Download to read offline

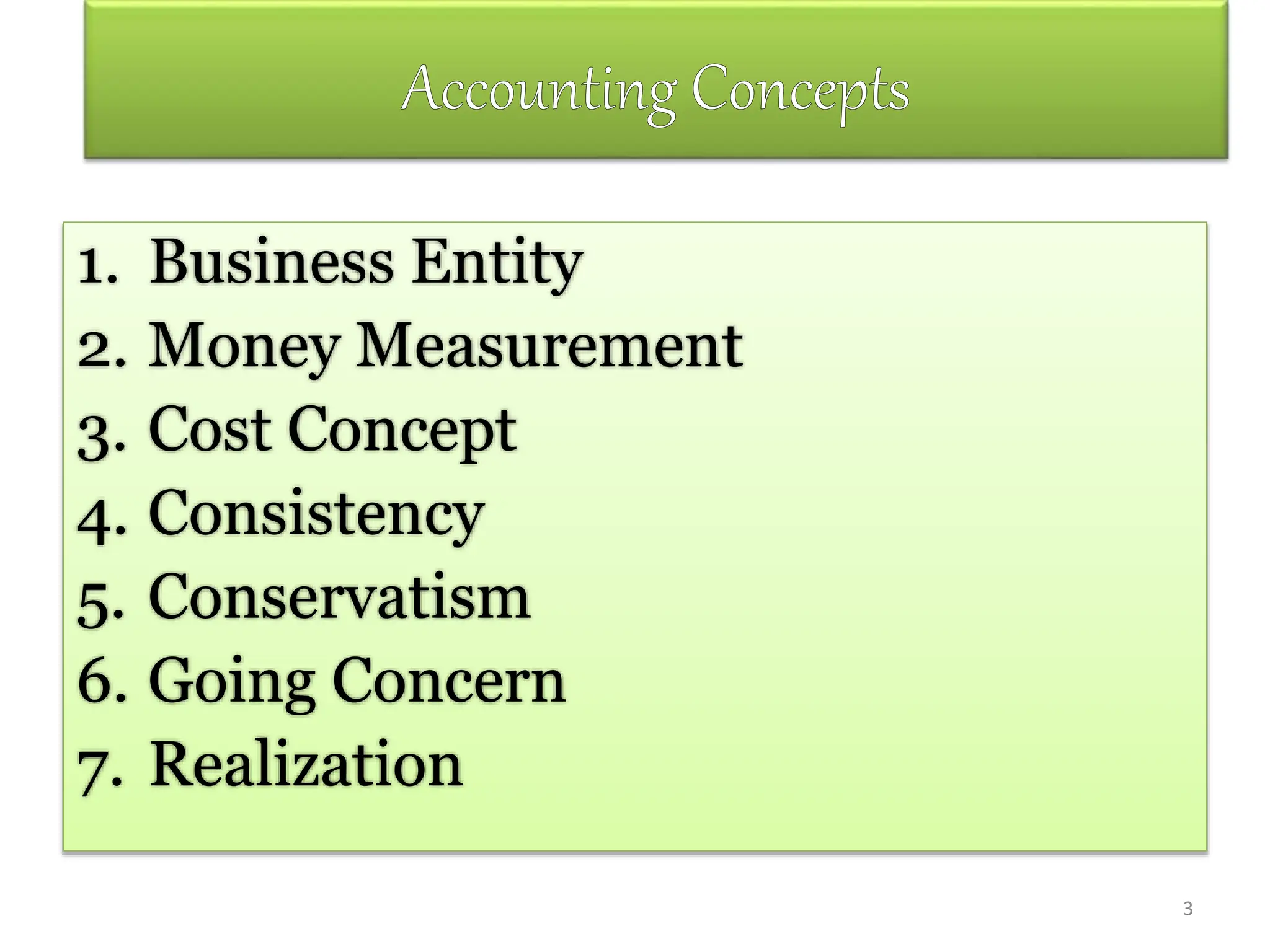

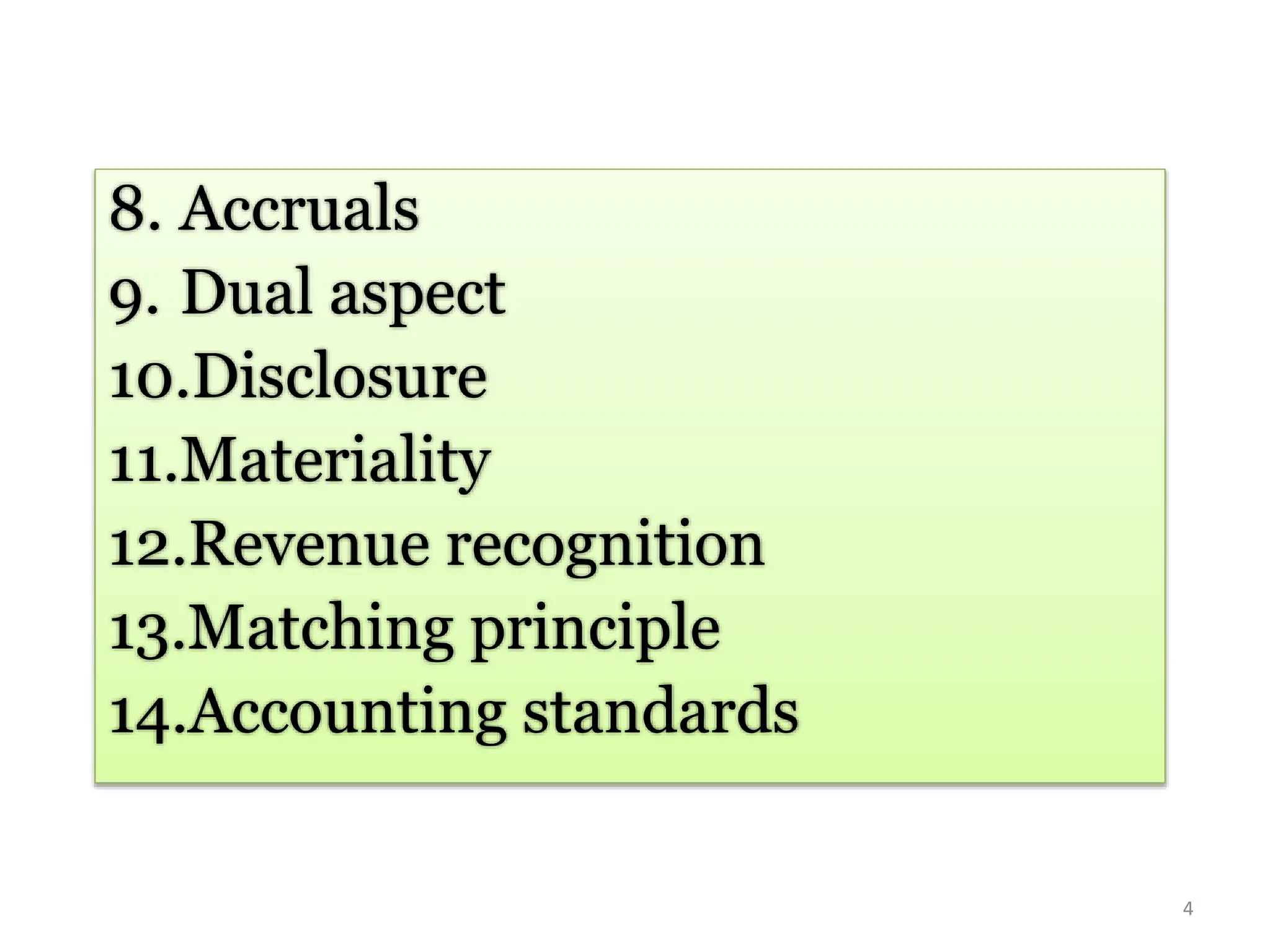

