Download as PDF, PPTX

The document discusses the importance of data integrity in backtesting trading strategies, highlighting that poor data can lead to inflated backtest performance. It provides examples of trading strategies, including mean reversion and intraday momentum, underscoring the difference in performance outcomes when using various price data sources. The conclusion stresses that the type of historical data required depends on both execution price determination and trading signal triggering.

Introduction to Dr. Ernest Chan and his background in algorithmic trading and machine learning.

GIGO principle; emphasizes data integrity's crucial role in backtesting trading strategies.

Mean reversion trading strategy for Closed-End Funds (CEF); includes results from backtests.

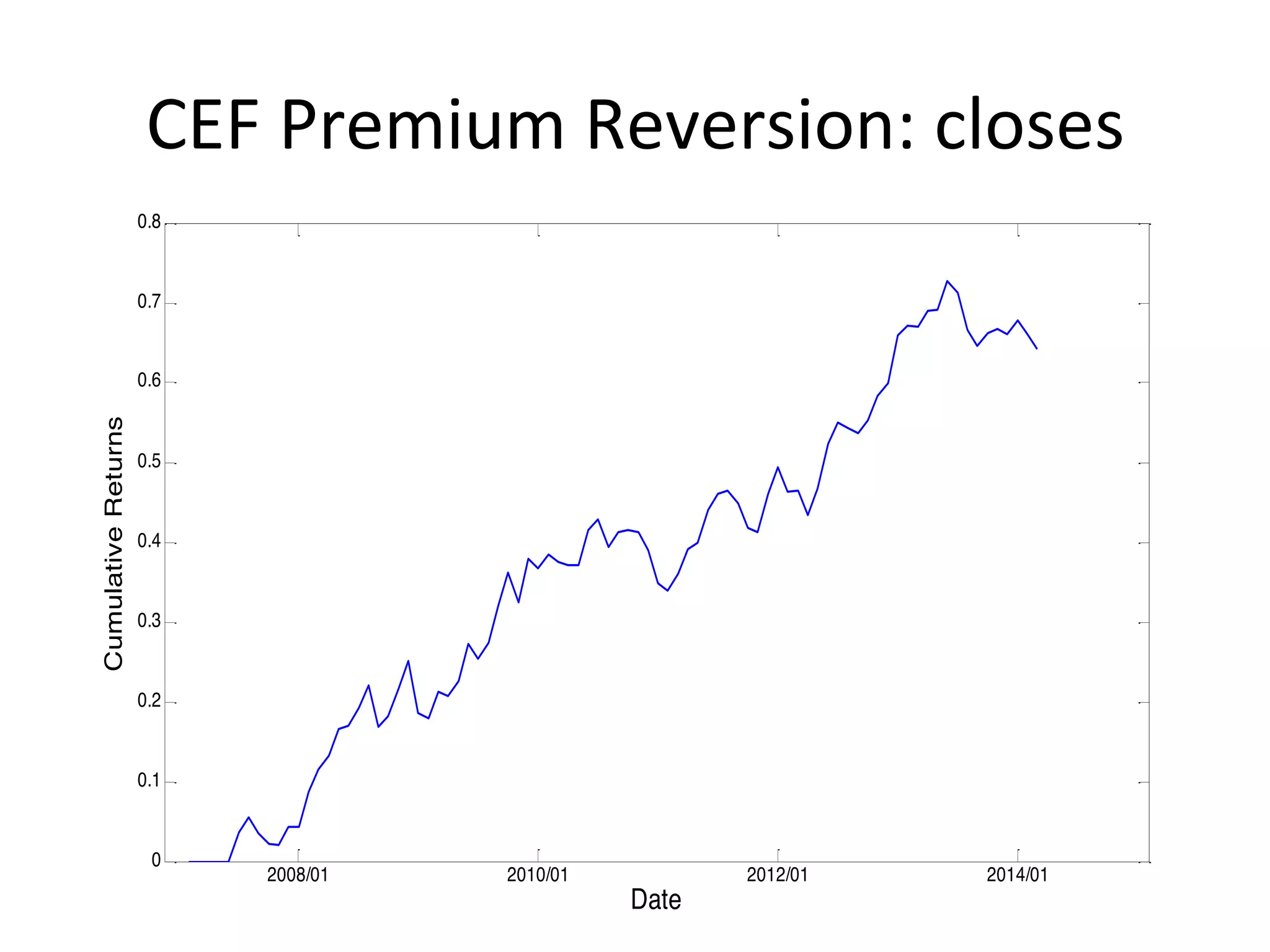

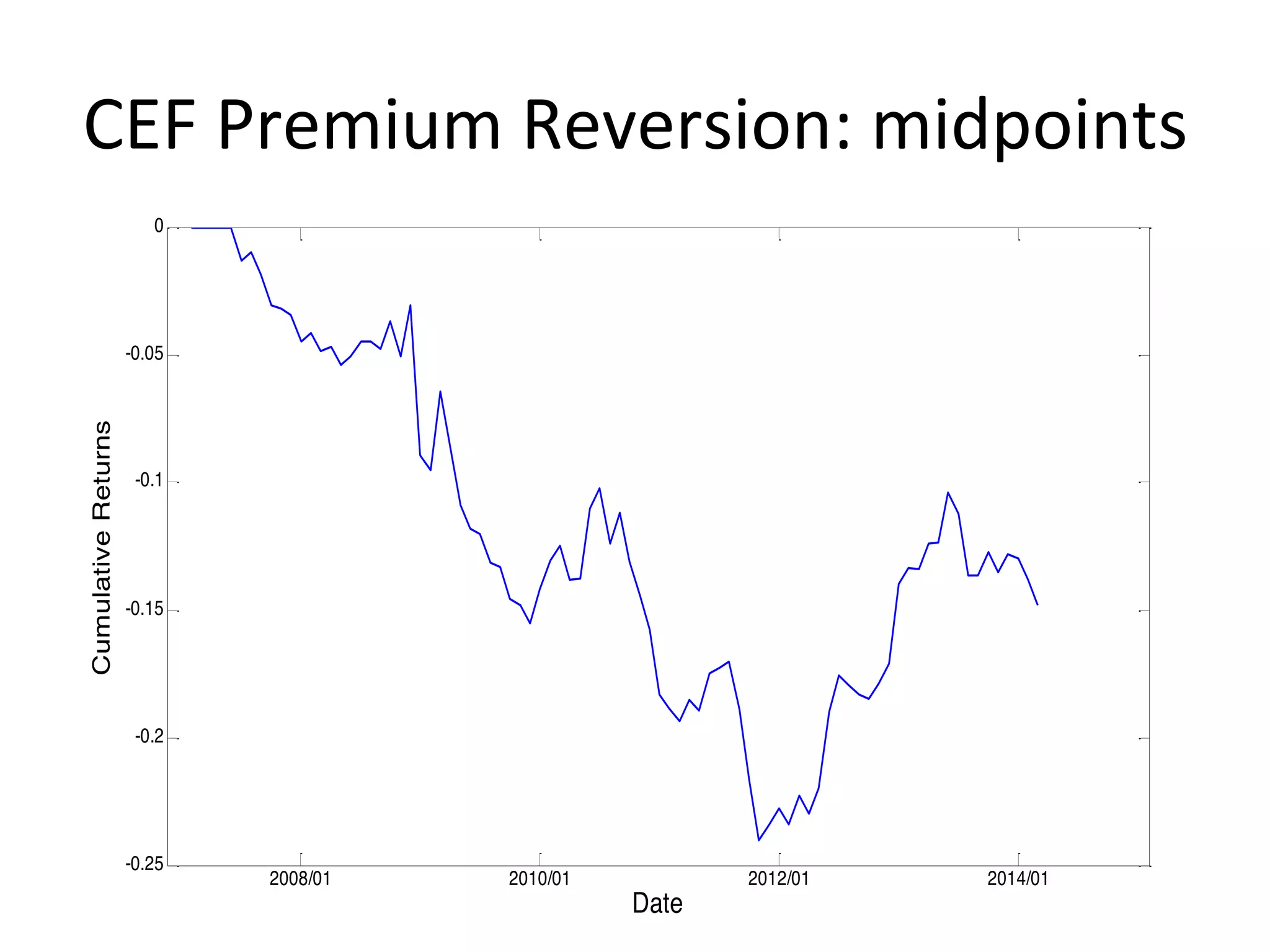

Charts displaying cumulative returns and performance metrics of CEF Premium Reversion strategy.

