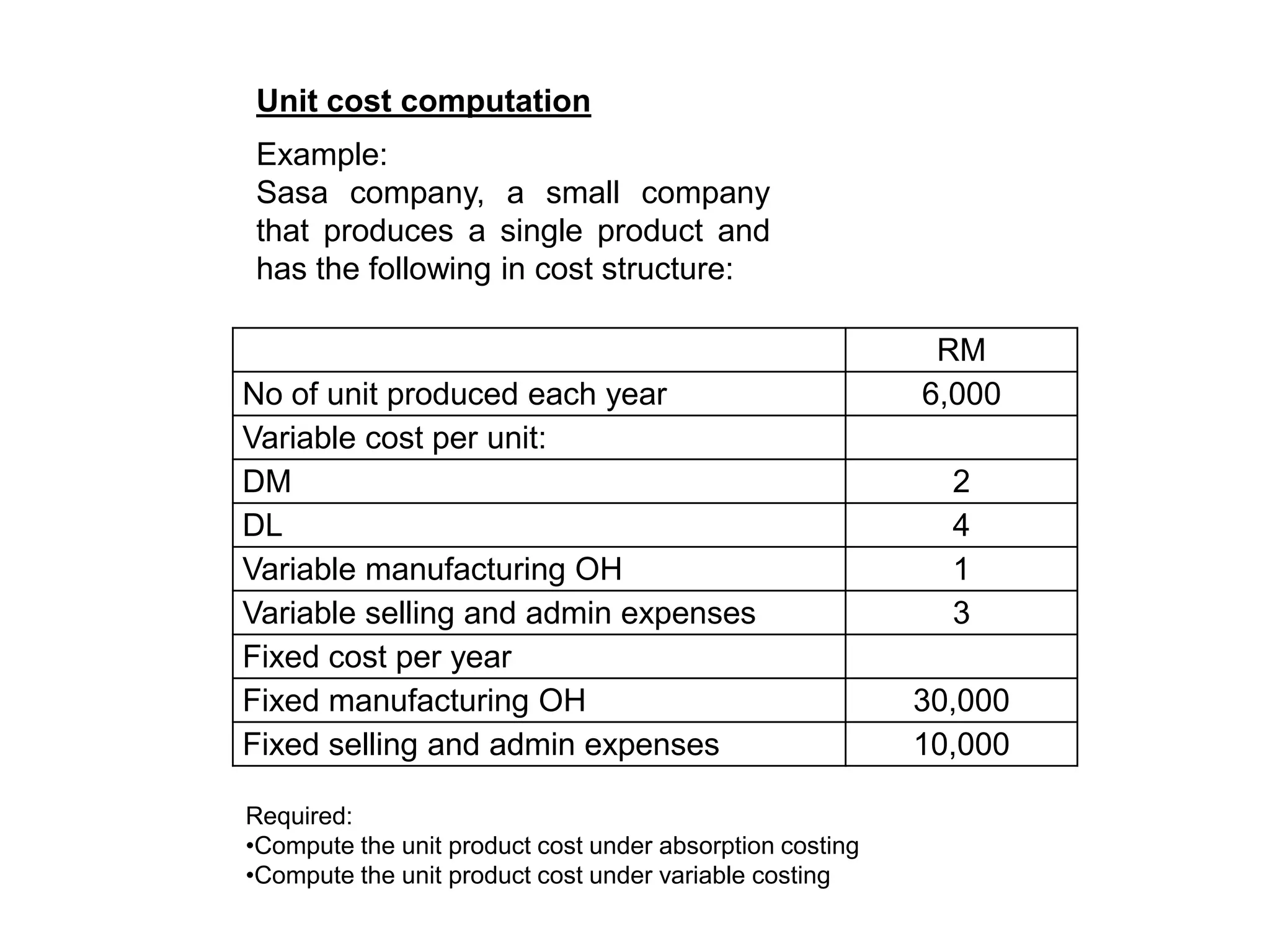

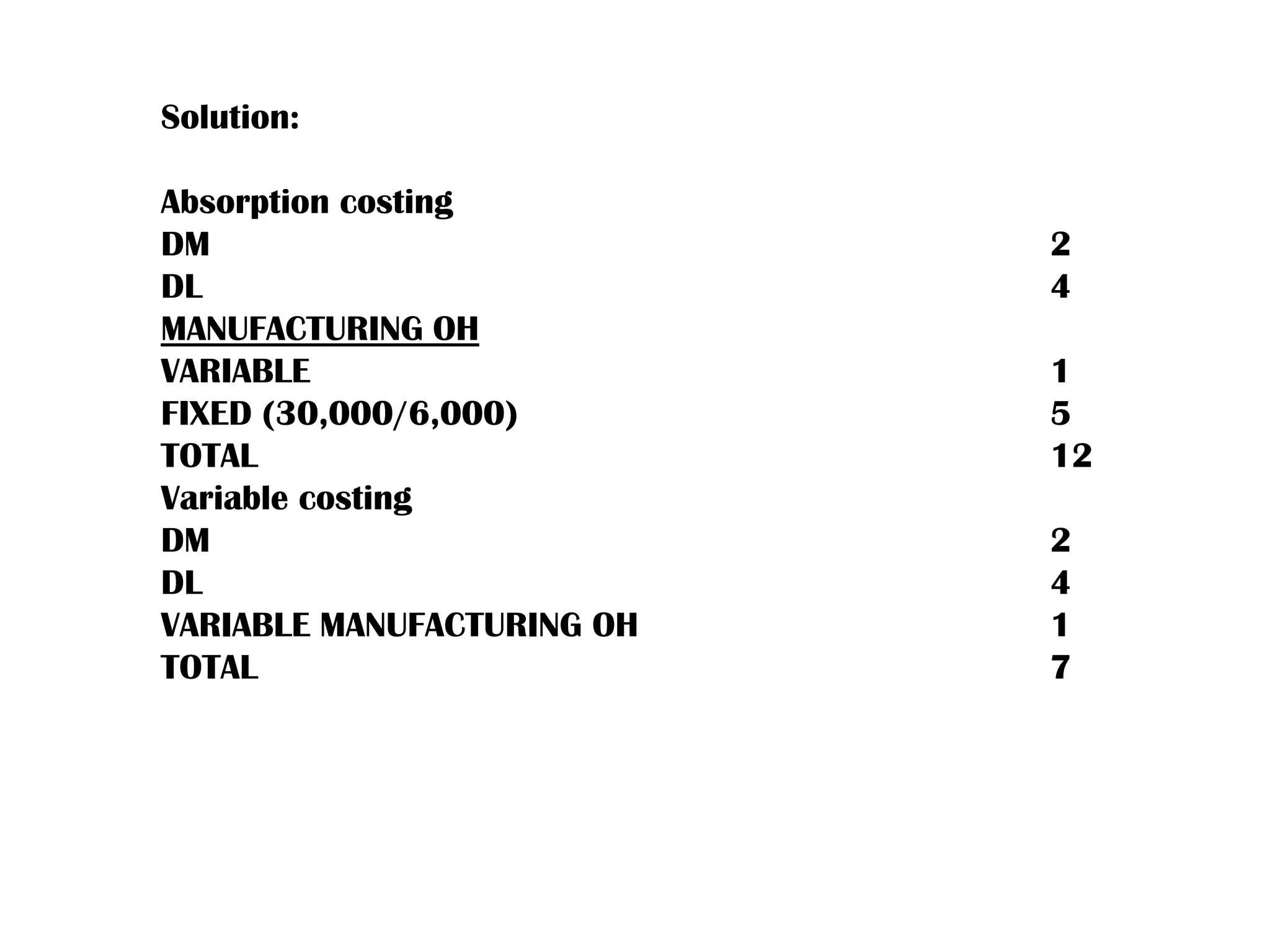

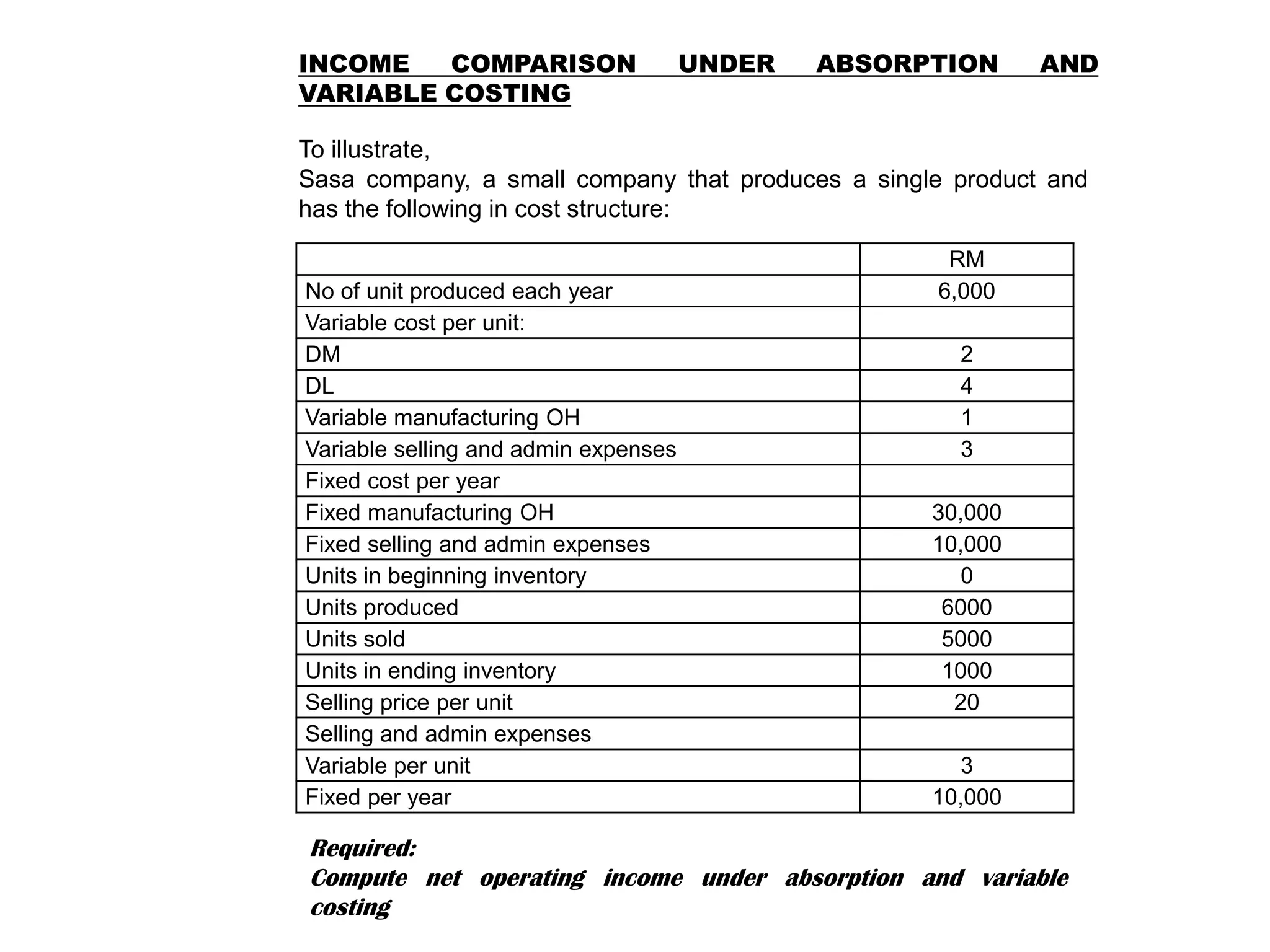

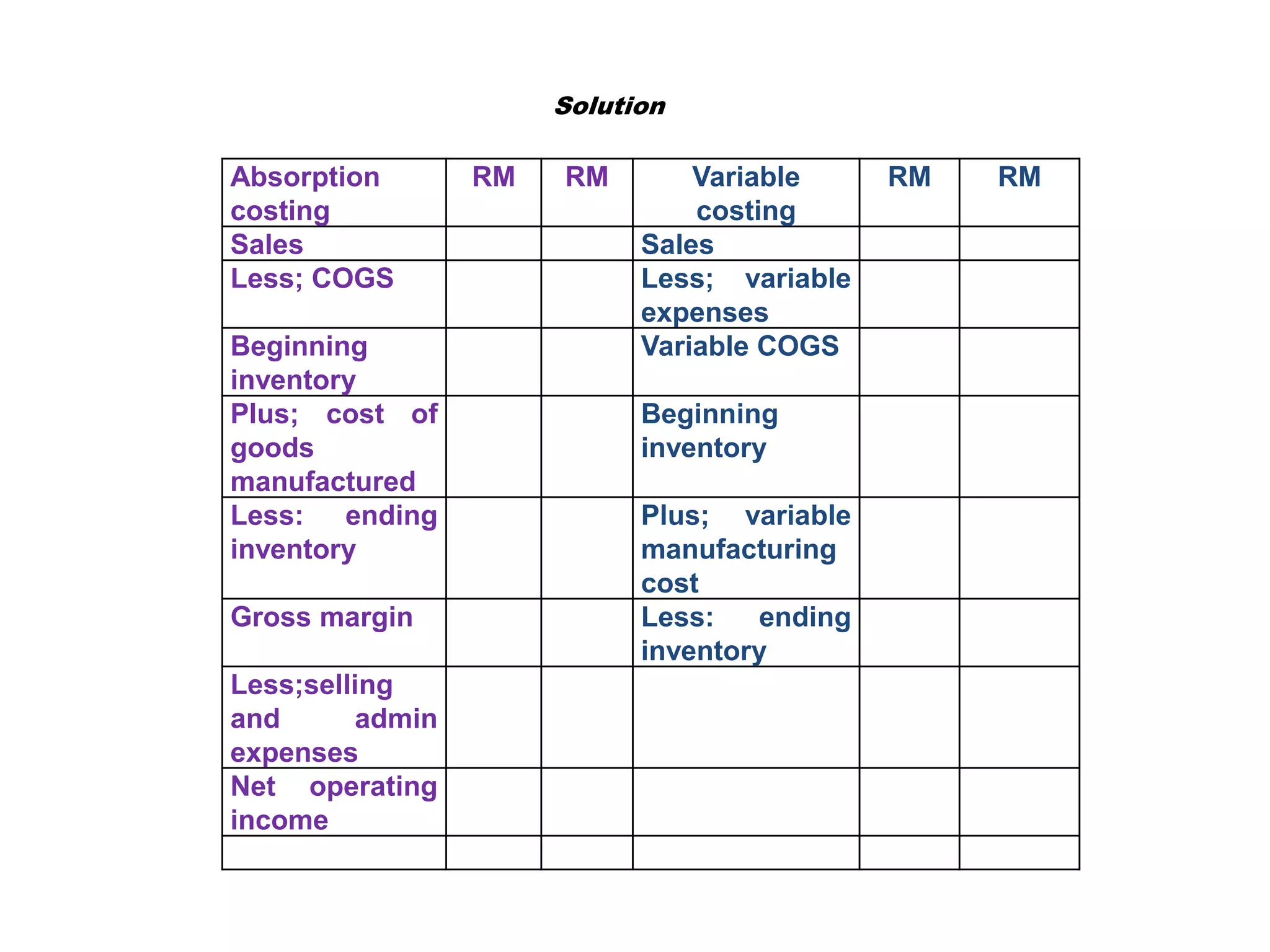

- The document discusses various cost concepts including direct materials, direct labor, manufacturing overhead, product costs, period costs, fixed costs, variable costs, mixed costs, sunk costs, opportunity costs, and incremental costs. - It also compares absorption costing and variable costing methods for valuing inventory and calculating cost of goods sold and net operating income. Absorption costing includes both fixed and variable manufacturing overhead in product costs while variable costing only includes variable costs. - Various cost classification and analysis techniques are presented including cost behavior analysis using scatter graphs, regression, and the high-low method to determine the fixed and variable components of mixed costs.

![[TUTORING SESSION KÌ I - 2021] Final Handbook MA.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/tutoringsessionkii-2021finalhandbookma-221130064059-cd42703e-thumbnail.jpg?width=640&height=640&fit=bounds)