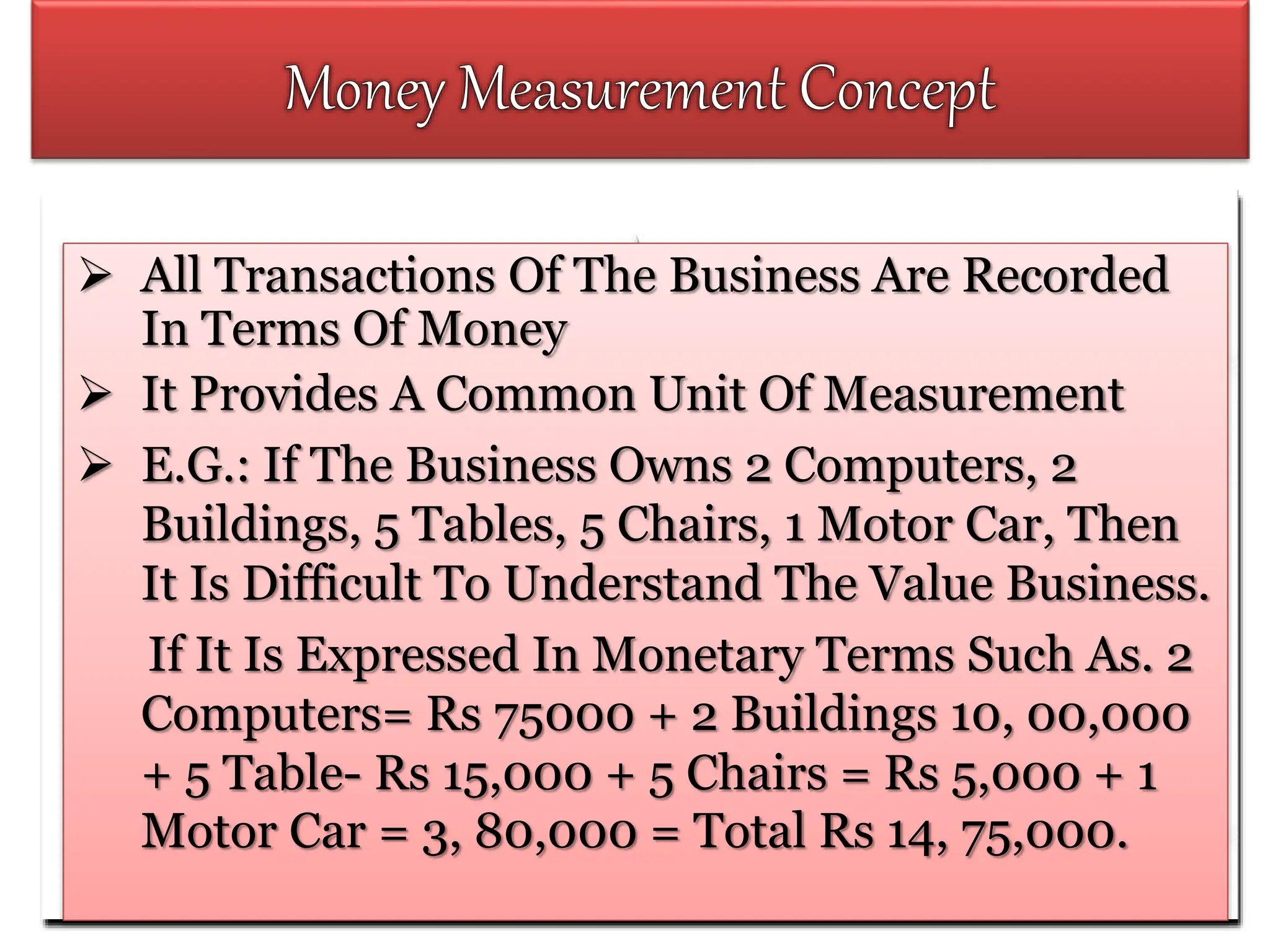

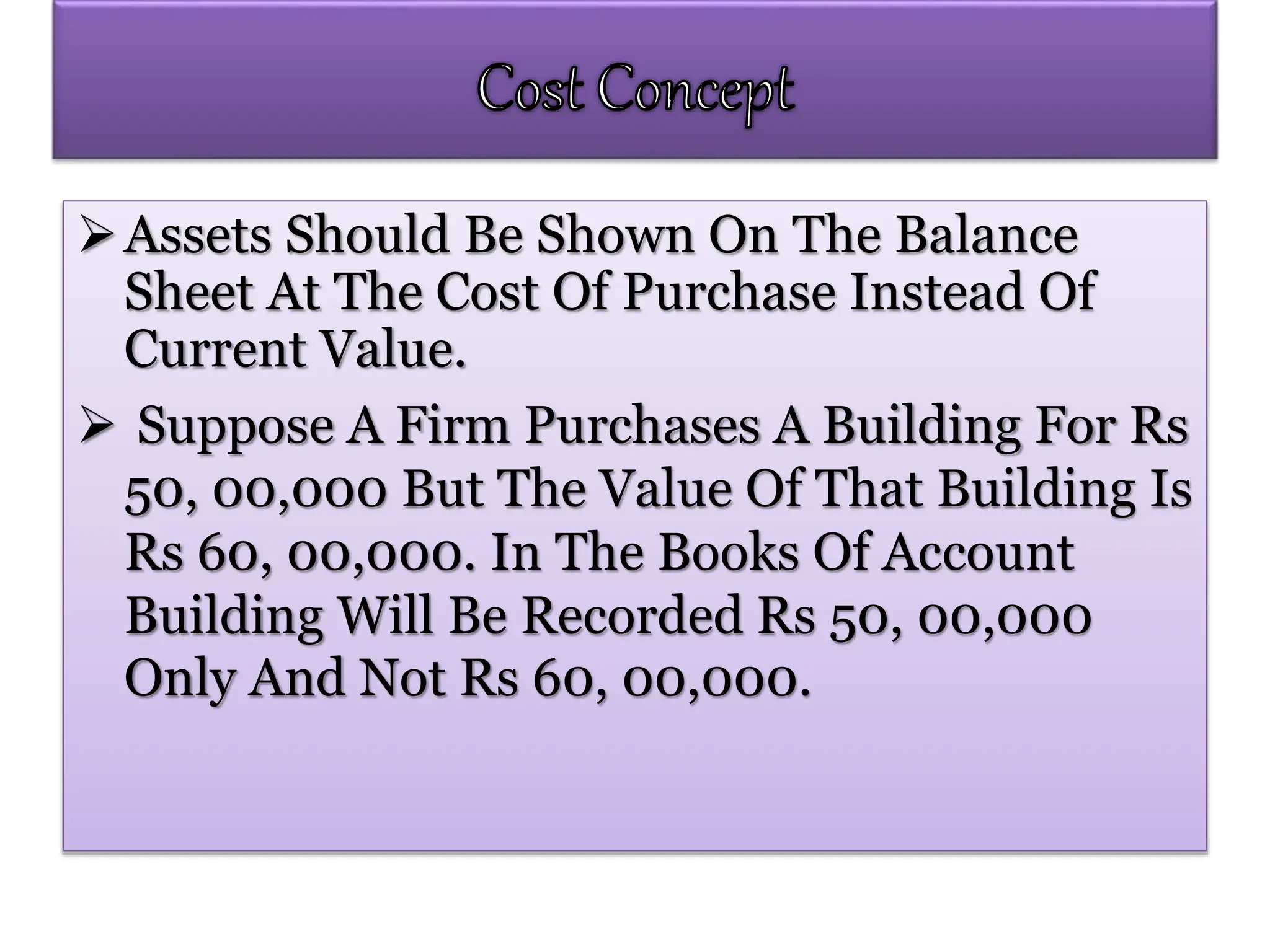

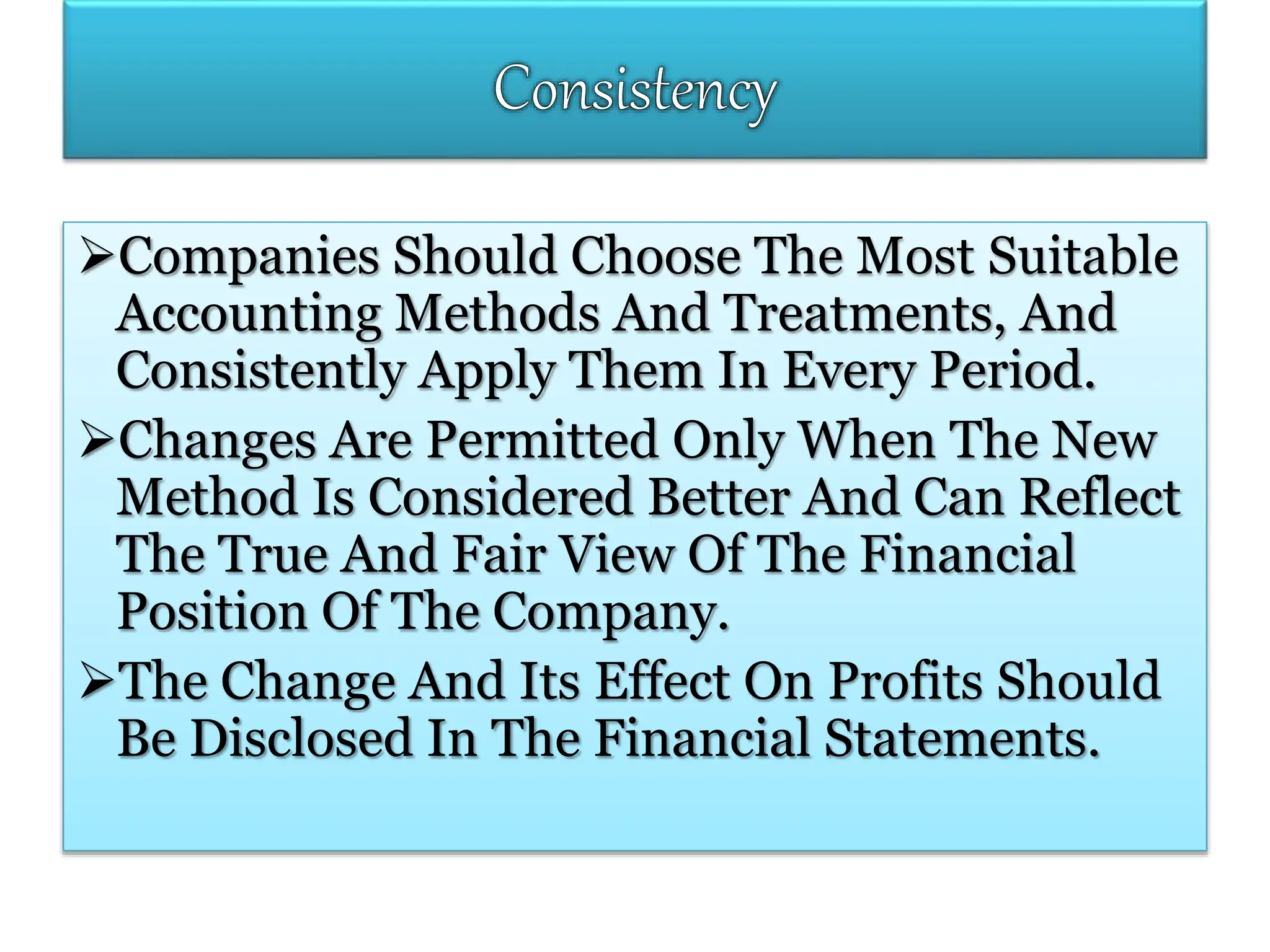