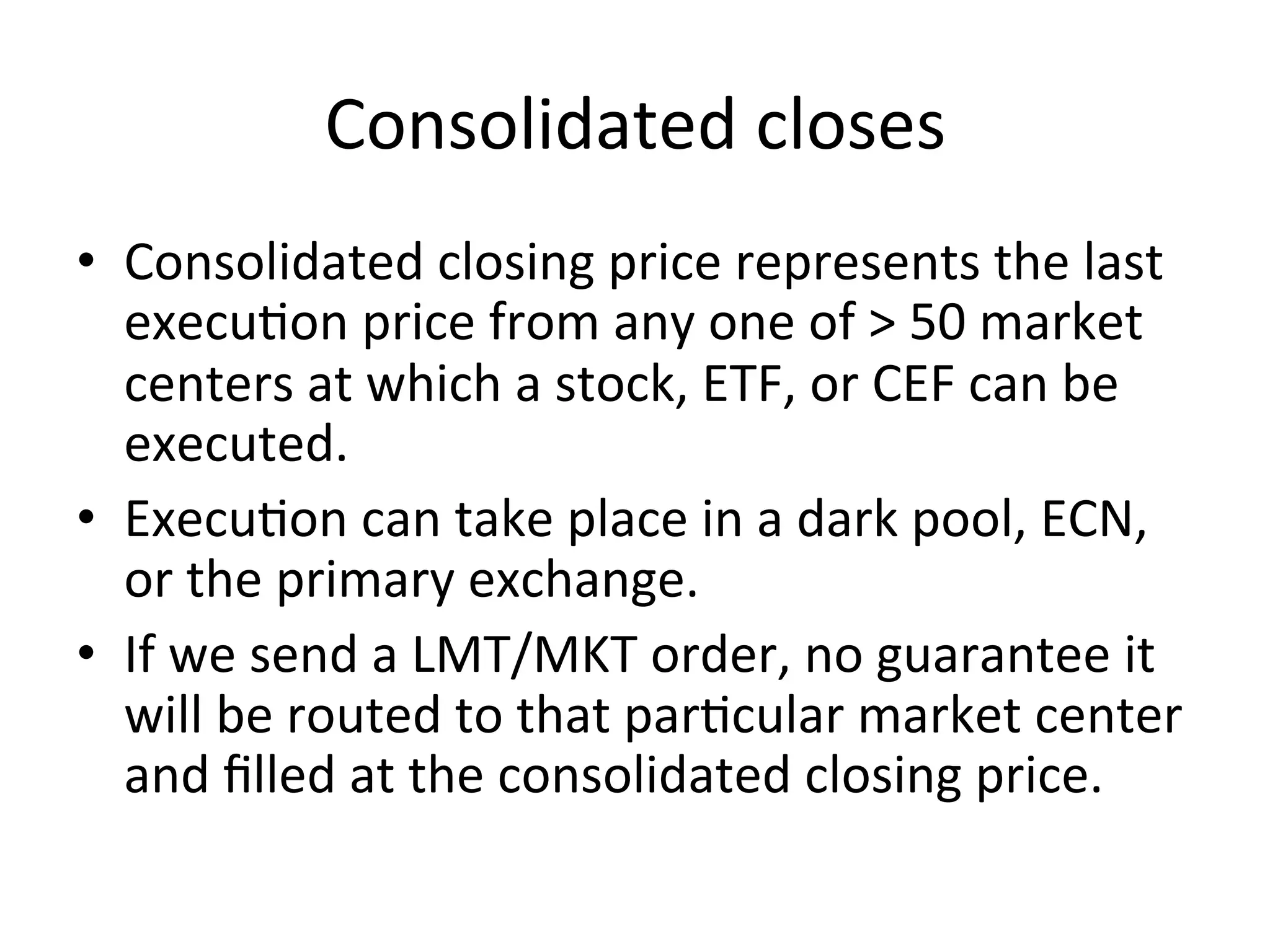

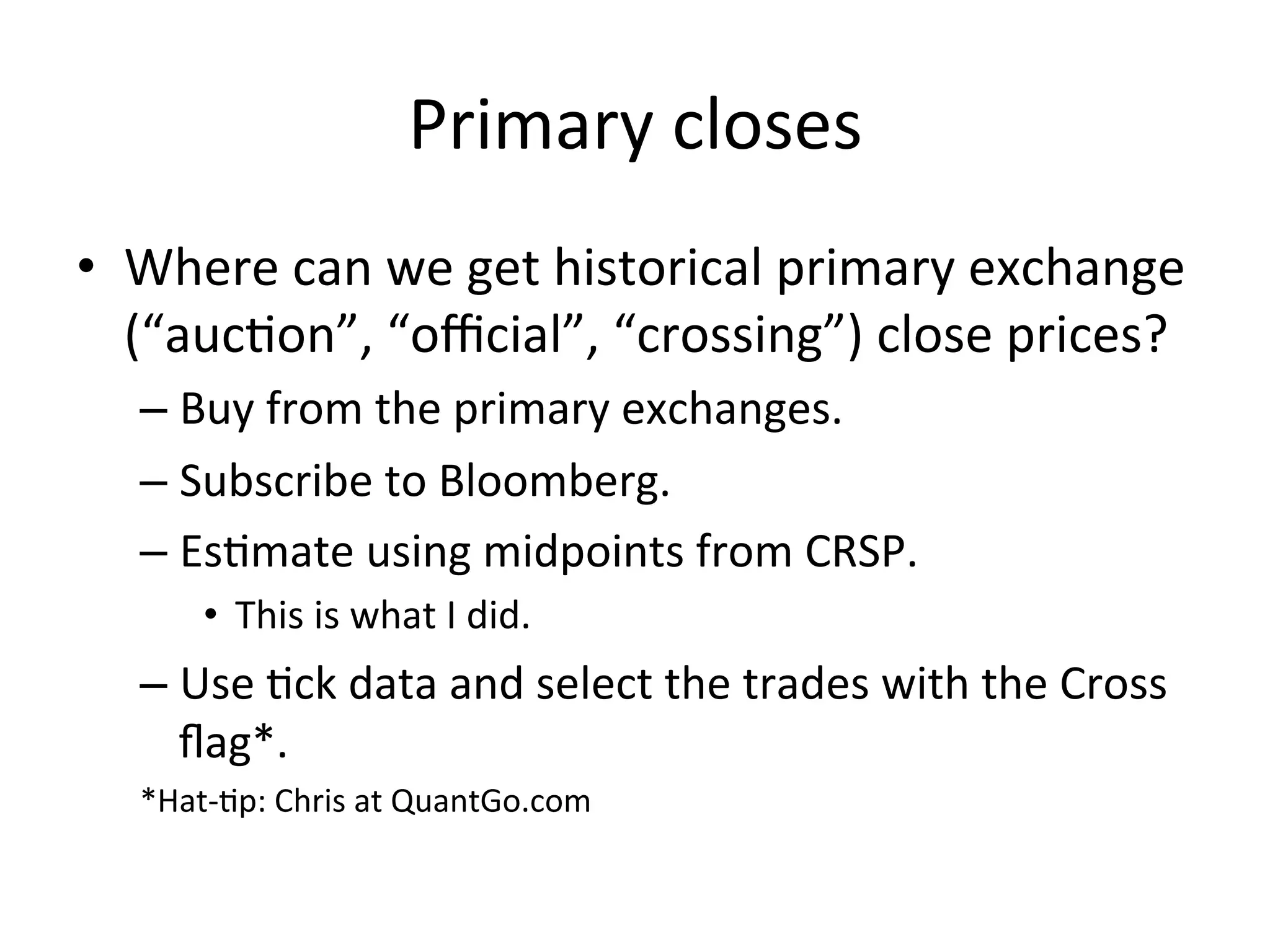

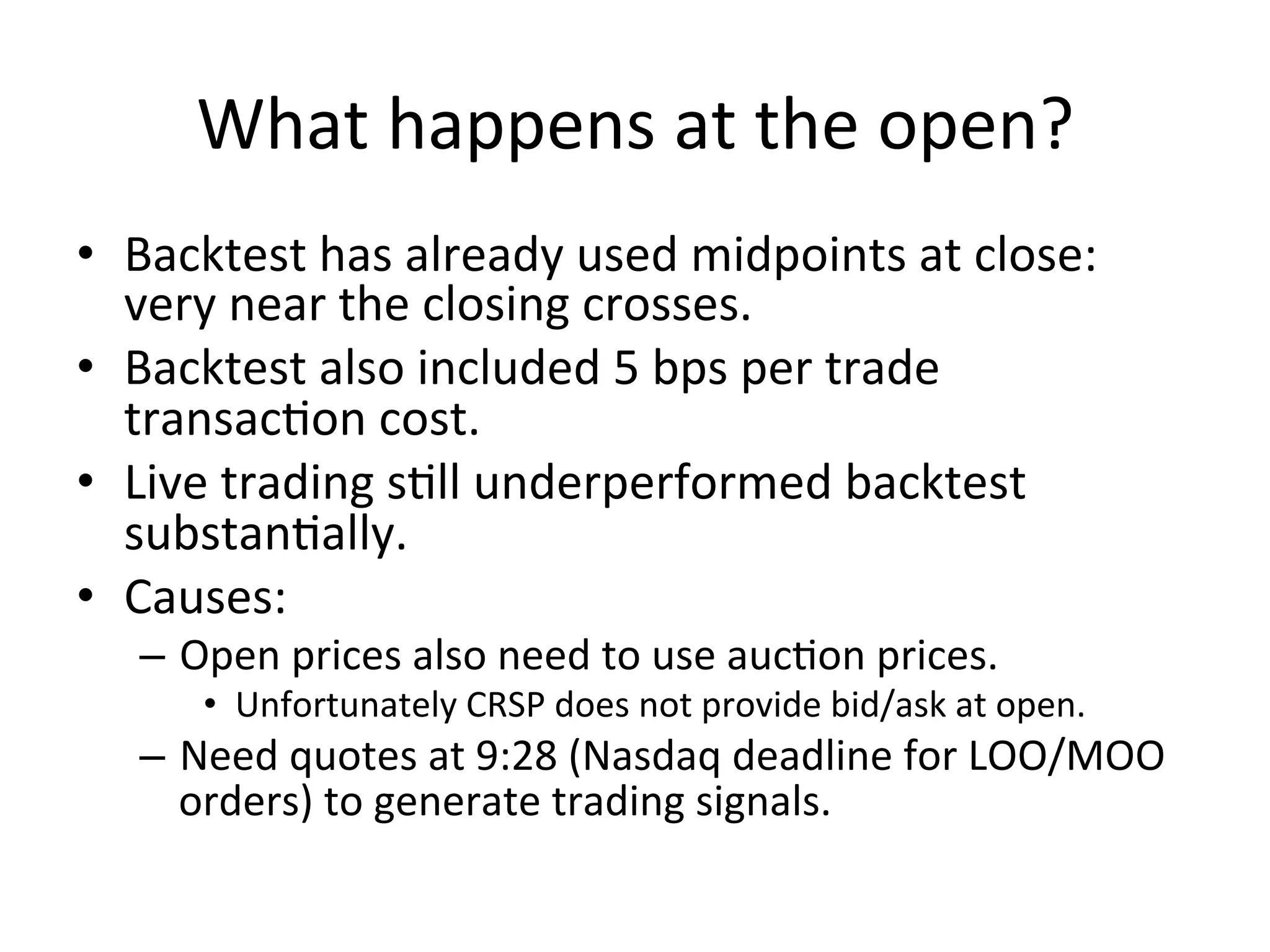

Differing results from using closing prices vs. midpoints; need for accurate execution data.

