Downloaded 76 times

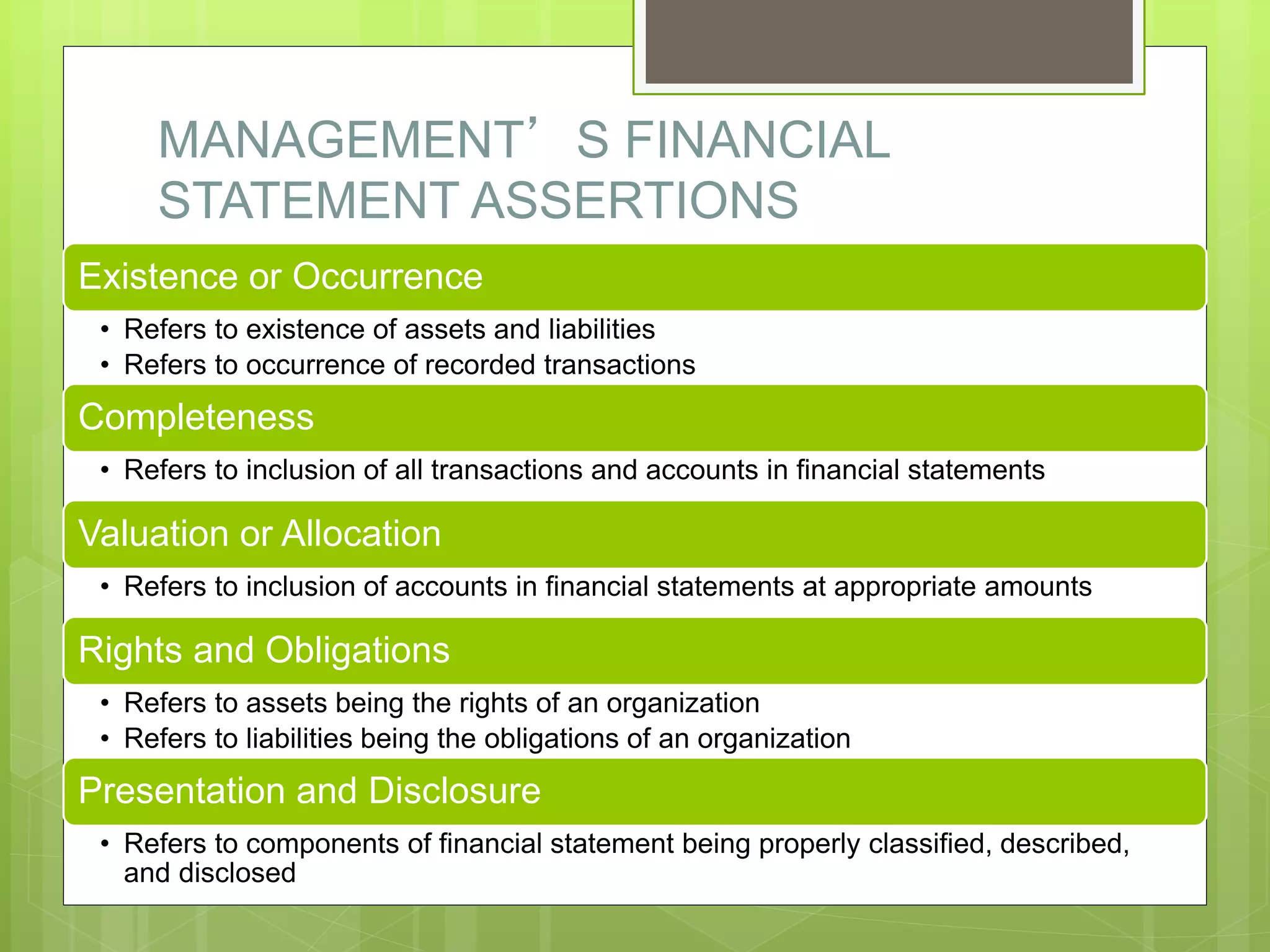

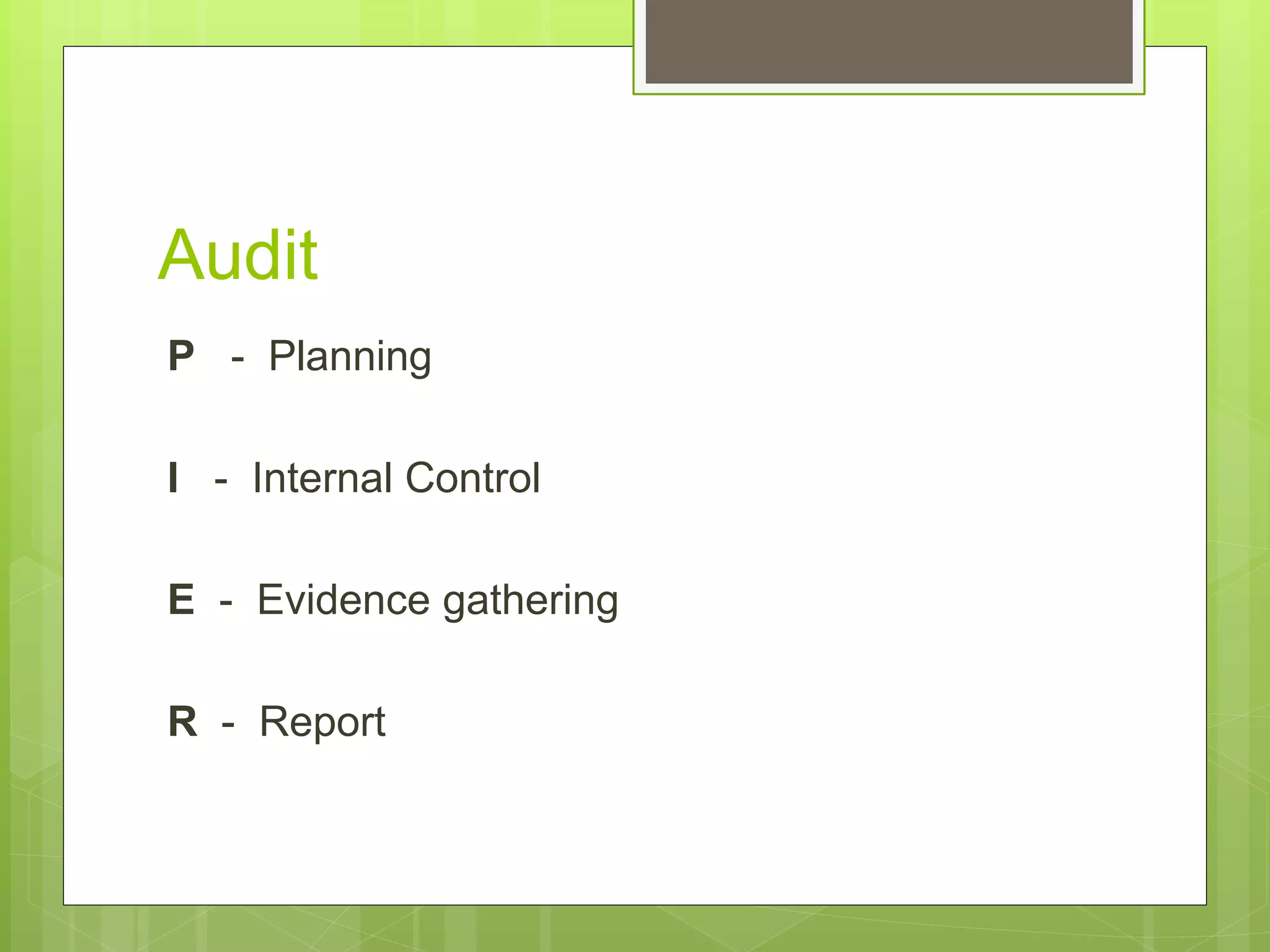

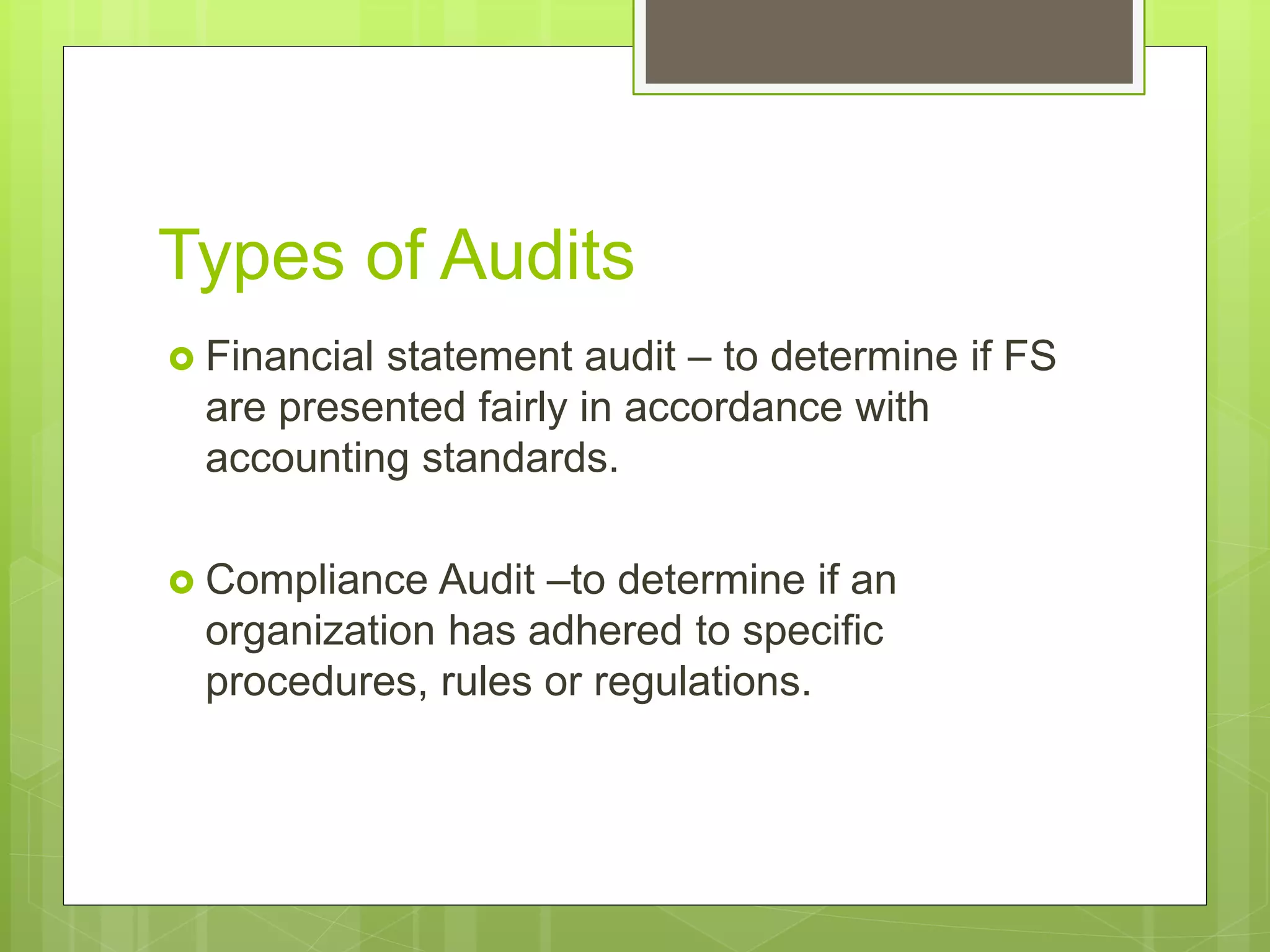

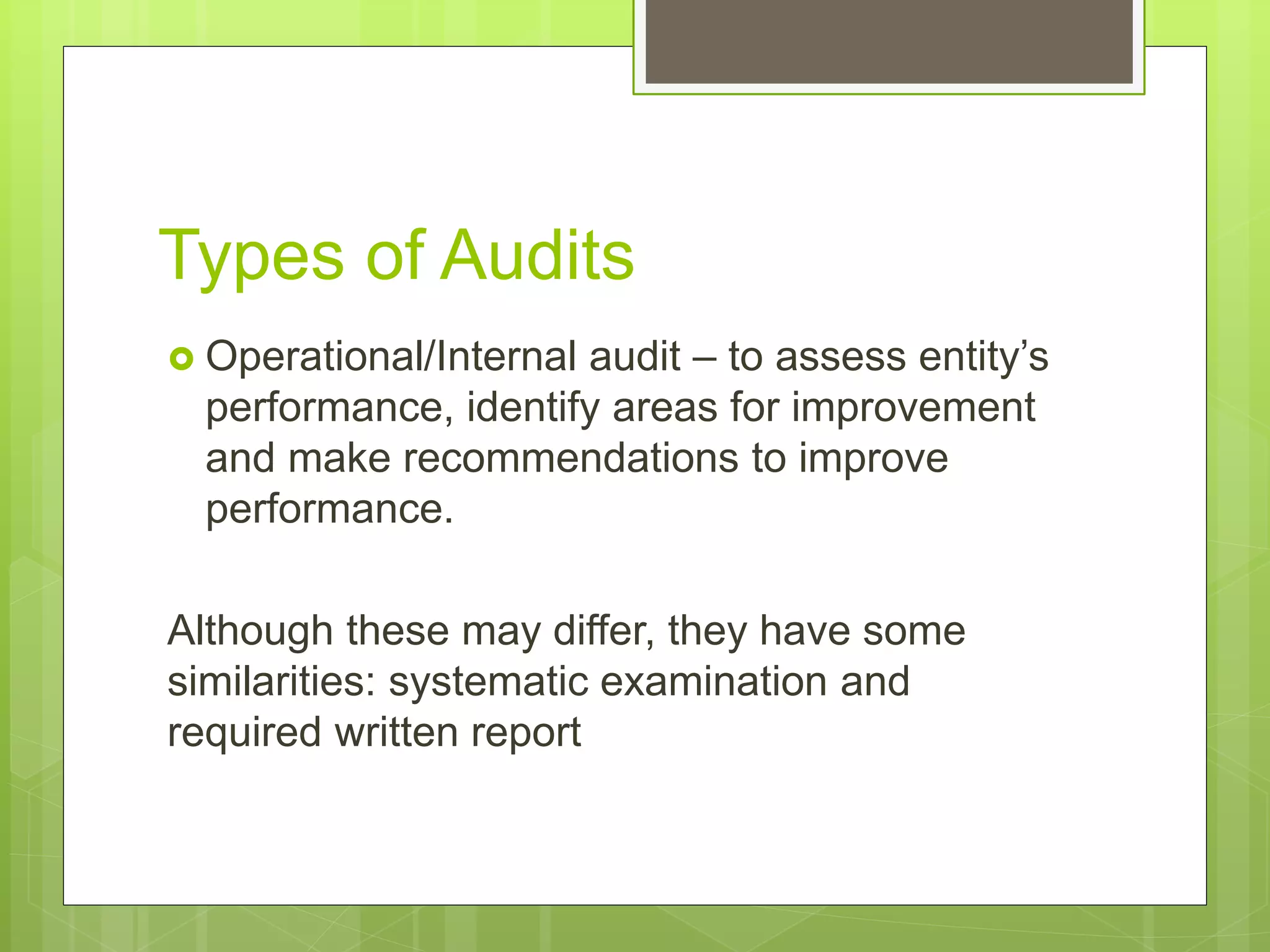

An audit is a systematic process of objectively obtaining and evaluating evidence regarding financial statement assertions to determine if they are in accordance with established criteria. The auditor ascertains if assertions about economic actions and events, such as existence, completeness, and valuation of assets and liabilities, are fairly presented. An independent audit provides reasonable assurance of the reliability of financial statements and helps ensure management has fulfilled its responsibility to adopt proper controls and prepare accurate reports.