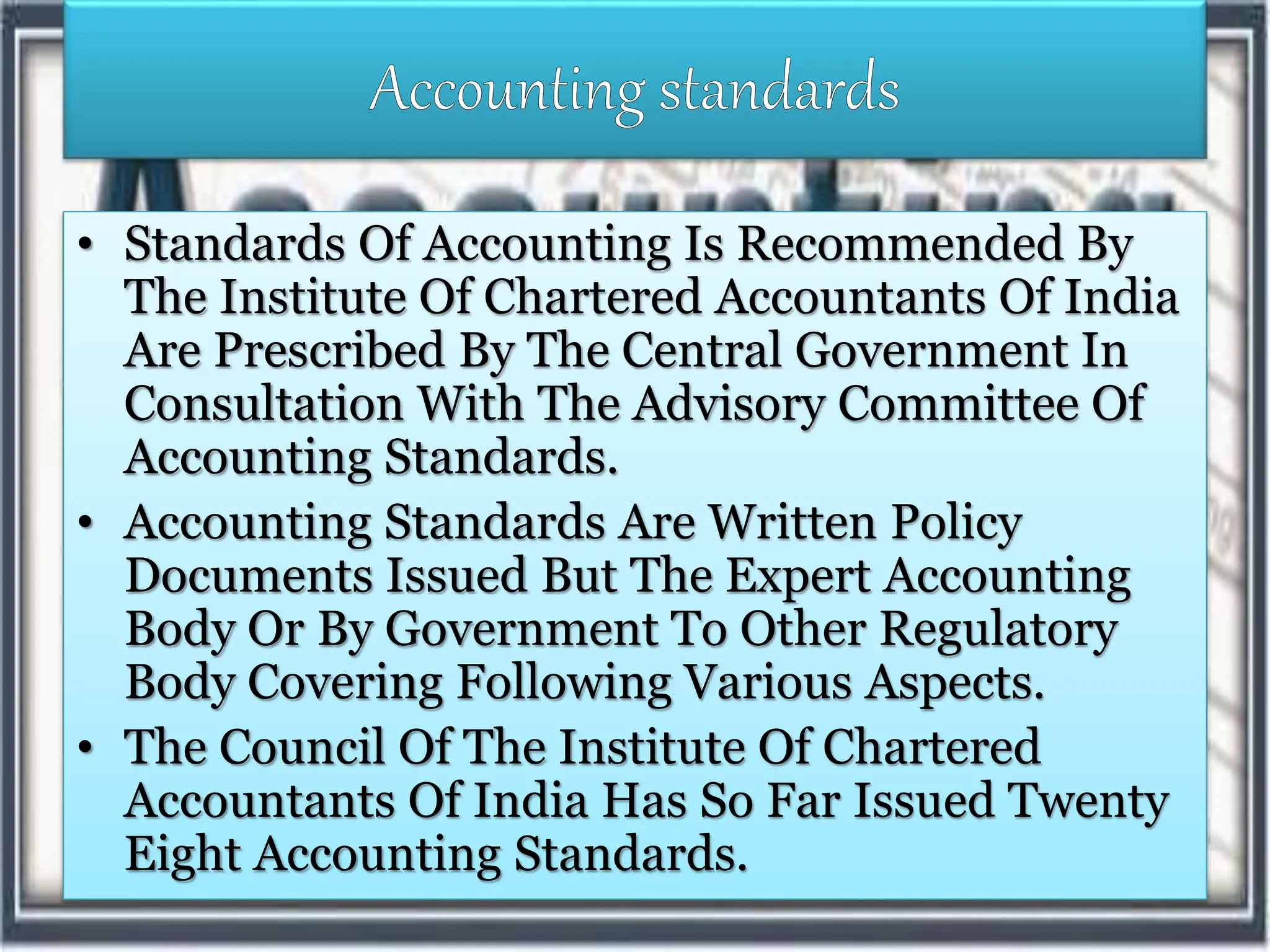

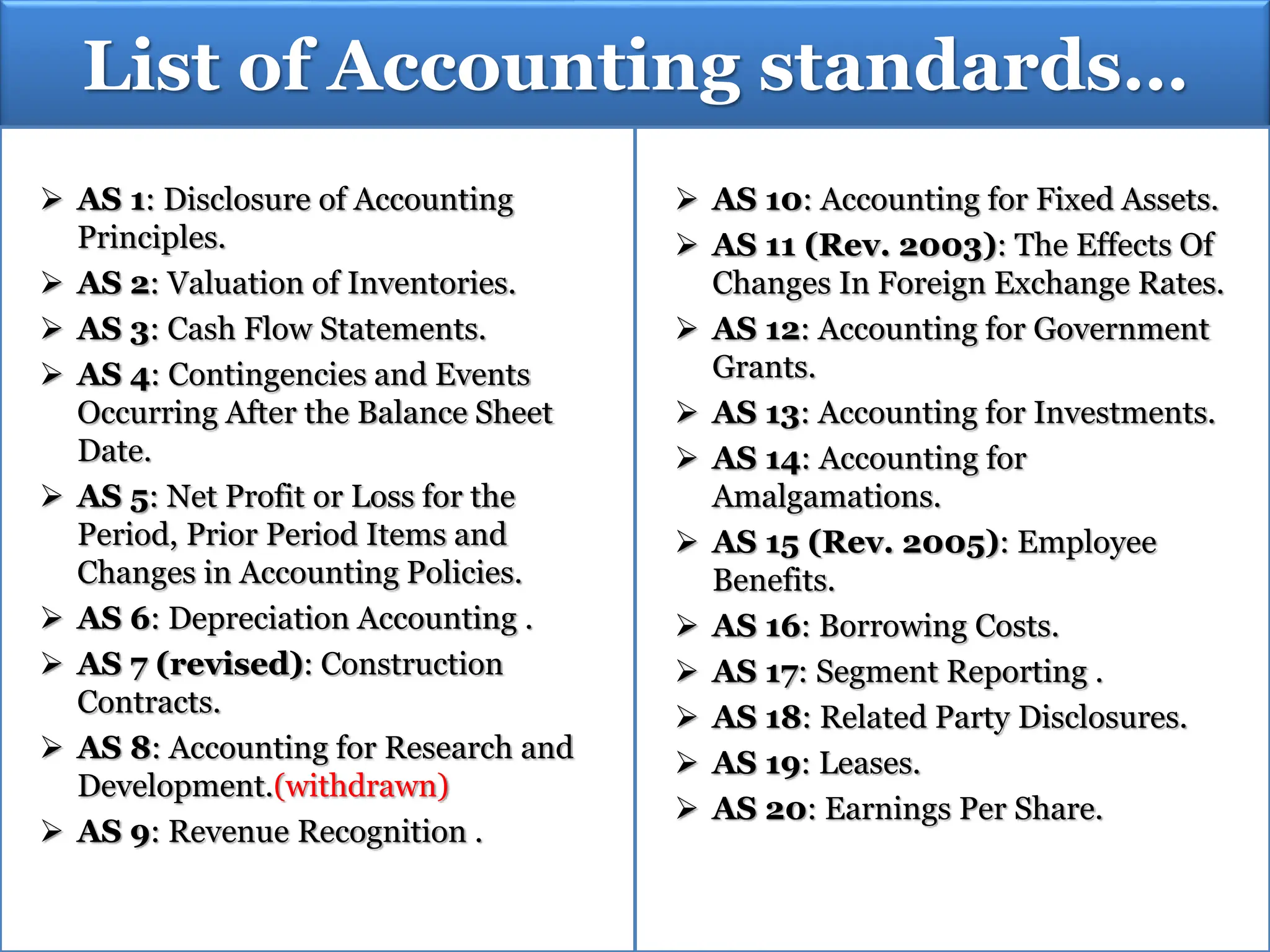

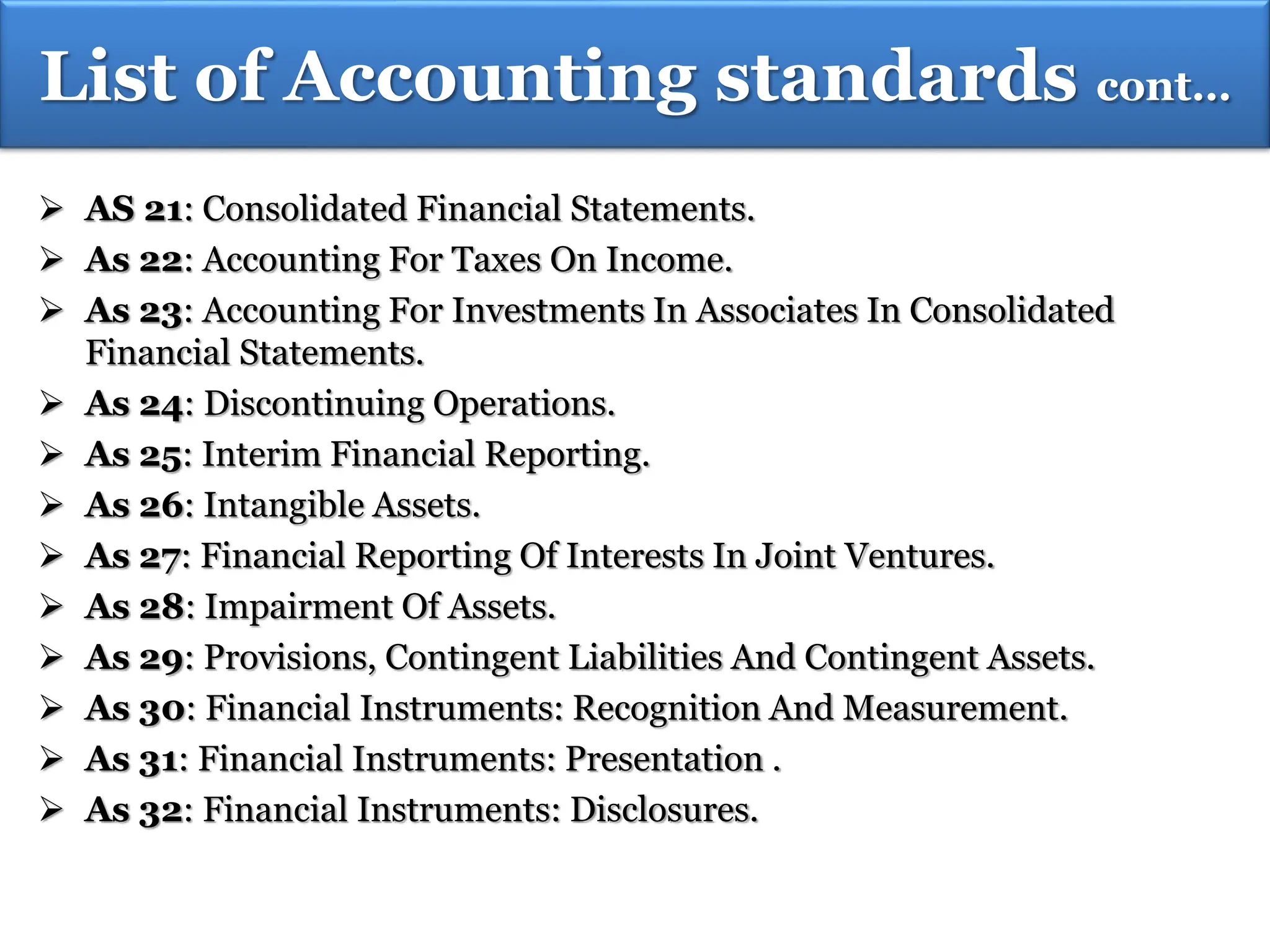

The document outlines various accounting principles and concepts essential for preparing accounts, such as business entity, money measurement, consistency, conservatism, and revenue recognition. It emphasizes that transactions must be recorded in monetary terms and highlights the importance of recognizing revenues only when realized, with a focus on matching expenses to revenue. Additionally, the document briefly details accounting standards set by the Institute of Chartered Accountants of India, which govern different aspects of accounting practices.