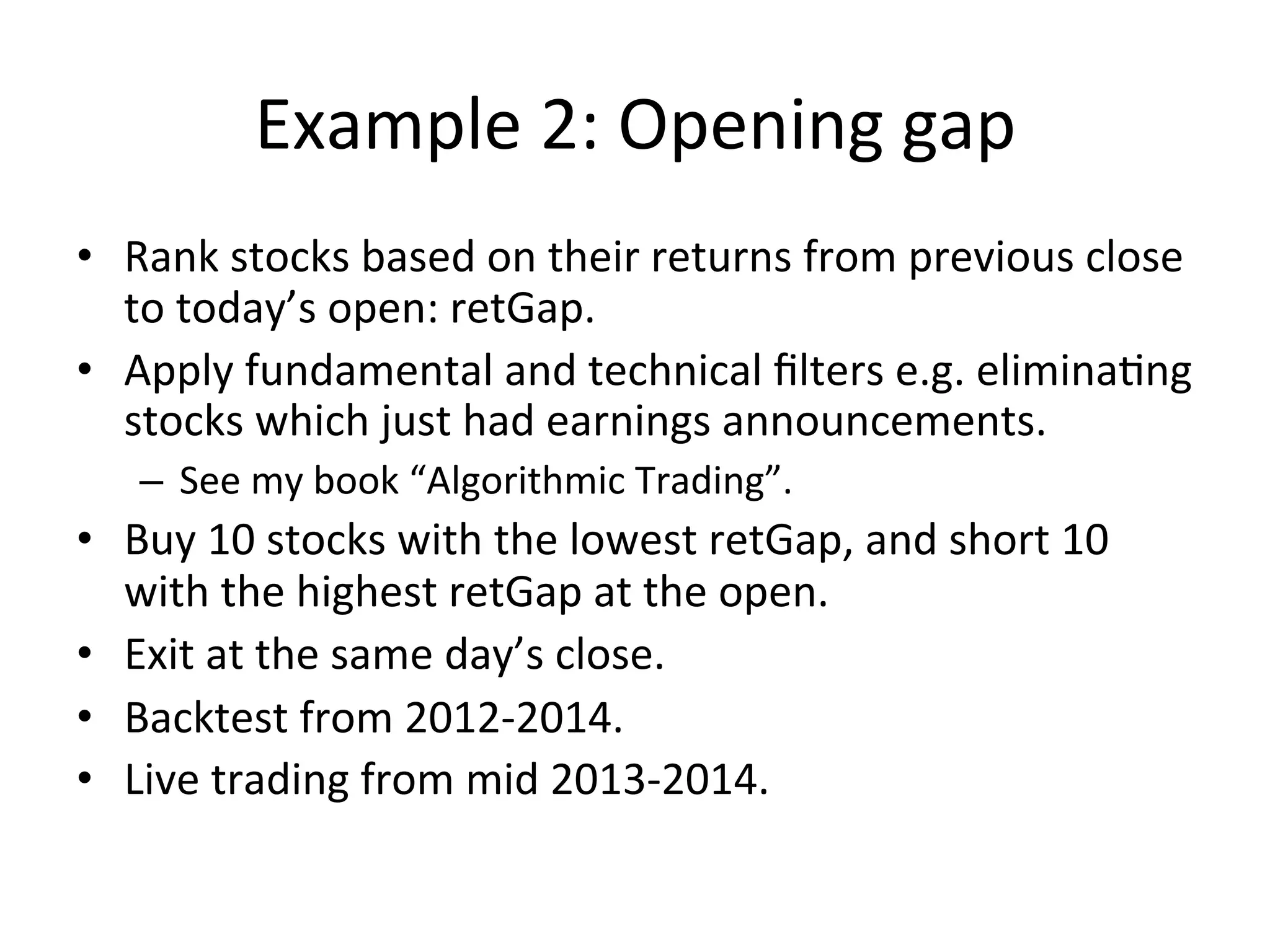

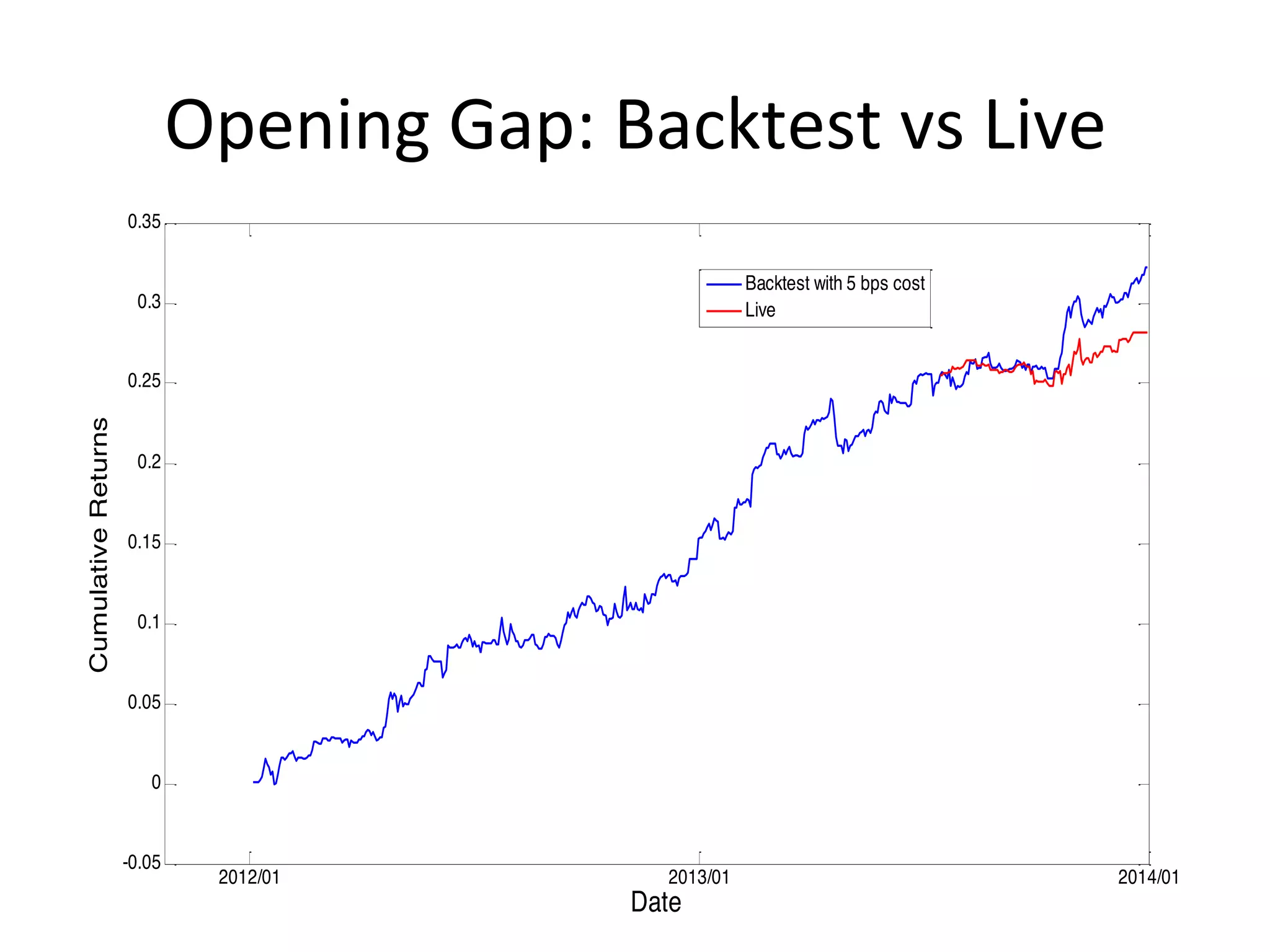

Strategy based on rank of returns from previous close to today's open; backtest and live performance.

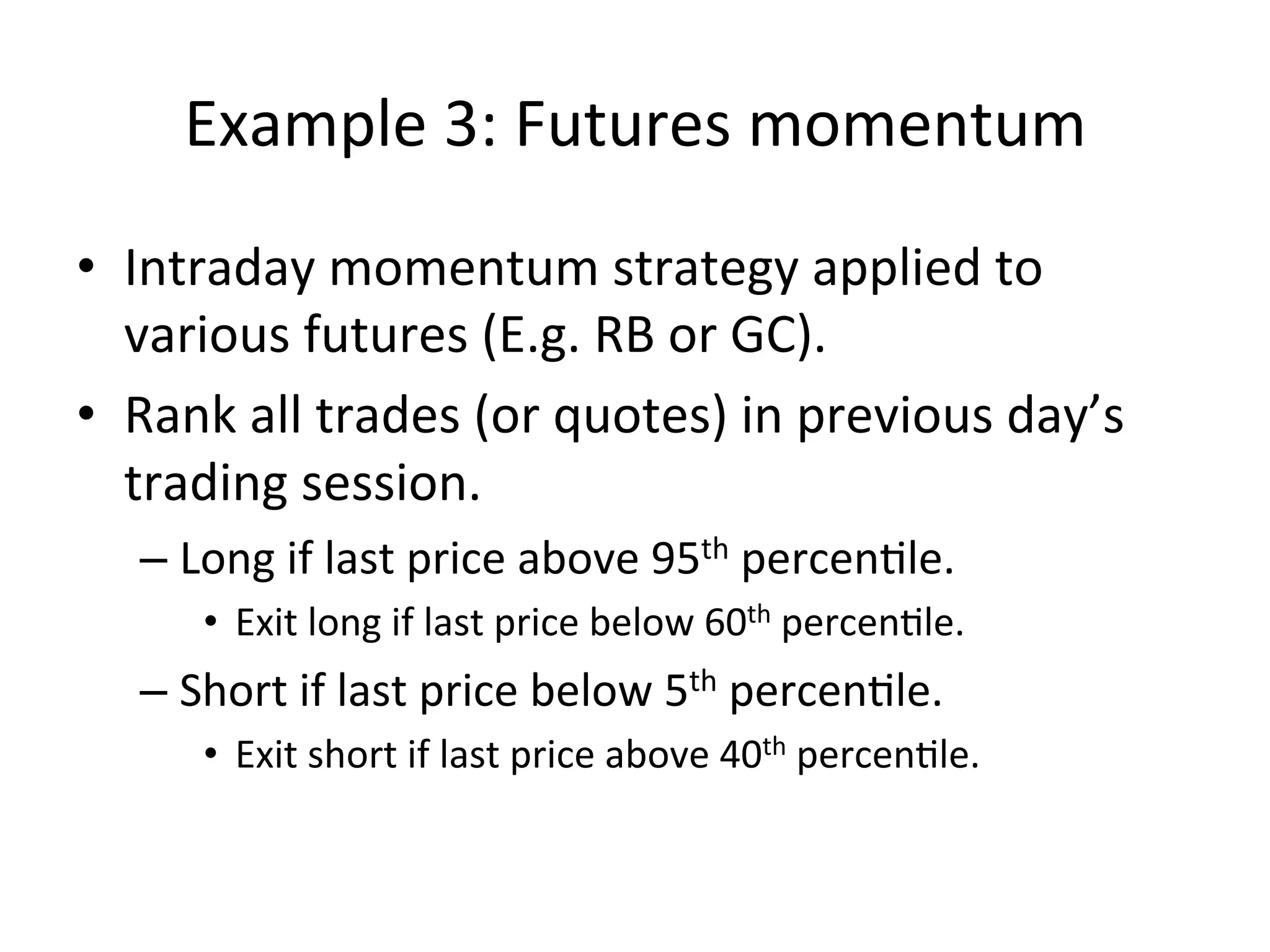

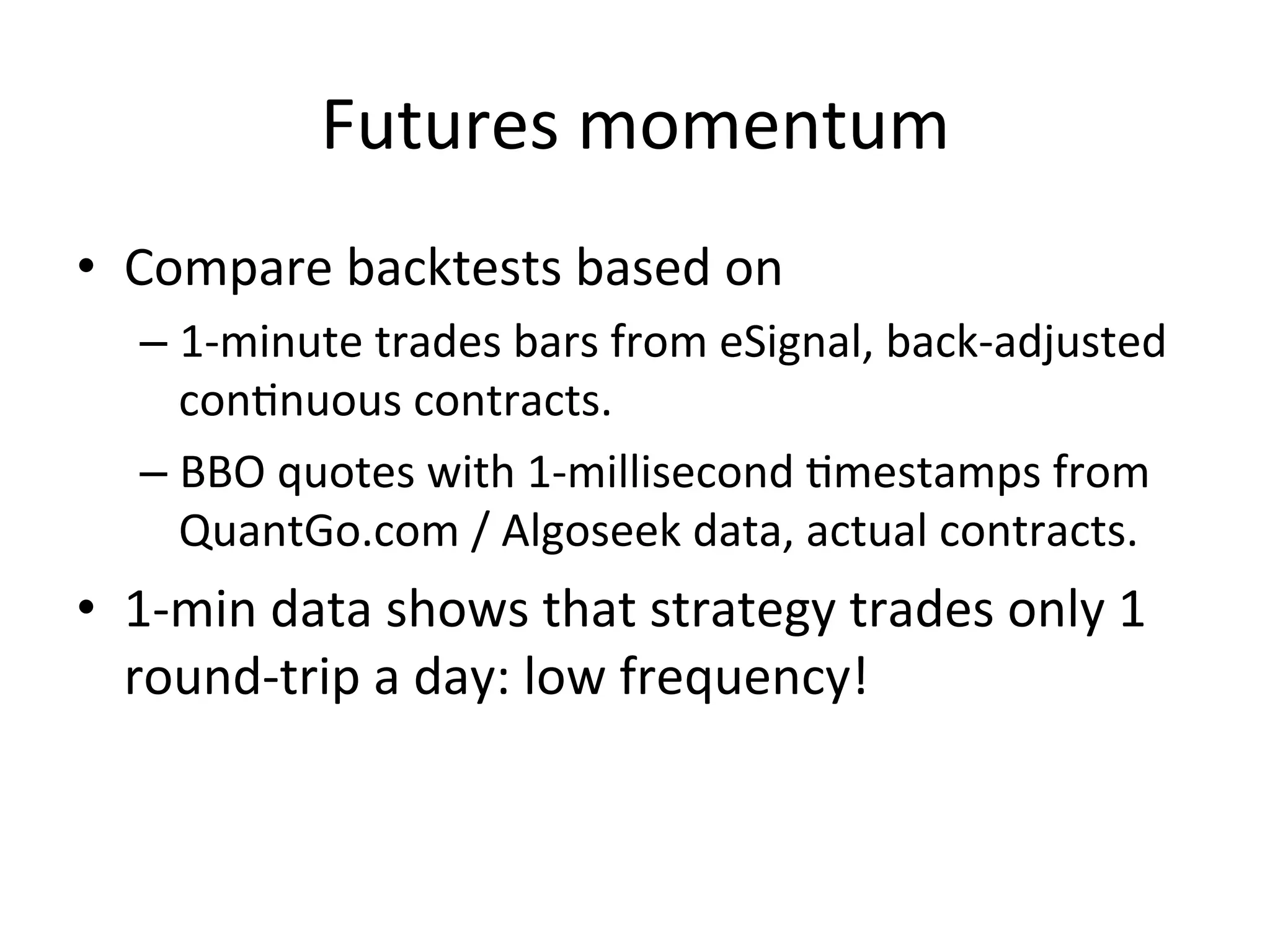

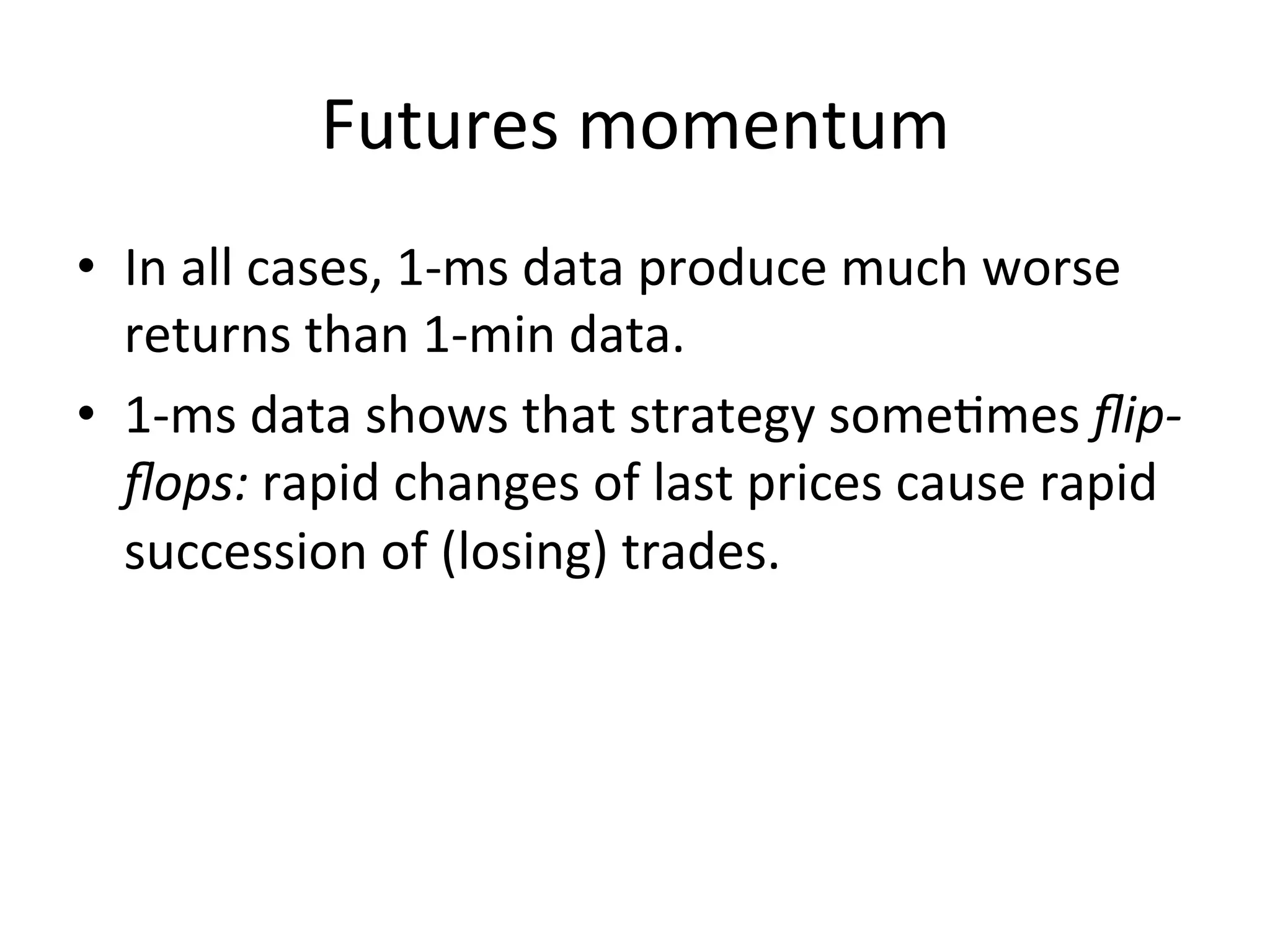

Intraday momentum strategy applied to futures; impact of data granularity on strategy performance.

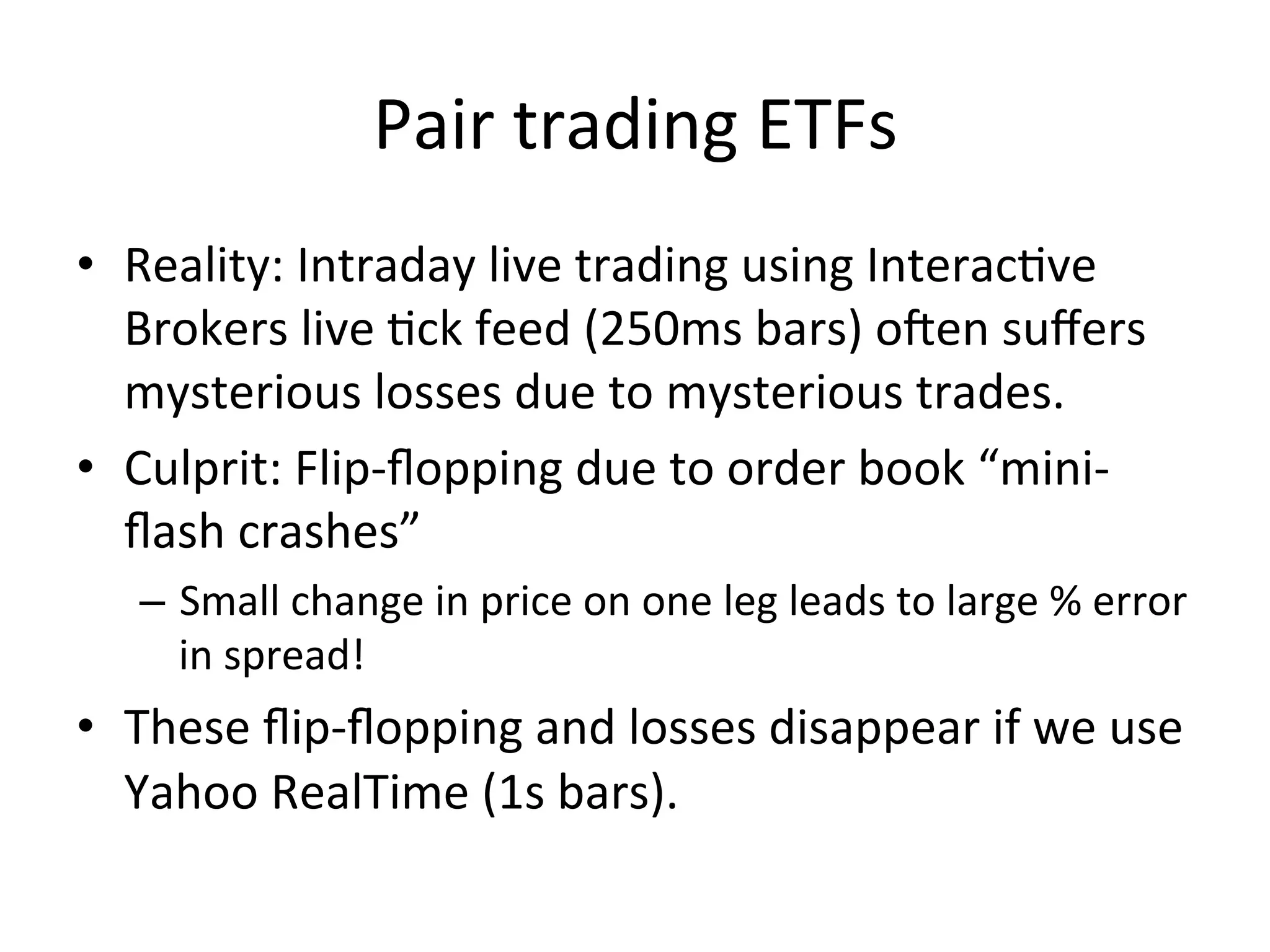

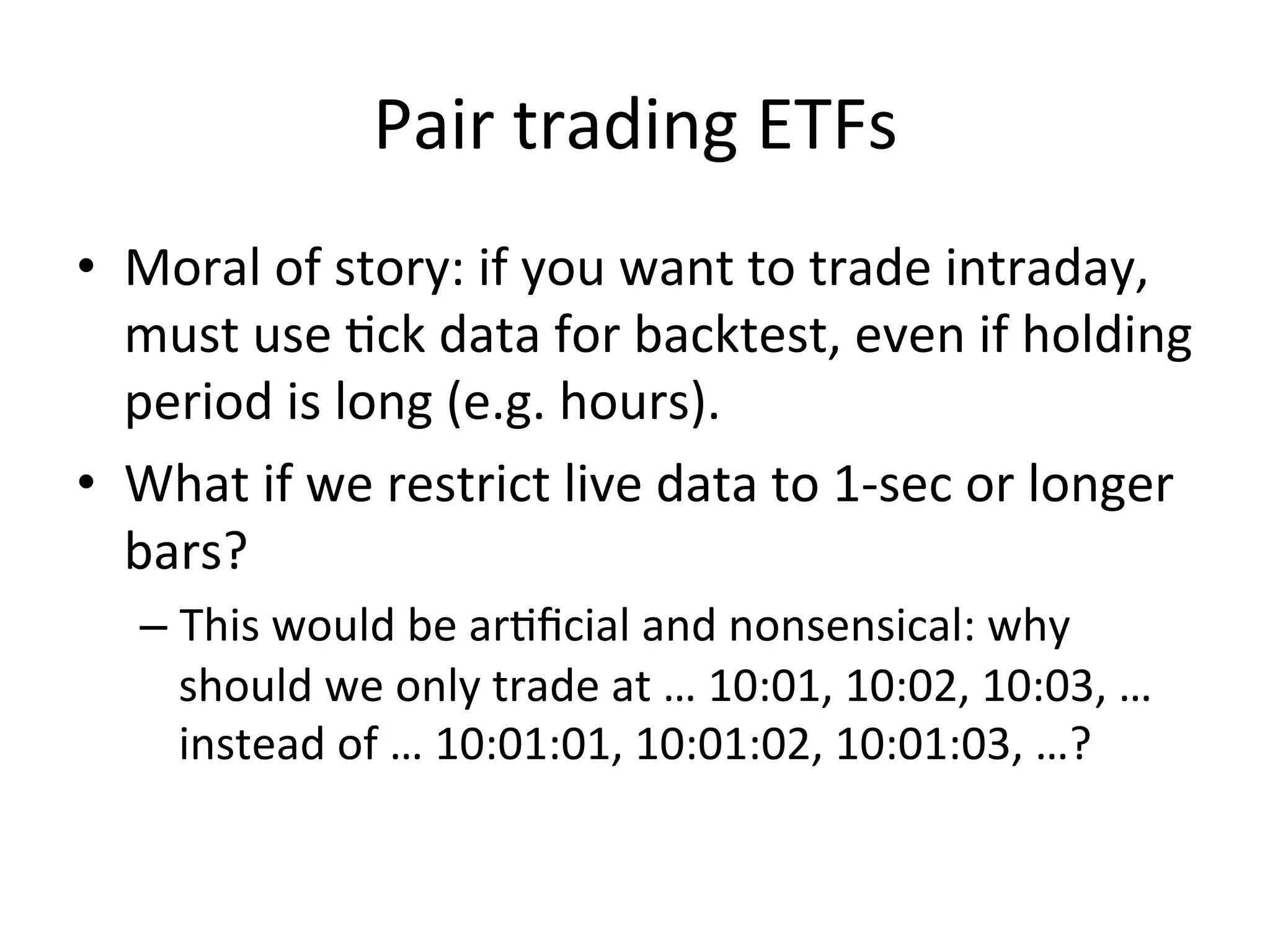

Mean-reversion pair trading strategy using ETF pairs; issues with intraday live trading performance.

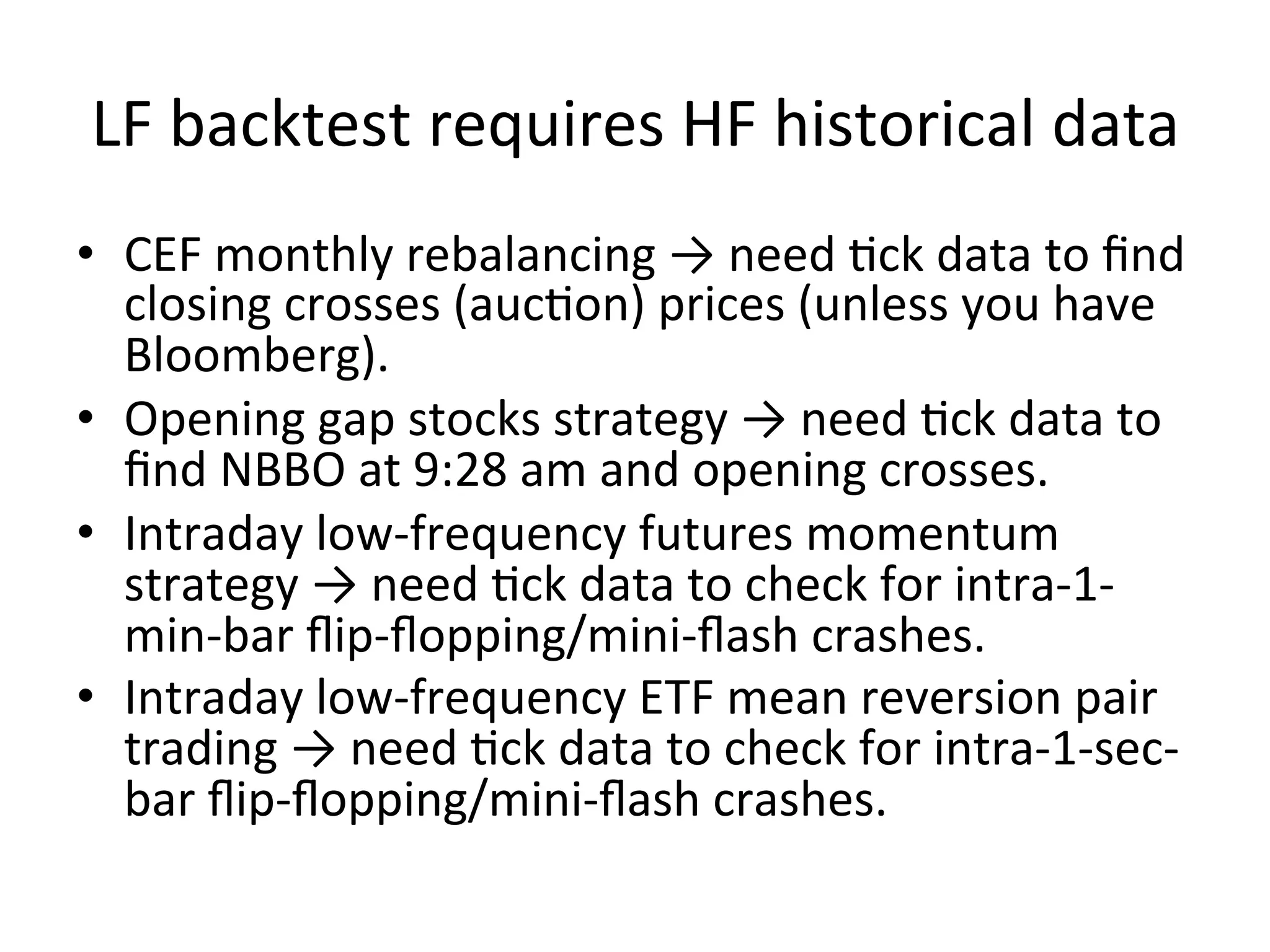

Strategies require high frequency historical data for accurate backtesting and execution.

Thank you note and resources for further information on trading strategies.

![[Data Meetup] Data Science in Finance - Building a Quant ML pipeline](https://cdn.slidesharecdn.com/ss_thumbnails/buildingaquantmlpipeline-191009091209-thumbnail.jpg?width=640&height=640&fit=bounds)